On Sunday I wrote about how the tax system, examined as a whole, isn’t nearly as progressive as George Osborne suggests. It’s regressive, in fact.

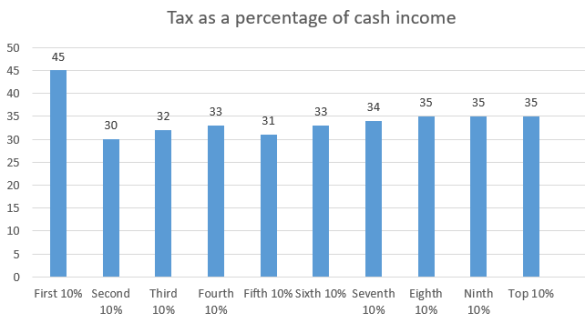

I gave the Office for National Statistics numbers for ‘quintiles’ – the lowest to highest earning fifths – of households. But here’s a chart for deciles which makes the point even more strikingly.

These are ONS numbers – taken from here – and they give tax as a percentage of the total of earned income and cash benefits.

The main culprit is Council Tax which – even after ‘Council tax support’ – consumes 9% of the total for the First 10% but only 1.5% of the income for the Top 10%. Every time – as with, for example, the Social Care Precept – Government chooses to fund spending through Council Tax you should be outraged. It is willfully choosing to dump those costs on the poorest because to do so is politically expedient. Collectively we understand but poorly the distributional effects of raising Council Tax. This enables Government to do what it should not without political cost.

But alongside the regressive nature of our tax system there is a related debate to be had about benefits.

Does it matter that the poor are disproportionately taxed if they disproportionately benefit from the benefits taxes fund? Is it the net effect of taxes paid and benefits received that one should analyse?

Of course, this is not what Osborne sought to do. The currency of political debate is ‘who bears the burden of taxation’. That political debate readily assumes, and often in ugly language (see this reference to “scroungers“), that the poor are beneficiaries of a burden borne by others.

But there is also a discrete, economic, debate.

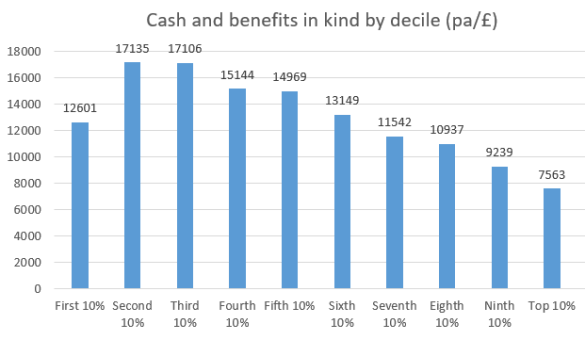

This debate is also informed by ONS figures. Here are their absolute numbers for cash and other benefits in kind received directly from Government (see Table 14).

The explanation for these numbers lies, in particular, in the universality of the state pension; the fact that all deciles are substantial consumers of education and (in particular) the NHS; and the fact that the rail subsidy is disproportionately enjoyed by the rich.

Of course, looked at as a percentage of income rather than in absolute terms, the poorer deciles benefit more than this chart reveals. But in absolute terms the differences in the extent to which the deciles benefit directly from Government are far less profound than you may expect.

I use this phrase “directly from Government” quite deliberately. The ONS figures capture those benefits we receive directly. But they do not capture those benefits we receive indirectly. They do not capture the extent to which the wealthy benefit from the infrastructure that enables income to be generated and wealth to be protected.

If we analyse who are the big beneficiaries of that infrastructure – of the legal system that enables income to be generated and protects property rights, of the police and army that secure our wealth from confiscation by acquisitive forces, of all the complex systems that Government provides and sustains and which enable us to earn our incomes – it is self-evidently the wealthy and high earners who benefit most.

Is there some argument that requires that we have regard to the direct benefits our tax system funds – but that we ignore the indirect benefits? If there is, I do not see it.

Of course, we should all benefit – as economic agents and as moral beings – from the social compact to which we, willingly or unwillingly, subscribe. We are, as George Osborne observed in the quote with which I began this discussion, “in it together.” True, we benefit differently. But we must each contribute according to our means.

Follow @jolyonmaughamPostscript:

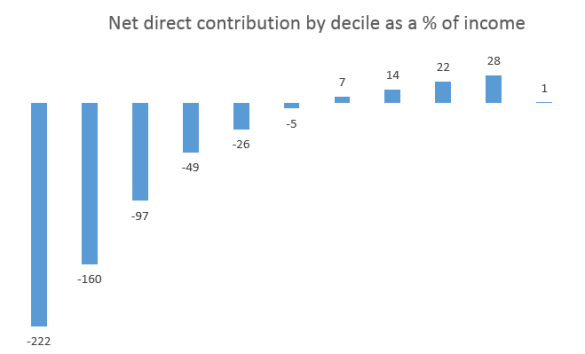

Here’s Andrew Jackson’s chart (see ‘Comments’below) of net direct contributions (I have re-titled his chart but the data is his).

Andrew adds:

“At first glance it looks very odd that the negative bars are so much bigger than the positive even though the total is 1%, but of course the negatives are percentages of much smaller numbers so this is to be expected.

“The other odd thing is that it comes down to only 1% difference, implying personal tax and benefits are largely breaking even; presumably other taxes cover all other spending. Although with council tax in there but local services excluded, that is also odd. In fact, the more you look at this the more you realise what is not included, at least in the way of benefits… but it’s a start.”

You must be logged in to post a comment.