Along with so many other members – and former members – of the Labour Party my thoughts in the second half of 2015 have been much absorbed with how to respond to the new direction it has chosen to take.

I have never pretended to be tribally Labour. My affinity is more to an idea of social justice than to a Party which once manifested its delivery and contains elements which hope to do so again. So I do not have to pretend, now, that I have not asked whether Labour remains the Party for me. My analysis – right or wrong – is that the path the Party is set upon may well lead – indeed without change is likely to lead – to permanent electoral oblivion. I also believe I could have more influence on Government policy were I not a member of the Labour Party. And the choice between working to save the Labour Party and working to better my country seems to me no choice at all.

What has kept me in the Party is the hope that Labour might again choose to manifest itself as a machine for delivering social justice. That, and a dogged attachment to the idea of good governance. Challenge, transparency, accountability, honesty, representation, diversity: it is a (rather lawyerly) adherence to an idea of how good policy is formed and implemented and overseen that has kept me in the Party. Not because I think Labour has any monopoly over those qualities – it absolutely does not – but because good Government depends upon good governance and good governance demands good opposition. And, enfeebled though its capacity to fulfil this role presently is, Labour is the only opposition the country has.

So I remain to try and cause it to so manifest itself again.

It has been said, and often, that candidates other than Corbyn offered little in Labour’s leadership elections. I think this is broadly true. But it is much less damning than might at first be thought.

Cooper, Kendall and Burnham thought they were competing against each other – and would have time after victory to put together a policy offer. This is, of course, exactly how good ideas are made. They do not spring fully formed from the mind of some mythical leader. They emerge from a process of deep and iterative thought. As I listened to the early leadership hustings what I most wanted was to hear someone with the courage to admit that they were still embarked on the journey of finding out what the solutions were.

And Cooper, Kendall and Burnham did not see until it was upon them the Corbyn steamroller. And then it was too late to respond. And in this, of course, they were mistaken – but they were far from alone.

And although I do not know what they were for I have little sense of what Corbyn’s Labour is for either. His appeal in the leadership campaign was primarily to higher spending and a largely unarticulated notion of change. Since his victory his more lavish policy offerings – for example, closing the so-said £120bn so-called tax gap or ditching the so-called £93bn of so-called corporate welfare – have (rightly) been shelved. And the gruel that has been replaced them has largely been drawn from Labour’s 2015 Election Manifesto – that and the policy platform of Stop the War.

But whether or not you think this analysis fair, what certainly is fair is the challenge laid down by those who remain supporters of Corbyn’s brand of politics: what is Labour’s rump for?

I have tried to engage with others in the rump to formulate a mode of responding to this challenge – and I will continue to. I hope something emerges soon – because I believe time is short. But for the meantime I will write personally, offering some tentative thoughts here and elsewhere. I should say, in particular, that I am very grateful to the New Statesman’s political blog for giving me the space to write. I hope they will continue to – especially as I wander further from my area of professional expertise.

So in the coming months – at least as time allows, because my workload in the coming months is especially heavy – I will write on some of conversations I believe the Party should be having. I hope to write on the following themes.

What do we want from our State?

Whilst ‘anti-austerity’ may unify us internally – although I sometimes wonder whether this is only because the expression is so open textured that we can march in uneasy step behind it – I think it is (and rightly) electoral poison. To the public at large, it neatly articulates their fear that Labour would deliver more spendthrift Government. To the taxpayers of today and tomorrow who must fund it, it is an undifferentiated appeal for a bigger state. Its appeal to that part of the electorate might be compared to the appeal to those who must suffer it of (some amongst) the Conservatives’ desire for a smaller state. Both are unprincipled and both are wrong-headed. But the difference is that the Conservatives realise this and do not campaign on it.

Instead, we must start by identifying what we want the State to be. We must make the case for it to exercise those functions. And what delivering them properly would cost. And if the result is spending more then we will at least have a principled basis for explaining why that is the right thing for us to do as a society.

What should be the relationship between business and society?

If I rub my crystal ball, this emerges as the defining political question of our time. As our lives fall into ever greater and more uneasy thrall to the power of money, what as a society can and should we ask of those who have it? How can we ensure business works for all of us? It is this question – and its answer – that represents perhaps the one great opportunity open to the Left. It is space that the Right is politically unable and financially unwilling to occupy. Scepticism of whether business has our interests at heart is both deep-rooted and widespread. We all sense – even if we find it difficult to articulate them – the ways in which money has come to corrode values that all of us hold dear.

But there are yet further levers open to sophisticated Government for ensuring that business behaves in all our interests. And a carefully modulated argument – challenging but not oppositional – for developing and wielding those levers would, I believe, deliver real electoral gains. Only Labour can persuade voters that it is on their side – but it still has to do so.

What should our tax system look like?

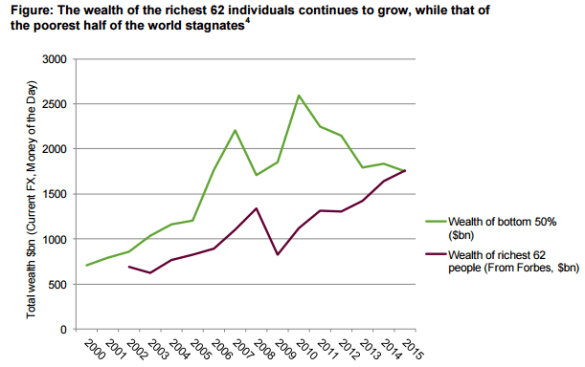

As the world changes, as wealth continues to cascade up, adhering to fewer and fewer hands, the Left must plan for more than accretive changes to rates and bands of taxation. The case for examining whether we get value for money from the very substantial sums of revenue foregone through tax reliefs – handsomely in excess of one hundred billion pounds per annum – makes itself. Inheritance tax must be replaced by a system which is both fairer and more fiscally meaningful. And Labour cannot forever turn a blind eye to the possibilities of taxing wealth rather than squeezing ever more from income. Unless the pattern of wealth accretion changes – and I do not think it will – there will come a time when this question is no longer the right question to ask, but instead is the only question. Labour must be ahead of the curve. The starting point, it seems to me, is to ask whether wealth taxes might give us greater fiscal autonomy: is capital more or less inclined than income to flee our borders.

But Labour’s narrative around redistribution has wrongly fixated on tax alone.

The housing market, too, increasingly functions as a system for redistributing wealth, regressively, from renters and other non-owners to those who have property.

The planning system creates scarcity – less than 10% of our environment is built on with half of that ‘built on’ as subordinate garden – and thereby preserves and enhances the wealth of those who own property to the cost of those who do not. The consequences for those who cannot hope ever to own a house in our Cities – and for the economies of those Cities – and for the money we have left for productive investment – do not need to be spelled out here. But a bold reform of the planning system should not be a mechanism for delivering further wealth to those who own the land upon which new houses might be built. Labour must ensure that the bounty that planning reforms occasion is shared with the State. So that the State can deliver the infrastructure investment that those reforms necessitate – and which will deliver prosperity to other regions too. This can be achieved by taxing planning gains.

The labour market might also be seen as a redistributive mechanic.

If you erode the pay and protections offered to employees you make it easier and cheaper for business to engage them. The result (as we have seen) is an increase in employment of marginal quality to the cost of those who lose bargaining power and the benefit of those protections. On the other hand, where you drive up the price of labour – for example by increasing the statutory minimum wage – you can reduce the propensity of business to employ, distributing from it and those not in employment to those who are. This should not, either, be what Labour is for.

Labour needs to have a honest conversation about these effects. I do not ignore apple pie truisms about the need to create a highly skilled and productive labour force. But we must also have a conversation around where to draw a line in the sand. How can we ensure dignity in the labour market for the low skilled? As a society what is the baseline quality of employment that we will permit business to offer to workers? The right answer will be the familiar product of a marriage between principle and pragmatism. But it must come from these questions – not a wilfully myopic outbidding of the Conservatives on the level of the minimum wage.

So these are the themes that interest me. I will write more on them.

But I am only a lawyer – and a tax lawyer at that. There are others more suited than me to develop these – or further or better ideas. My modest goal in the coming year is to contribute to or precipitate a conversation. If your vision of the Labour Party is that it is a machine for delivering social justice I would like to issue to you an invitation. Please respond, here or elsewhere. It really doesn’t matter where. If the ideas are good, and well expressed, people will find them.

All of this means I will do less in the way of scrutiny of the Conservatives’ tax policy.

It is easy to stand on the sidelines and criticise – and after all we have so many targets to choose from. But although vigorous opposing may serve the purpose of making us feel better about the ugly reality of not being in Government, we should not fool ourselves into thinking that it is any replacement for the process of articulating our own, positive, vision of the society we would like to see and create. It is only by presenting that electorate with a better vision than that the Conservatives’ offer that we can hope to bring about the change we would like to see.

You must be logged in to post a comment.