Facebook UK Limited – which I’ll call UK Facebook – has published its accounts for the year ending 31 December 2014. Heather Stewart of the Guardian has written about them here. I wanted to add a few points of my own.

First of all, don’t be fooled into believing that these accounts tell you anything about what advertising revenue or profit Facebook makes from UK based advertisers, or advertising targeted at UK consumers. UK Facebook’s business is this:

So its business is providing services to what I’ll call Real Facebook.

Second, UK Facebook could have chosen to tell us a little more about the transactions it enters into with Real Facebook. But, as is its right, it didn’t:

I don’t suggest there’s anything legally wrong in it having declined to disclose this material. But it seems – to me at least – a strange decision for a company whose tax affairs are very much in the public eye. It could have taken the view that its reputation would be better served by transparency – but it didn’t. And people are bound to ask the question, ‘why?’

Third, its accounts show a more than doubling of turnover from 2013 to 2014:

Most businesses’ profitability improves when they double their turnover. But not UK Facebook’s: its pre-tax loss actually increased from 23% of turnover in 2013 to 27% of turnover in 2014. That’s not a feature most people would expect to see in a rapidly growing normal business.

Fourth, another notable feature of UK Facebook’s accounts is its huge staff costs:

These are obviously substantial: as a proportion of turnover they were 82% in 2014. But, perhaps even more remarkably, they are static as a proportion of turnover: in 2013 they were also, yep, 82%. Again, that’s not a feature most people would expect to see in a rapidly growing normal business. You’d expect staff costs as a proportion of revenues to decline as a business increases in size.

Now, the most likely explanation for this is that UK Facebook charges its services – largely consisting of its employees – out to Real Facebook on a cost plus basis. I’m not suggesting that there’s anything unlawful about this. But it does rather imply that UK Facebook may well never make a profit. Because what are described in its accounts as its revenues are really just its staff costs multiplied by a number (here 1.22). And that extra 0.22 may well never be enough to cover office costs, fixed assets and so on.

Certainly that 82% (or 1.22 multiplier) ratio suggests that the UK taxpayer won’t ever enjoy meaningful profits from whatever success Real Facebook enjoys in the UK.

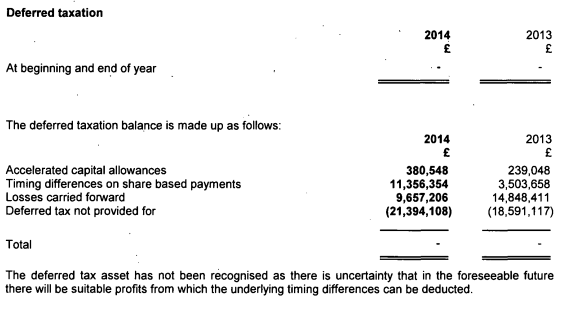

Indeed, that seems to be UK Facebook’s own view. Its accounts set out how it treats its deferred tax assets (basically, the right to set past losses against future profits) and states:

And does UK Facebook recognise deferred tax assets?

It does not.

Finally, Heather’s article is attracting some criticism from the twitter intelligentisa for failing to recognise that, by paying remuneration in the UK, UK Facebook is actually increasing its UK tax liability. That criticism seems to me to be misplaced for a number of reasons.

- Even if you assume that all of the remuneration it pays in the UK is paid to UK resident employees, the net effect of doing so is that its employees acquire an income tax (and modest NICs) liability. And UK Facebook acquires a liability to pay Employer’s National Insurance Contributions of 13.8%. That rate is lower than the rate of corporation tax (likely to be 21% depending on timing) on profits diminished by the payments to employees.

- You want to be careful not automatically to assume that, because the staff are employed by UK Facebook, it follows that they pay tax on their employment income in the UK. For example, if UK Facebook engages staff who are resident in the US, it is the US, not the UK, that has main taxing rights in respect of the income of those staff. So UK Facebook could be depleting its profits chargeable to UK corporation tax by paying salaries to staff resident elsewhere on which salaries no UK income tax liability accrues and which still deplete the corporation tax liability of UK Facebook.

- Moreover, the average staff member enjoys a remuneration package with an average cost to Facebook of £238,000. No one pays their staff that unless there’s pretty vigorous competition for the services of those staff. It’s at the very least very possible that, if Facebook wasn’t paying them here, someone else would be.

In any event, clearly, it’s no defence for X, facing an allegation that it doesn’t pay the appropriate amount of corporation tax, to say: ‘well, I’ve done some other things that the law requires of me.’

Follow @jolyonmaugham

“That’s not a feature most people would expect to see in a rapidly growing normal business.”

I really don’t know about that – can easily imagine circumstance in which a rapidly growing business is investing and growing costs faster than the top line. Amazon! But even bricks and mortars businesses can do that, depends on nature of business.

So, revealing my ignorance, are the prices charged for inter-group services like this not supposed to be based on third party pricing? Don’t see how that fits with cost plus pricing. Also a third party support and marketing services provider is going to charge prices consistent with it making a profit (otherwise it would not exist) so if Facebook is telling a “we are still in early stage growth so costs are outstripping revenues as we build” story, one would hope it cannot keep telling that forever. That is, if I haven’t completely misunderstood how pricing set in this context.

Thanks Jolyon for such a well thought out commentary on UK Facebook’s accounts.

As a chartered accountant may I say that Real Facebook, like so many other multinationals, is just taking the ****?

Forty years ago when as an articled clerk never in my wildest dreams would I have thought that describing a multinational’s tax policy would require the use of a profanity.

The argument that those employees could earn the same elsewhere seems weak to me. Reductio ad absurdum, it implies that anyone who is highly skilled will automatically get their just rewards whether or not any new, innovative businesses decide to set up shop here. I would be challenge you to name another tech firm paying an average salary of £238,000.

That being the case, surely a pragmatist would argue that Facebook brings greater benefit to the UK taxpayer by paying out as much money to its employees as possible. There’s £101k in income tax and employee NICs due per employee earning that amount. Add in the 13.8% employers’ NICs and the total tax paid per employee is £134,118, equivalent to 56% of the salary. Replace any one employee with the equivalent amount in taxable profit and the exchequer gets less than half that amount. Why the obsession with corporation tax?

Facebook UK doesn’t increase ITS tax liability by paying large sums to its employees but, unless those employees are able to avoid tax on their bonuses to reduce those to the 21% which might have been paid by Facebook UK had it not paid, doesn’t this mean that HMG receives more in tax revenue from (Facebook UK + Facebook UK employees) than it would have done?

If that is right, isn’t it better for everyone in the UK? Facebook UK employees get more money. HMG gets more tax revenue from Facebook UK employees and Facebook UK Employers’ NI. Real Facebook gets some benefit to its global position. The only loser is Facebook UK which could have taken the amount it spent on bonuses (less 21% corporation tax) instead and remitted that to its US parent.

Perhaps this is an unusual situation in which the real loser is the IRS in the US but which could in other circumstances be reversed where a UK “Real” company does similar things with its group companies elsewhere so that less is sent back to the UK “Real” company and so its UK tax liability is reduced?

If the company has a loss £28.5m after a share option charge of £35m, then it appears that there’s an underlying profit of £6.5m in there somewhere. It’s not clear from the article whether the £35m is the accounting charge or the tax deduction (it sounds more like the latter), but the conclusion I’d reach is that this is an artifact of a rapidly-rising share price, which gives accounting charges and tax deductions which bear no relationship to the company’s actual performance.

Had the share price remained flat, then there would be no tax deductions for the options and we’d be looking at taxable profit of around £6.5m, so CT of a little over £1.3m (assuming transfer pricing is all fine, naturally). As the share price has gone up, we get PCTCT of nil but taxable employment income of potentially £35m. That would give secondary NI of roughly £4.8m – never mind the income tax and primary NI of what, £14m or more?

That’s a huge boost to the Treasury, which arises because of Real Facebook’s Nasdaq performance rather than because of UK Facebook’s trading results.

Also, on the recognition of deferred tax assets: one is normally very strict about forecasting profits for this purpose. You normally only look ahead one year, so (assuming predictable underlying profits, which seems fair if they’re on a cost-plus basis) to be able to recognise anything you’d have to assume that option exercises in the next 12 months (several of which will have elapsed by the time you sign the accounts) will give no appreciable tax deduction.

That means that either you expect there to be very few of them, or that the share price will be barely above the exercise price (or both). Both of these appear fairly unlikely given Facebook’s share price growth over the last few years.

I think you agree that this UK company is a sideshow and the question is should an overseas company, the Real Facebook, “broadcasting” advertising into the UK over the internet be taxed in the UK on these revenues or any profit it earns thereon. Legally these revenues are made overseas and the UK company is just a local facilitator. If we based tax on the legal entity location or even the physical location of the servers then a company like this will just move either to the lowest tax location. The only way to tax them is to require large internet companies such as these have a license to “broadcast” into a county. The terms of this license could demand revenues are run through a UK company. Unlicensed operators would have to be blocked by ISP’s. Internet freedom campaigners will of course complain against this. I am not saying I support this idea but I have yet to hear a better way to tax cross border advertising revenues on the internet by the country subjected to the advertising.

No, Facebook earns its money by selling adverts – forget where they’re served from. From what I understand there are some very real questions on where the real selling is taking place. EY have as one of their key audit risks for Facebook Ireland that it would be determined to have a permanent establishment in the UK.

Of course, Paddy, there are exceptions. But my statement was expressed as a generality and is entirely true expressed as a generality.

As to your second point, I’m not a transfer pricing expert but I would have thought cost plus was probably accepted as a reasonable proxy for market value. But, yes, unpacking how you charge on a cost plus basis and make a loss might be a fruitful exercise.

Hi Tristan,

As to your first point, it’s basic supply and demand. I’m not arguing they will earn £238,000; I am arguing that it likely reflects the market rate for staff.

As to your second point, you’re dealing with an argument that I haven’t made. But what is pretty clear to me is that Facebook employ staff in the UK because they think it helps them make money. If they do employ staff they obviously have to meet their obligations to deduct tax and pay NICs. And also such obligation as they have to pay corporation tax. Of course it’s a good thing for the UK that they’re employing staff here – but that doesn’t legally excuse any non-compliance with their obligations to pay tax or morally excuse any legal misbehaviour.

Jolyon

Hi Andrew,

I think there are a number of assumptions in your post which look to me to be wrong.

(1) it’s not a share option charge. It’s a restricted share charge (note 16).

(2) you seem to be assuming that the restricted share charge is not a real cost. It is a real cost which reflects the costs of remunerating employees. I don’t think the accounts state how UK Facebook pays Real Facebook for the grant of the restricted shares but in my experience of other cases, sometimes the employing entity cash settles and sometimes it equity settles. The fact that there are only 1000 shares in UK Facebook suggests it hasn’t equity settled.

(3) I’m not certain of this, but I don’t think UITF 32 adjusts the P&L of the employing entity by reference to how the parent entity’s share price performs post grant.

(4) on deferred tax assets, I’ve just applied what UK Facebook’s accounting policy states. What you say is inconsistent with that accounting policy.

Jolyon

it was deemed that point of sale was in UK even if delivery was via broadcast from overseas Facebook would just move its sale team properly offshore and still avoid tax. I suspect they carefully have a system where UK employees “recommend customers” to overseas company for sale to take place offshore.

Hi Jolyon,

(1) I am guilty of loose language, in that I tend to refer to all share-based payments as “share options”. Most people I’ve dealt with concerning them (including HMRC) seem to do so – it’s just a convenient shorthand.

But Restricted Stock Units and share options are treated in essentially the same way for tax purposes. In fact I nearly commented that I was assuming that these would be RSUs rather than options proper, but sadly didn’t bother.

(2) In my experience US firms often don’t bother settling at all. This makes no difference to the UK tax position.

However, I’ve never been happy with the idea that share-based payments are a cost to the company in the first place (and, given the arguments that surrounded the introduction of FRS 20 et al, I don’t think I’m alone here). I’m happy to accept that GAAP says they should be treated *as if* they’re a cost, and I like the symmetry of a CT deduction to match the IT/NI liability, but I don’t really feel that they are a cost to the company.

(3) I’m not sure what you’re referring to here – I don’t think I’d suggested it should?

But the UK tax deduction certainly depends on the share price movements post grant (although not of course post exercise).

The effect is much more pronounced for options (where the deduction could be eliminated if the price falls, or greatly exaggerated if it rises) than for RSUs (where you’ll always get a deduction, as “exercise price” is nil), but either way there’s an effect.

(4) The accounts wording is the normal way this is set out in accounts, but in my experience the normal way it is *applied* is to look a year ahead. That’s not to say that I haven’t seen other bases applied, of course, but auditors can be relied on to complain if you try to do so without some good justification.

But “there is uncertainty that in the foreseeable future” is exactly what I said, if you take “the foreseeable future” as being one year (which is the norm in my experience), and “uncertainty that.. there will be suitable profits” as meaning that the RSU deduction may well exceed underlying profit (which seems likely given the position this time)

I follow and agree with your analysis Jolyon except on one point.

The rate of employers Nic may be lower than the rate of CT but the amount of Employers NIC paid by UK Facebook is going to be pretty high isn’t it? Why does this not get factored into the amount of tax the company pays?

It depends on whether the employee is employed in Great Britain. You shouldn’t assume that they all are. To such extent as they are, there will be an Employers’ NICs liability. I haven’t argued that paying staff more is a UK tax avoidance device.

To be fair, if you run that argument then it may also be that there are UK employees not paid by UK Facebook, in which case there may be a secondary NI liability without a CT deduction.

Jolyon – but has anyone suggested legal misbehaviour or non-compliance with their obligations to pay tax?

I have to admire your consistency, Maya, always eager to ensure that all arguments for big business are put when it comes to tax.

I think my views are pretty plain. I said in my post, several times, that I wasn’t saying that Facebook had done anything wrong. Tristan was putting the argument that if you aggregate income taxes they are higher than corporation taxes – and asked why the obsession with corporation tax. I heard the echoes of an oft advanced argument that we can forget about corporation tax misbehaviour because business X has a high total tax contribution. And I was advancing the point that it’s reasonable to expect of businesses that they comply with all relevant laws (and, although I mis-phrased it, with moral obligations too if theyd like to avoid moral criticism) not just some of them. I think that was a reasonable point to make by way of response.

Just looking at the income statement for Real Facebook, it looks like they are paying a global effective tax rate of about 40%, consistently year on year. That’s just under double that of Apple and Google, famed users of those structures.

Now, clearly having zero UK profit is bad for the UK tax take. But could it be that Facebook actually isn’t using these structures, and the UK profit is simply the correct interpretation of transfer pricing rules as they stand (which can cause some odds results)?

After all, if Real Facebook is going to be paying US tax on the money paid to it by UK Facebook (and based on its high tax rate, it doesn’t seem to be sheltering cash tax free offshore), it’s probably doesn’t care how much UK corporation tax it pays.

UK corporation tax is a tax on profits, not turnover. Are we supposed to be surprised when a loss-making company pays little or no corporation tax?

If the implication is that the company is recharging staff costs (but apparently not other costs) at cost plus 22%, then surely the real question is whether that marked-up amount represents a proper arm’s length price for the sales support, marketing and engineering support services that its 360-odd UK employees provide. I’m sure HMRC is giving proper consideration to whether comparable uncontrolled prices exist or whether profit splitting methods might be more appropriate.

It was a simple question of clarification. I agree I can’t imagine anyone would seek to excuse legal non-compliance in one area by saying ‘but they comply with some other law’, so I wondered what you had in mind in that scenario (and why you were bringing it up, as there doesn’t seem to be a question of non-compliance here). Nevermind. If I was after belittling personal commentary, there are other tax blogs to go to for that kind of thing.

The whole total tax contribution debate – don’t look at the corporation tax we pay, look at the vat and the NICs and the tax our employees pay – is predicated on something embarrassing (usually reputationally/morally) in the corporation tax return. Im surprised that you you weren’t aware of that given your close interest in the field. But I’ll apologise when you direct me to some of your writing where you seek to hold big corporations to account – not just those who themselves seek to hold big corporations to account.

Indeed. If you assume for the sake of argument that Facebook is artificially shifting profit out of the UK in order to reduce its tax bill, then a couple of observations spring to mind:

1) Shifting to the US is a poor decision: you’re taking profit from 20% tax to 40%. For it to be effective we’d need to identify the low-tax jurisdiction that they’re moving the profit to.

2) They’ve over-egged the position. A loss in the UK does not reduce the profits taxable elsewhere: for each £1m shifted which makes a UK loss, you get tax (at whatever rate) where the profits are recognised, which is an actual cost, and a deferred tax asset in the UK which is worthless. Even shifting profits to Ireland would be counter-productive.

3) The results speak for themselves: if Facebook are trying to manage their tax down, they’re doing really badly at it.

4) This suggests to me that if Facebook’s transfer pricing policy is biased at all, it is aimed at keeping the IRS happy even if this comes at the expense of other jurisdictions.

But I don’t see any particular reason to suppose that there is profit-shifting going on. It looks to me simply as if Facebook has a very generous RSU scheme which is paying out a lot due to the share price. As a result value is being shifted from the company to employees, and the tax position reflects that.

How is the IRS a loser? If JM is right with his clear inference that Facebook UK is undercharging Real Facebook, then that means profits of Real Facebook are higher than they would otherwise be. If Real Facebook is in the US (which it may or may not be) then the IRS is actually receiving more tax due to the transfer pricing mismatch.

I suppose it could be if Real Facebook is being charged the right amount by Facebook uk but not receiving as much profit from Facebook uk as it “ought” and thereby having less profit to be taxed by the irs.

It might be that actually there is no loser. If there’s no loser I’m not sure Facebook can be criticised.

So, Facebook in the UK has, apparently, broken no laws, observed all regulations and has flouted no requirements.

Yet in The Guardian, on R Murphy’s blog and here, it is said to be ‘facing an allegation that it doesn’t pay the appropriate amount of corporation tax’.

Next time Labour complains that people think it is anti-business, we shall have all the evidence we need to prove the charge.

I think you’ll find Osborne described tax avoidance as “morally repugnant”. But don’t let that get in the way of a good rant, will you?

He probably did. But he is in a position to change the law, should he so want. He has even less cause for legitimate complaint than you do.

If he, or you, want a change in the law, then he or you should tell us what, in his or your opinion, that change should be. Until then, people or corporations following the law should not be facing ‘allegations’ without some proof of substance to them.

Most of the changes I have seen proposed would require leaving the EU (or at least dismantling the single market) as a starting point. Not many who campaign on this issue want that, so exactly what is it you, The Guardian, Mr Osborne and Mr Murphy want changed in the law as it stands?

So you accept you were wrong to suggest it was only an issue for the Labour Party?

I didn’t ‘suggest it was only an issue for the Labour Party’.

Still wondering what changes to the law you would like to see, if you regard the Facebook situation as unacceptable though.

But where’s the avoidance? Where is there any evidence that the tax charge is lower than it “ought” to otherwise be? Yes there are companies out there engaging in immoral tax avoidance, but is there anything to suggest that this is going on here?

sure, I expressed myself poorly on first point. I mean it’s normal enough not to be a warning flag.

(although this is moot as on further reading turns out UK arm was profitable and only paid no tax because of rolled over losses from previous years)

Could someone tell us non accountants, lawyers etc exactly what FB has done wrong and how much tax they ‘should have’ paid & what laws that FB haven’t broken need to be changed?

Or -just get Murphy to give a figure he thinks is ‘right’ and don’t bother with this legal nonsense.

1) “But it does rather imply that UK Facebook may well never make a profit.”

As you say, that’s because Facebook UK’s business model is cost + engineers.

I know and have acted for lots of companies that have never made much of a profit as they pay out what would otherwise be taxed at 20% CT to their employees where it is taxed at anything up to c53% if you include employers’ NIC.

Is that in itself really a concern?

Both you and other commentators basically seem to be saying “I’m not saying Facebook has done anything wrong but LOOK at what Facebook is doing!!”

2) “Most businesses’ profitability improves when they double their turnover. But not UK Facebook’s:”

Could you cite your evidence for that first bit or is it just something you have stated without evidence because it supports your argument and sounds a bit ‘fishy’?

As to your 1) I’m glad we agree that UK Facebook may well never make a profit. The reason I made the point is because many people may have formed the impressionism that the present state of affairs was a temporary thing connected with the fact that Facebook is an early stage business. But the state of affairs is, as we both agree, a likely function of the nature of UK Facebook’s business model.

As to your 2) my proposition is absolutely self-evident. And if you weren’t blinded by your desire to defend Facebook you’d accept that as true as well.

in my experience cost plus is a fairly common standard for consulting transfer pricing. I have been involved in a couple of companies with a similar structure and they all followed similar rules. The aim is usually to break even to be honest.

You have to remember that there is another jurisdiction at the end of these costs. The jurisdiction of the main entity usually takes a dim view of profits in the off-shore subsidiary. In one case the cost margin had to be reduced after the tax authorities complained the margin was excessive. Keeping tax authorities in the main jurisdiction happy is usually the priority, it’s not so surprising.

Wherever Facebook conducts any economic activity in the UK is not so obvious to me. Most of the value must be created in the US, where all the development is done. You could draw a parallel with ITV for example. Some significant percentage of ITV UK revenues gets paid to US movie and TV show producers. Facebook Ireland surely has a similar relationship with Facebook US.

Pingback: A further note – on Real Facebook’s Accounts | Waiting for Godot

Just going back to your CT vs NI point:

– If Facebook makes a £1 profit in the UK, it pays 20p of CT.

– If it shifts that profit to employees, it pays only 13.8p of secondary NI.

That is fair enough: less tax is paid.

But you also have to take into account that by shifting the profit out to employees, Facebook also pays out the underlying £1.

If it keeps the profit and pays the CT, Facebook is 80p better off as a result of that profit.

If it shifts the profit to the employees and pays the NI, Facebook is actually 13.8p worse off overall than it was if it hadn’t made the profit in the first place. It loses 93.8p on the deal.

(Unless of course the RSU scheme allows the NI to be shifted to the employee, in which case Facebook suffers no UK tax, but is still missing the profit – it’s only 80p worse off as a result of the profit shift, not 93.8p).

Focusing on tax rather than looking at the value movements is often misleading. I’ve lost count of the number of clients who suggest making charity contributions, for example, who only notice the 40p tax saving and not the £1 it costs them to buy it.

Fascinating article. Thanks.

So basically the problem is what most people think Facebook UK’s business is, is in fact not what facebook UK’s business is.

I assume most people think Facebook UK is responsible for facebook’s revenue from UK users i.e. its value of selling ads to all British users.

But actually its revenue comes from charging its staff to Real Facebook and has nothing to do with how Facebook in general actually makes its money.

Hence Facebook UK’s tax liability has pretty much zero relation to how profitable Real Facebook actually is.

That’s certainly one – fairly significant – issue. And yes.