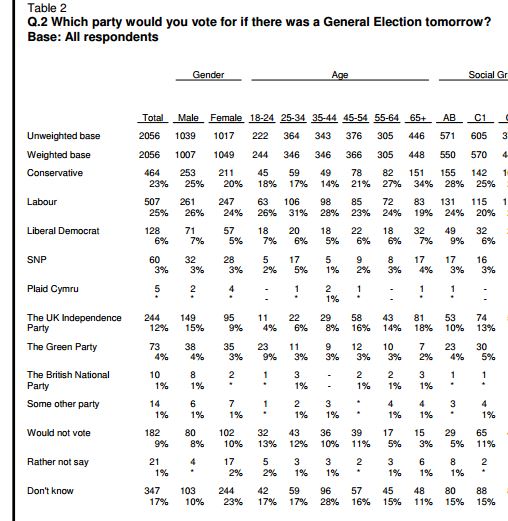

This is an extract from the most recent Populus Voting Intentions Poll:

On Friday, Faisal Islam noted the huge difference between the voting preferences of the young: 18-25; 25-34 and 35-44 (all of whom show a strong preference for Labour) and the old: 65+ being the only group showing a strong preference for Conservatives.

On Friday, Faisal Islam noted the huge difference between the voting preferences of the young: 18-25; 25-34 and 35-44 (all of whom show a strong preference for Labour) and the old: 65+ being the only group showing a strong preference for Conservatives.

The Conservatives responded, today, by announcing that they would extend the Pensioner Bonds scheme of which, as I put it:

So which came first? The chicken or the egg?

In an idle moment – ha! – I trawled back through the Budgets and Autumn Statements of this Parliament to look for measures targeted specifically at the young and old. How have those groups borne the burden of those public spending decisions?

Such an exercise quickly runs aground because many of such measures are not specifically costed. Either you include measures only if specifically costed – which leads to one kind of distortion – or you confine yourself to looking at changes to tax and benefits (which are always costed) but ignoring age-specific non-tax or benefit changes (pensioner bonds, student tuition fees, Public sector pensions, etc). I chose the latter.

Sometimes, the costs change between when the measures are announced and when they are implemented. Again, for the sake of consistency, I have given the costings for the first period for which full costings are given. If no full costings have been given, I have given the latest provided. I can’t promise to have done this exercise perfectly – tracing through the full costings of measures announced with prospective effect is complex – but what I have done follows.

- introduced the following measures benefiting +65s: introduced the pensions triple lock (£5,730m), pension credit minimum income guarantee (£3,170m)

- introduced the following measures hitting -21s: restriction to Sure Start Maternity Grant (£375m), abolition of health in pregnancy grant (£640m), abolition of Child Trust Fund (£2,530m), abolition of Savings Gateway (£410m), conditionality for lone parent benefits (£1,390m), second income threshold for family tax credits (£660m), child tax credit remove baby element (£1,395m), child tax credit reverse supplement (£900m), freeze child benefit (£5,185m)

- introduced the following measures benefiting -21s: increase child tax credit plus above indexation (£8,910m)

Net Effect: Over 65s gain £8,900m; under 21s lose £4,575m

2010 Comprehensive Spending Review:

- introduced the following measures benefiting +65s: Cold weather payments (£200m)

- introduced the following measures hitting -21s: withdrawal of child benefits to higher rate taxpayers (£10,110m), changes to working tax credit for families (£4,290m), child tax credits – use RTI (£1,010m)

- introduced the following measures benefiting -21s: increase in child tax credit (£1,805m)

Net Effect: Over 65s gain £200m; under 21s lose £13,605m

- introduced the following measures hitting -21s: abolition of Employment and Support Allowance NICs concession £35m

Net Effect: under 21s lose £35m

- introduced the following measures hitting -21s: reversal of changes to child tax credit (£4,940m), freeze working tax credit (£1,385m)

Net Effect: under 21s lose £6,325m

- introduced the following measures hitting +65s: freezing of age-related allowances (£3,290m)

- introduced the following measures hitting -21s: threshold and tapering of child benefit (£1,505m)

Net Effect: under 21s lose £1,505m, over 65s lose £3,290m

- introduced the following measures benefiting +21s: increase child benefit (£175m)

Net Effect: under 21s gain £175m

Nothing

- introduced the following measures hitting +65s: limiting foreign winter fuel payments (£20m)

- introduced the following measures benefiting +21s: abolition of Employers’ NICs for under 21s (£1,945m)

Net Effect: under 21s gain £1,945m, over 65s lose £20m

As I have discussed here the 2014 Budget showed a yield from the introduction of pensions flexibility. That yield flows from the assumption that pensioners will choose to draw money from their pension pots earlier than they would otherwise have done, with a consequential acceleration of income tax receipts. The fact of this projected yield – of £3,045m – does not seem to me to justify the introduction of pensions flexibility as a measure “hitting” pensioners. I have also not included – as the expenditure thereon constitutes neither tax nor benefit expenditure – the initially (i.e. before today’s extension) projected £215m cost of pensioner bonds.

- introduced the following measures benefiting +21s: exempting children from air passenger duty (£390m)

Net Effect: over 21s gain £390m.

If one nets off all of these figures over 65s have gained in changes in tax and benefits during the life of this Parliament £5,790m and under 21s have lost £23,535m.

Chicken or egg? I don’t really care whether the Tories have fed the demographic that keeps them in power; or pensioners vote for Tories because of their policies. And I’ll leave others to consider the question of fairness. But I will say this: my assessment of the answer to that question will be the decisive factor in how I vote come May.

Note: Updated on 8 February at 17.45 to correct a double counting error.

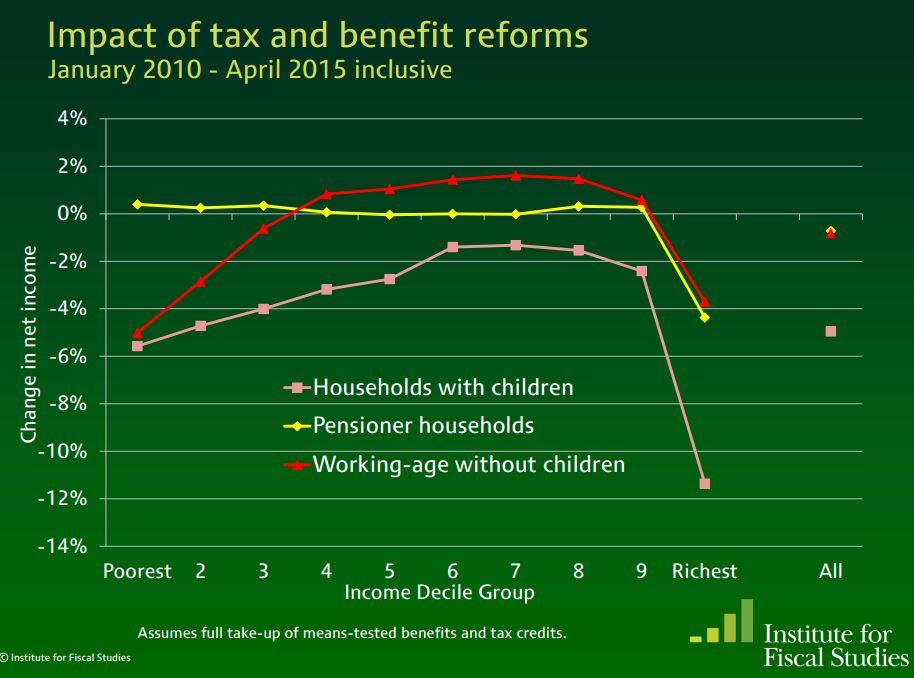

Further Note: the knowledgeable and helpful Heather Self – @hselftax (and well worth a follow) – has pointed out that the IFS has done a similar exercise showing the effects of tax and benefit reforms on household income. Here’s one of several relevant slides.

You must be logged in to post a comment.