We talk a lot about taxing the rich – and perhaps we should. The rich become rich by operating in a system that the state enables. And the contention that taxation amounts to a deprivation of their money

is internally inconsistent. The rules of the game at which the rich win include a price to play. I cannot opt to abide by the rules that benefit me – but not the rules that don’t. No one forces me to accept the offer of my neighbour on the left to give him half the plums I collect from his tree. But if I do the half he gets were never my plums.

But this ineluctable logic can’t be pushed too far. Not if my neighbour on the right also has a plum tree – and he’ll let me keep 60% of the plums I harvest. Not if I decide that if I only get to keep half it’s not worth collecting the plums at all. And not if I took the view that, if I vault the fence in the dead of night, I might get to keep all the plums.

These ideas – and others – are all expressed in a relationship we call the Laffer Curve. We call it that wrongly, and uselessly too. Wrongly, because there is no one Laffer Curve. And uselessly, because no one knows what it looks like.

Here’s a Laffer Curve for income tax.

What it shows is (1) that if you have a tax rate of zero, you don’t yield anything. Few would argue with that. And (2) if you have a tax rate of 100% you also don’t yield anything because no one works and so no one pays tax. That’s slightly more tendentious: there’s always someone who so loves his job that he would carry on even if everything he earned went to the state. But let’s press on with the argument – leave Tax QCs to one side for the moment – and assume that at tax rates of 100% no one would work.

The logical consequence of these two propositions is that there is a rate more than 0% and less than 100% at which the tax yield is the highest – what we call the ‘revenue maximising’ point. Set tax rates too low and Government relinquishes more plums than it must. Set it too high and your taxpayers may defect to your neighbour, not bother at all, or be heavily incentivised to find ways to dodge your plum tax.

This is a basic – but incredibly important – insight.

It explains why there is a point beyond which raising taxes is counter-productive (in revenue raising terms anyway) for Government. It explains why, if the aggregate earnings of everyone in the country is 100 taxing them at 20% might raise 19 but taxing them at 80% won’t raise 76. It explains how Ed Miliband’s Labour could argue that cutting income tax from 50% to 45% was a £3 billion tax cut for the wealthiest; the Coalition could respond that it would only cost £100m; and (on the best available evidence) they could both be right.

It’s also a useless insight. Of course, if your neighbour could work at what this rate was he could maximise the amount of plums he got to keep.

But he can’t. Tax theoreticians on the right argue a Laffer curve looks like this.

They argue that high tax rates disincentivise work, stimulate emigration and generate tax avoidance. And they’re right. They also argue that tax rates reduce economic growth – reducing the number of plums on the tree (loosely speaking). And they argue that the consequence is that the yield maximising rate is a low one.

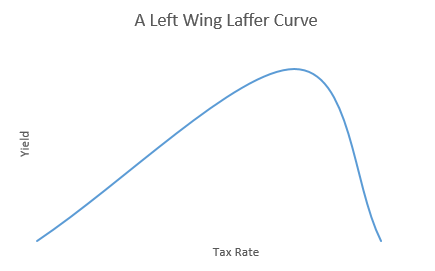

Those on the left argue for one that looks like this.

They agree high tax rates can disincentivise work, cause emigration and tax avoidance. But they argue these effects are overstated and that higher tax rates need not stunt growth. You can push tax rates much higher, they say. And they argue that those who can afford to pay more tax should do.

But this debate rarely rises above assertion and counter-assertion. Because what we know about the shape of the curve is precisely nothing.

We know that today, with our top rate of tax at 45% on income above £150,000, the 332,000 who earn above £150,000 will pay about £49.1bn in income tax in 2015-16 (Table 2.5 (2015-16)). But we don’t know what the world would have looked like today if, for example, Government hadn’t decided to raise our top rate from 40% in 2010-11.

Would there be more (or even fewer) than 332,000 people with income of above £150,000 paying income tax in the UK? Would they be earning more or less in aggregate that they do now? Would they have engaged in more or less tax avoidance? Has a 45% rate had a negative impact on economic growth – or more accurately earnings growth – or more accurately still earnings growth amongst very high earners? What are the effects of that increase on those earning below £150,000? We can speculate on any one of these effects. But unless we can speculate accurately about all of them – and we can’t – we can’t answer the question whether Government receives more in income tax now than had it stuck with a 40% rate.

We can’t construct a sensible counter-factual for the world as it might have been. And nor can we construct a sensible counterfactual for the world as it might be if we were to change rates tomorrow. But from the discourse on the left and right you’d be forgiven for thinking we could.

Here the left’s spokesman du jour Jeremy Corbyn:

Fair taxes for all – let the broadest shoulders bear the biggest burden to balance the books.

He might be right that the broadest shoulders should bear the biggest burden (and in a sense they already do: the highest earning 5,000 taxpayers pay a total of £9.43bn in income tax, or more than 5.5% of all income tax receipts). But it’s a non-sequitur to assert that raising taxes will balance the books, indeed if you tip into the downward slope of the curve you’ll further unbalance them.

And it bedevils much thinking on the right too – here’s Nigel Lawson talking of cutting the top rate to 40%:

I would strongly support this: It would significantly enhance the attractiveness of the UK as a place to do business, at no cost in terms of lost revenue.

That was the experience when I brought the top rate down to 40 per cent in 1988 and it is even more relevant today.

The (let us assume) fact that cutting the tax rate from 60% to 40% was revenue neutral absolutely does not have as its consequence that further tax cuts would be revenue neutral too. (You can test this hypothesis by looking on any Laffer Curve of the effects on yield of cutting tax rates from 20% to 0%).

The IFS’ pre-election estimate of the exchequer effects of raising the top rate from 45% to 50% doesn’t quite fall into this trap:

But it’s important to recognise that HMRC’s estimate from March 2012 (a document that still makes – if you’re of a certain mindset, anyway – for interesting reading) will be of very modest value now. The shape of the curve is affected by a variety of externalities that change over time. The marked success of the Coalition in tackling tax avoidance will reduce what I’ve referred to as dead-of-night fence-vaulting. Put shortly, it will have shifted the revenue maximising point to the right. So too, and markedly, will restrictions in pension tax relief for high earners. But the Coalition also adopted other tax measures which will have shifted the point to the left. And that’s before we move on to effects external to the UK.

I stress these points because they’re what I find most interesting. The political potency of the inequality narrative won’t diminish any time soon. And so the question whether to change income tax rates will continue to find its answer in political rather than fiscal considerations. Nigel Lawson knows this, of course. As (one imagines) do Corbyn’s advisers. Both are embarked on what virtue signalling looks to their respective supporter bases. But it’s no more than assertion: stay sentient folks.

But, as I sought to stress back when I was involved in Labour’s tax policy making, alongside the virtue signalling it’s worth considering how to maximise the yield from changing tax rates. This is a truth that applies to both upward and downward rate change – but I don’t get much sense that many policy makers think like this. Although we can’t know what a Laffer Curve looks like we can still seek to shape it in advance of rate changes. And that’s as universal a truth as you’re likely to find in tax rate policy.

Follow @jolyonmaugham

I feel the biggest problem with the Laffer Curve is that it looks at income tax as if it were the sole means of generating government revenue. But there are plenty of other taxes contributing to the government’s coffers which can only be levied once income tax has been deducted.

For instance, if VAT was applied evenly to all goods and services at (say) 25%, then the government could drop the 20% basic rate of income tax entirely (the extreme left of the curve) without losing much revenue. The reason is that the untaxed portion of people’s income is also taxed whenever it is spent into the economy. So the focus on the ‘ideal income tax rate’ alone paints a misleading picture of the government’s actual tax raising capabilities.

The same is true in any debate about corporation tax. A corporation may pay very little corporation tax (20%), but use the saved money to make a dividend payout (taxed at 30-something percent). The question should be less about whether a particular tax rate is at the optimal level, but rather about which tax should the government be encouraging people to pay.

I’ve written here about a Laffer Curve for income tax – because I’m interested in the relationship between politics and tax policy. And income tax is especially political. But for that, the post could as easily have been written about a Laffer Curve for VAT or corporation tax…

What both sides of the argument – and even you here with a call to tax ‘the rich’ is blur the line between wealth and income. There are many people in this country who have accumulated a lot of wealth, but have paid minimal tax on that accumulation. Whereas those who are of a younger generation, even those in the 40% bracket, will struggle to get anything close to as much wealth unless it is passed to them as inheritance.

It’s very irritating that Corbyn has focused on high earners rather than the wealthy, which is where I think the debate needs to be. But perhaps we should not expect anything else given his constituency.

A wealth tax is of course a rather different question. It’s one that Richard Murphy, who of course advises Corbyn, has spoken in support of. The idea of replacing part of the income tax burden with wealth taxes is one I am interested in too.

The counterfactual surely lies in history: in my lifetime we had income tax rates in the nineties without the economy grinding to a halt. As George Harrison had it, #let me tell you how it will be: there’s one for you, nineteen for me…

It might not have ground to a halt – but was revenue maximised? Plus, as I observed here https://waitingfortax.com/2015/09/03/jeremy-corbyn-and-pensioners/ (of 60% rates): “The UK is no longer in the 1980s when personal income tax rates hit 60%. The make-up of our economy, the shape of our tax burden, the mobility of our highest earners, all of these things have changed. And changed in a way that makes it less rather than more easy to impose higher rates of tax on the rich.”

Your discussion of the Laffer curve seems to assume that the behavioural responses which reduce the yield are entirely negative for the economy (working less, migration or tax avoidance) but there are also possible positive responses. If a higher tax rate reduces the incentives for people on high incomes to bargain for higher pay raises then this could be a positive as an economic rent is eroded making the economy more efficient. This could also have positive distributional effects. There is some evidence that this is the case including the link between top tax rate and pre tax incomes of the top 1% and lack of a link between top tax rates and growth as well as micro evidence of economic rents (see more on this here: https://www.equalitytrust.org.uk/course-correction-pre-distributive-case-50p-top-income-tax-rate-0).

But as you say it’s impossible to know from our current position how large these effects are or where they occur in the UK. There’s considerable reason to be sceptical about the role of the top tax rate in deficit reduction. But I’d argue that this doesn’t mean that it shouldn’t be part of a wider discussion as a tool that can shape behaviour and has the potential to curb economic rents.

Thanks.

There are all sorts of value judgments inherent in whether the tax maximising point should be the target. There are arguments, typically from the right, that there is some morality inherent in low tax rates. And also that the growth maximising point is more important to (and different from) (and to the left of) the tax maximising point. These arguments are, of course, disputed. And then there are perspectives, like yours, that post-tax income equality is itself a positive, and that higher tax rates can be growth enhancing. This latter point – which was once analytically ‘out there’ – derives some support from recent OECD and IMF analysis. Although your perspectives, too, are disputed. I wanted to deal in this post with a slightly narrower point – but of course I recognise that there are other important debates about whether we ought even to be trying to hit the top of the curve.

Well I suppose this is the point – the Laffer curve exists, but is hard to define at best and is not even static. There will be different curves for different taxes, different times and even different people (as you say, some people might be willing to work even at 100% tax rates).

Moreover, each Laffer curve will interact with other variables (other taxes, benefits, lifestyle choices etc) which makes an individual and precise definition near impossible.

That does not make them irrelevant, as some like to say. There is enough data available from tax and GDP numbers, and various other interactions, to make an estimate of what a tax change might do. Importantly what it will do to tax AND GDP, given the two are inextricably linked. It’s not an exact science, but is far better than trying to make changes in a vacuum of information, with no idea on what the effects may be – which feels exactly what Corbynomics is doing.

But surely the point is that they are all interrelated – looking at the curve for one tax tells you little about the overall tax take.

That’s fair. I think these disagreements are also a further reason why (as you say) talking about the tax rate in terms of the Laffer curve isn’t that useful. Whether the tax rate increases avoidance, migration, or bargaining are all separate things and each depends on the wider structure of the economy. Even if you are focusing on yield the laffer curve (as an idea) isn’t helpful unless you know more about these responses and how high likely they are in the current economy. It makes sense to focus on those rather than the idea of an overall laffer curve.

I think that’s fair – and I agree.

There is a relationship between top rates of income tax and top pay though, which is borne out by facts and experience of the last 40 years or so.

We now know top rates of tax have fallen massively over the last 40 years at the same time as top pre-tax pay has soared. Whether the relationship is causal or merely correlative may be moot.

Whether increased top people’s pre-tax pay can be justified as a reward for increased productivity is also moot. Some commentators consider the additional rewards as (unjustified) rent extraction.

If there is a causal relationship, then a valid conclusion is that top rates of income tax should be hiked massively – not to raise more revenue but to combat rising inequality. Combating inequality this way makes Laffer irrelevant.

Whether increased top people’s pre-tax pay can be justified as a reward for increased productivity is also moot. Some commentators consider the additional rewards as (unjustified) rent extraction.

If there is a causal relationship, then a valid conclusion is that top rates of income tax should be hiked massively – not to raise more revenue but to combat rising inequality. Combating inequality this way makes Laffer irrelevant.

That seems a strange argument. Some people are making out like bandits, so the Government should get a share so it can too?

Perhaps it would be more sensible to fix the actual problem, if there is one. More influence by shareholders on executive pay, for example, or forcing the BBC to pay its ‘top talent’ less, or whatever you think the problem is.

I’m not sure this is a very strong argument – it only looks at things in a very one sided way (inequality bad, tax only solution, so raise taxes). Inherently it’s a lowest common denominator approach.

However, it misses the point that high taxes can be bad for growth – and economic growth can be a massive factor in reducing inequality (especially in poorer nations).

So you have to somehow balance the two – and you need some idea of where the Laffer curve(s) are to be able to optimise that equation.

“If there is a causal relationship, then a valid conclusion is that top rates of income tax should be hiked massively – not to raise more revenue but to combat rising inequality.”

Why is that a valid conclusion?

Is the argument that ‘hiking’ taxes massively is some sort of social mission which is justified no matter what the result? OK, we do that. Some people might stay, some people might leave the UK, some people might stop working but you’re arguing that this is worthwhile no matter what the outcome just to end ‘inequality’?

In the 1970s the top 1% of earners paid around 11% of all income tax. Today they pay around 30% of all income tax. You chase them away to solve this terrible inequality problem and you’re looking at quite a tax gap to fill.

Quite honestly I’d rather have a boss who quadrupled his salary whilst doubling mine than one who halved his and cut mine by 25%.

If inequality of incomes is higher than it’s ever been isn’t also our standard of living? Would you rather it was 1915 and we had more ‘equality’ of income and a life expectancy of 52 years or 2015 and this ‘terrible’ inequality and living conditions better than we’ve ever had and an extra 30 years of life to look forward to?

@Andrew C

“Quite honestly I’d rather have a boss who quadrupled his salary whilst doubling mine than one who halved his and cut mine by 25%.”

That is not what is happening though,is it? Wages are falling for the rest of us while top wages are soaring.

“Is the argument that ‘hiking’ taxes massively is some sort of social mission which is justified no matter what the result? OK, we do that. Some people might stay, some people might leave the UK, some people might stop working but you’re arguing that this is worthwhile no matter what the outcome just to end ‘inequality’?”

@Andrew C

You’ve missed my point. My conclusion was based on a suggestion that top pay is not earned. Or to put it more simply, top people are extracting value from firms without creating equivalent value for either the firms or the economy. We are all the poorer for it. Taxing the rent would be perfectly sensible under these conditions.

@Tyler

Inequality is just when it arises from proper functioning markets (or so the theory goes). The point I made was that top peoples’ pay may not arise from a properly functioning market. Directors and other top people effectively set their own pay – they are not price takers like ordinary workers.

So there is a real possibility that the extraordinarily high incomes of directors and their ilk do not correlate with extraordinarily high productivity. If this is the case, then growth won’t be damaged by increasing tax on top incomes.

High taxes can be good for growth too.

@soarergti

The point I made, which is supported by others, is that low tax on high incomes is a cause of inequality. So taxing high incomes is a fix.

Hi MsJones – I understand – your concern is principally about inequality of outcome. It is not a concern I much share – equality of opportunity is, in my view, more important.

So, would you want to reduce all incomes – including those of successful entrepreneurs, musicians, sports people, artists, authors, trade union leaders, ex-EU officials etc. etc. or is it just directors in companies who need taxing to the hilt for the sake of equality?

@soaregti

My concern is for distributive justice – not equality of outcome. Those who put into society and who are price takers should reap just rewards.

Those who are price setters and who take out more than they contribute should be taxed highly on that part of their income which constitutes rent. Highly paid directors fall into the latter group.

I cannot see why some do not appear to accept that high income tax rates (and, even more obviously, capital gains tax rates) do not become counter-productive for aggregate tax collections. Many might not recall the 1960s & 1970s when cash pay was very highly taxed leading to a (mainly undesirable) proliferation of more lowly taxed benefits such as company cars. I used to advise some SMEs and I have no doubt that one of the principal drivers behind both bonuses and dividend payments have invariably include the additional income tax (& NICs in the case of the former) becoming payable. Even without Arthur Laffer, it not difficult to see that the tax authorities will collect far less in aggregate if even a small percentage of such taxpayers decide not pay a bonus or dividend because of the additional taxation which would arise.

I don’t think it’s wise to pick very specific examples are you have done – highly paid directors are still few and far between (and pretty mobile for tax reasons).

You really have to look at the general population. The 40% tax rate comes in at just over 42k a year, which isn’t a huge sum of money. What would happen to the vast numbers of workers on these kind of salaries if that tax rat started shooting up? Which is the kind of tax increases you would need to push through to dramatically alter government receipts.

I have to say, in all the economic literature I’ve seen and read, high taxes tend not to be a particularly good thing for growth. People tend to use the Nordic countries as an example where high taxes have worked, but if you look at them they tend to be highly liberalised economies (with lots of privatised services) with fairly homogenous populations (so inequality was low to start with) and even then as the tax burdens have increased growth has tended to slow.

It strikes me that there is another fallacy at the heart of the Laffer Curve which is illustrated by the absurdities of the extremes at either end. In a 100% tax society, high earners would still presumably find a way to eke a profit, for example by deducting their salaries from corporate profits or by living large off other tax-deductible expenses. That is, the Laffer Curve (as posited) assumes that the rate of tax set by the government is the rate at which tax is actually collected, without possibility of tax avoidance. Conversely, at the other end (0% tax), presumably a society without any government services, there would be all sorts of costs to the individual for private security, fire protection, private education, etc., meaning that the individual would not reap all the benefits of 0% tax anyway (since at some point it is presumably more efficient to have government perform at least SOME services, unless you take libertarianism religiously).

Fully agreed. As somebody who is very much into the higher rate band but still struggles to pay rent and live in London as it is – I would be very unhappy with further tax rises. A large part of the differences in outcomes are about wealth inequality (which changes access to schools, etc), not necessarily earnings. At the last election we had what seems like a very sensible proposal of a mansion tax – yet was opposed by supposed left wingers including Diane Abbott.

A couple of points: 1. As Tyler says above “Well I suppose this is the point – the Laffer curve exists, but is hard to define at best and is not even static. There will be different curves for different taxes, different times and even different people (as you say, some people might be willing to work even at 100% tax rates). Moreover, each Laffer curve will interact with other variables (other taxes, benefits, lifestyle choices etc) which makes an individual and precise definition near impossible.” That’s true enough, as it’s not so much that there is a level of income tax beyond which people will stop working, but a level beyond which people will start seeking with greater intensity to stop paying it. Balloon-squeezing occurs first, as for example the reward of one’s labour is taken as capital rather than income, or in non-monetary form, or deferred as ‘investment’ where this will result in payment of less tax now. So income tax yield will increase less than a simple function of increase in rate would suggest, but on the other hand capital tax yield will increase (though by a lesser amount than the hoped-for income tax yield). 2. Ian’s suggestion of considering extremes is right too. It might be thought that a 100% tax society cannot exist, but in practice something like that happens in a wholly collectivised economy where all of what is produced belongs to the state. The experience of ‘communist’ systems in the 1950s, 60s and 70s suggest that on the one hand this can be attempted, but on the other that it will not succeed. 3. Putting the two together, it is interesting that the total tax yield as a share of GDP has moved within a fairly narrow band for the UK for many decades, at roughly a third of GDP, despite all sorts of tax changes on top of all sorts of societal changes. But in some other countries tax is a distinctly higher share of GDP and has proved sustainably so. This suggests that the actual revenue-maximising point is a function not so much of tax systems but of democratic choice and the willing collective acceptance of a particular tax burden in return for a particular level of provision by the state. But where that ‘social compact’ is not shared by a significant part of the population (significant in terms of tax-paying potential rather in terms of number of people) then tensions and difficulties can arise.