It is, sometimes, Parliament, a wonderful thing. Here’s Charles Walker (Broxbourne) (Con.), moments after describing himself as “a capitalist, red in tooth and claw”, talking in 2008 about the levy on non-doms:

He’s tackling – head on – the one reason why we offer a tax sweetener to the wealthy with foreign connections to move to or stay in the UK. I’ve written elsewhere about the perverse effects flowing from the poor design of that sweetener. I’ve also asked some questions about whether HMRC are effectively policing it (and there is more to follow on that front). What I want to do today is look at the data: does it support the case that we need it to bring the wealthy into the UK – or keep them here?

But before I get to it, a few observations:

(1) if you’re wealthy, thinking about moving, and comparing possible places to live you absolutely compare, amongst other factors, tax regimes. Our non-dom regime has something of a gravitational effect;

(2) the power of this gravitational effect is not constant. It might pull you here – but it doesn’t follow that you continue to need it to stay. Once you’ve found a comfortable social and cultural orbit – something London absolutely offers, at least to the wealthy – the removal of any tax sweetener that factored in your decision to move here will operate only weakly in your decision whether to stay;

(3) cultural factors are important. The percentage of millionaires in New York (which doesn’t have a non-dom rule) is about a third higher than that in London (although it should be noted London does much ‘better’ when it comes to billionaires);

(4) the percentage of millionaires in both London and New York is a tiny fraction of that in the tax havens of Monaco, Zurich and Geneva. This should cause you to ask whether tax really is a major factor in London’s appeal to mobile individuals. Those motivated principally by tax have – and choose – ‘better’ alternatives; and

(5) I think it’s beyond sensible dispute that there are economic benefits for us all in attracting the wealthy to the UK. Many of the arguments to the contrary are, as I have argued elsewhere, confused.

Anyway. Those observations aside, the data.

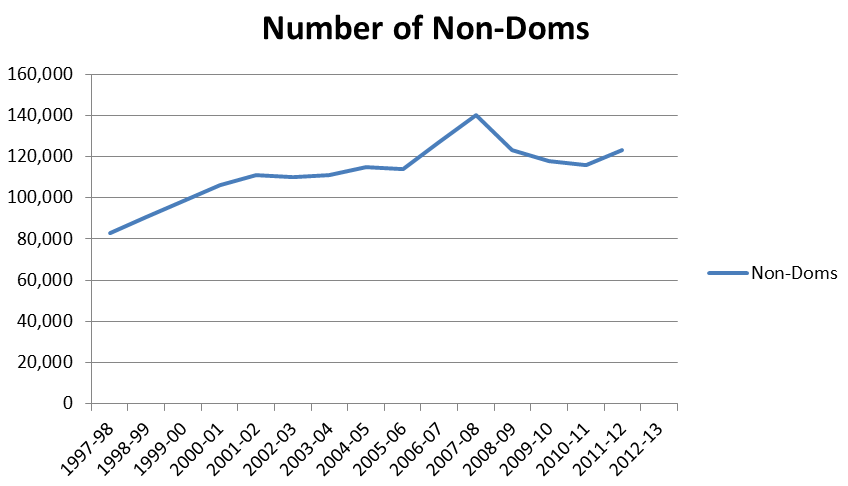

What follows is a table garnered from various ‘official’ sources (to avoid clogging up the post, the sources for all of the data are given in a ‘comment’). The table shows the number of non-doms registered with HMRC over time. Do the Chicken Little arguments of those law firms who advise non-doms – that the effect of the introduction of the non-dom levy has been cataclysmic – stand up?

The non-dom levy was introduced in the tax year 2008-09. The number registered as Non Dom then in the country was 123,000. The number registered as Non Dom for the last available year (2011-12) is… 123,000.

The apparent peak was 140,000 in 2007-08. I say ‘apparent’ because there are very good reasons to be sceptical. It can only be right if there was a huge jump from 2005-06, followed by a matching huge fall to 2008-08 and all against a consistent pattern of gentle increase.

What does this mean? The only argument for tax sweeteners is that we need them to attract or retain the mobile wealthy. If – as the data shows – reducing those sweeteners hasn’t materially affected our ability to attract or retain them, it’s entirely proper to ask whether removing them would.

Note: I have not found figures for 1997-98, 1998-1999, 1999-00, 2006-07. The table, therefore, assumes a steady progression between the ‘known’ numbers on either side of the missing years.

You must be logged in to post a comment.