Here’s what the FT reported this morning:

Ouch. That doesn’t sound so good. More tax cuts for multinationals must be the answer, right?

That’s what you’d think from the responses from Government:

But is that really what the KPMG ‘league tables’ show? Do we really need “further improvements” (for them, that is. You and I would probably describe it as collecting even less tax from multinationals)?

Here’s the KPMG Survey. It has lots and lots of questions comparing our ‘tax competitiveness’ with that of other nations. And business is asked over and again what would help our ‘tax competitiveness’. And they have lots of suggestions which result, unsurprisingly, in them paying less tax.

But when I take my three daughters into an ice-cream parlour and ask them whether they’d like ice-cream they tend to say yes. There’s not a single question in the KPMG report which seeks to assesses whether those tax breaks are in any way decisive of a decision to invest here or not.

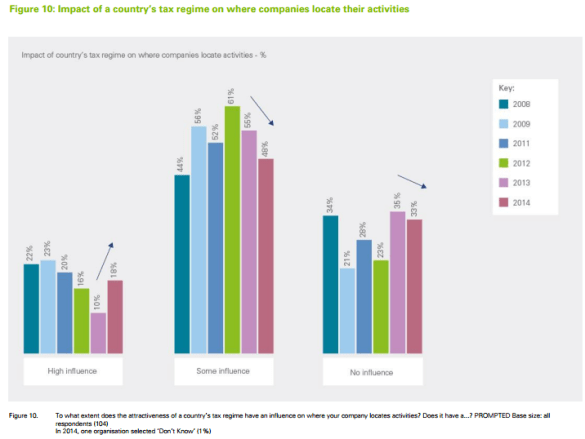

This is close as the reports gets:

You’ll note the tiny sample size. You’ll also note that “high influence” is counted together with “some influence (and is not disaggregated). It could perfectly well be – indeed I would guess – that the number saying it has “high influence” is lower than the number saying it has “no influence.”

You don’t believe me? Well, here’s what the selfsame KPMG survey showed in 2014 (where they did disaggregate ‘high’ and ‘some’):

In 2013, the number saying the tax regime has “no influence” on where they located their activities was a staggering 350% of the number saying “high influence”.

And the report contains no analysis at all of the costs and the benefits for us as a nation of cutting the tax burden on business.

You see, at 20% we already have a corporation tax rate which is by far the lowest in the G7 and the joint lowest in the G20. Those other G20 nations with a 20 per cent rate? Russia, Saudi Arabia and Turkey. And are there really businesses contemplating setting up in Saudi Arabia who might be induced to set up here instead with a 2 per cent cut in corporation tax?

Nine years ago the rate of Corporation Tax was 30 per cent; today it is 20 per cent. In his 2015 Budget Osborne announced plans to cut it further to 18 per cent. That cut alone will cost £2.5bn in its first year. And that’s not my number, by the way. It’s HM Treasury’s own number – you can read it at Table 2.1 here. So “tax attractiveness” carries a very meaningful cost.

And the effect on Foreign Direct Investment in the UK – not the only measure of success, granted, but perhaps the one most applicable to the KPMG survey? Here’s the ONS’s chart.

In 2005, our rate of corporation tax was 30%. As it was in 2007.

You might think the KPMG report is a naked pitch for business to pay less tax. Dressed nicely for dinner, for sure, the better to be able to engage policy-makers and the electorate. And journalists. But still, just a pitch.

What do we actually get for foregoing the tax revenue – the “further improvements” described by Treasury? The effects of the greater “tax attractiveness” described by KPMG? And is it worth it?

We have no idea.

Follow @jolyonmaugham

What’s striking is that the FT spouts this KPMG claptrap without a dissenting voice. For a proper understanding of the ‘competitiveness’ of nations means, see what leading world thinkers make of it http://foolsgold.international/faq/what-is-competitiveness/

It’s astonishing how . . . oh, I’ll stop raving and go and have a cup of something calming

Pingback: Tax Research UK » The UK’s tax competitiveness

I would assume that those saying that tax has ‘no influence’ don’t have any choice as to where they locate their activities. If you do have a choice I can’t see how you could possibly *not* take it into account.

But I don’t believe the ‘high influence’ numbers either. Of course people will say that if asked but in reality tax is just one of a very long list of factors that drive these decisions, and it’s rarely near the top.

Gosh, I wonder why FDI fell off a cliff in 2007-8.

I also wonder why the last Labour government reduced the rate of corporation tax from 30% to 28% in 2008, and indeed why one of the first acts of Gordon Brown in 1997 was to cut the rate from 33% (which it has been since 1991) to 31%, and then to 30% in 1999.

(Just for historical interest, the rate was 52% until 1982, and then dropped precipitately to 35% in 1986, and then bobbed along in the 30% until …)

I remain to be convinced that these changes to the corporation tax rate are that significant in terms of overall competitiveness. Successive chancellors have linked cuts in the rate to various base broadening measures e.g Nigel Lawson’s phasing out of first-year allowances; Gordon Brown’s attack on the leasing industry; and Osborne’s further restrictions on capital allowances as well as the bank levy and changes to North Sea taxation.

More relevant in competitiveness terms are the abolition of ACT (because of EU law); the exemption on inbound dividends, the lack of outbound dividend withholding and the substantial shareholdings exemption. These factors have made it much simpler to set up significant UK international holding company operations…..with taxpaying staff to match. Twenty plus years ago, the UK was a poor location taxwise for such activity. So I can see that in this respect the UK has attracted some business and tax revenues which it would not otherwise have secured.

Pingback: Nicholas Shaxson: Why “National Competitiveness” is Like Ice Cream | naked capitalism

Pingback: This isn’t how I want society to be run | tormod46