The release by UK Facebook of its accounts made some media noise. Heather Stewart of the Guardian covered them here, Richard Murphy here, Vanessa Houlder here, Hugo Rifkind here and your present correspondent observed that UK Facebook was unlikely ever to make a, or a material, taxable profit here.

Most – with a couple of honorable exceptions – of the twitter taxperts rallied round UK Facebook. A number of bad points were taken in its defence – and no doubt one or two good ones as well. I would not want to pretend – for it is a long mile from true – that I have any monopoly on insight.

It does surprise me that this is the invariable and knee-jerk reaction to stories asking whether Big Business is misbehaving. Although not quite as much as it surprises me that many taxperts don’t understand that the consequence of their myopia is poor understand of tax issues: journalists don’t feel able to call on experts that they can’t trust to tell the unvarnished truth. This is a real bugbear of mine: I’ve written about it (in two addresses to my colleagues) here and here. As I put it in the first of those two posts:

Here’s a short prescription. Rather than bemoaning the limited understanding of public and media, we should work to improve it. I speak to a lot of journalists – several a day – and I’ve only ever spoken to one who wasn’t interested in the truth.

But we need to be transparent about the premise from which we proceed. When we act in a professional capacity it’s right that we talk our own book. Everyone understands that we sometimes speak as lobbyists. But it’s important to signal when we do. Otherwise we become part of the problem. If we merely stand on the sidelines and criticise, we don’t merely ignore Gandhi’s injunction to ‘Be the change you wish to see in the world.’ We thwart it.

***

Anyway, on to UK Facebook.

One of two points taken in its defence was that you can tell that there is no funny business in its accounts because if you look at the rate of corporation tax paid by Real Facebook on its global profits that rate is really rather high. If true this is a decent point: why would you shift profits out of the UK and into another jurisdiction where you’d pay as high or an even higher rate of corporation tax?

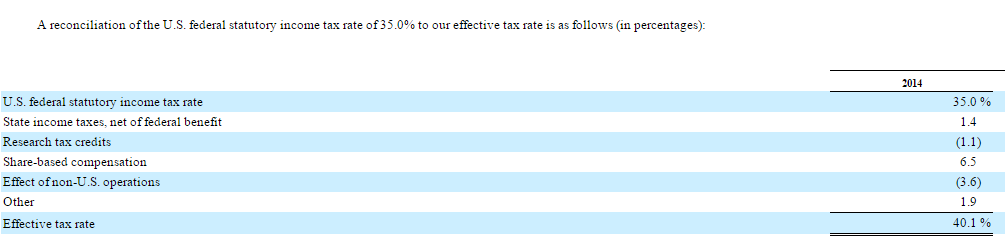

But is it true? Well, at first glance, it looks true. Annex 2A of this document, prepared by the EU Commission, states that Real Facebook paid 45.5% tax on income in 2013. And if you go to Facebook’s own accounts, at Note 13 you find this (and I should note that the accounts refers to income tax which is what our American cousins call corporation tax. For ease of use for my UK readers I am going to call it US corporation tax) :

And this:

They’re probably too small to read on the bus but what they show is that in 2014, Real Facebook made provision for $1.97bn of US corporation tax, an effective tax rate of 40.1% on worldwide income. In 2013, the equivalent rate was 45.5% (hence the Commission figure) and in 2012 it was a remarkable 89.3%!

This surprised me a little because, as the Note itself records, the statutory rate of US corporation tax is 35%. And few of us tax professionals are paid to increase above the statutory rate the amount of tax our clients pay. So I did a little digging.

Not that much, mind. Further down in the very same note you find this:

Excess tax benefits associated with stock option exercises and other equity awards are credited to stockholders’ equity. The income tax benefits resulting from stock awards that were credited to stockholders’ equity were $1.85 billion, $602 million and $1.03 billion for the years ended December 31, 2014, 2013, and 2012, respectively.

So alongside the US corporation tax paid, Real Facebook also received what are shyly described as “income tax benefits” arising from share options (I’ll talk about share options for shorthand although there will be other share based remuneration too) it had granted, of £1.85bn.

Hang on a second: so is the tax provided for by Real Facebook in 2014 $1.97bn (at an effective tax rate of 40.1%) or $1.97bn minus 1.85bn (at an effective tax rate of 6%)?

To find the answer to that question, you need to dig a little deeper.

At page 42 you find this:

2014 Compared to 2013. Our provision for income taxes in 2014 increased $716 million, or 57%, compared to 2013, primarily due to an increase in income before provision for income taxes. Our effective tax rate differs from the statutory rate due to non-deductible share-based compensation, operations in jurisdictions with tax rates lower than the U.S., and tax research credits. Our effective tax rate decreased primarily due to a change in our geographic mix of pre-tax income.

The bit that’s emboldened in that quote was emboldened by me. Now I am not an expert in US Accounting Practice or the US Tax Code. But my understanding is that under US Accounting Practice (and the same is true here) an employer get an accounting deduction when it grants most common types of share option based remuneration to employees to reflect the fact that its incurred expenditure. But under the US Tax Code it doesn’t get a tax deduction when it grants those options; instead it gets that tax deduction later on when the options are exercised. And the amount of the deduction depends on how much the option is then worth.

This timing mismatch has a number of consequences. But in particular, it means that a business with substantial staff costs which costs it chooses to meet in the form of share options will always show a high rate of US corporation tax.

Example. Assume for the sake of example that in 2014 I have income of 100, staff costs of 90 all of which I meet by granting share options of that value, no other costs and the rate of corporation tax is 35%. I will have accounting profits of 10, taxable profits of 100, I will pay tax of 35 and I will have an effective rate of corporation tax of 350%.

But, of course, in the real world, you can’t ignore that, in the future, when those share options are exercised, you will get a tax benefit.

Assume that the options in Example were all exercised on 1 January 2015 at a price which reflected my expectation of their value at the date in 2014 when I granted them. I’d then receive a tax benefit of 35% of 90 or 31.5. That tax benefit would be attributable to my activities in 2014. And if you matched it to 2014 I would have paid tax on my 2014 activities of 35-31.5+ 3.5 and my effective tax rate would be 3.5 on 10 or 35%.

Of course, in practice it’s a little more complicated than this example implies. In 2014 we would show on our balance sheet an expectation of what tax benefit we expect to get in the future (an item called a deferred tax asset) which we would adjust upwards or downwards depending on how closely actuality delivered on our expectations (perfectly in my example, less so in practice). And the tax benefit we got might not be attributable only to our activities in the year in which we got it (it is in my example) but in earlier years too. But these complexities shouldn’t obscure the fact that the tax benefit derives from our activities and reduces the amount we have to pay to the tax authority.

In 2014, Real Facebook made an upward adjustment to its deferred tax assets attributable to stock options of $1.85bn. That figure is not wholly attributable to Facebook’s activities in 2014. But it does reflect share options granted by Real Facebook to its employees – which is a cost of Real Facebook doing business. And it does reflect a 2014 upwards adjustment to Real Facebook’s expectation of tax benefits arising from the grant of those share options. And you can’t ignore it and pretend it has nothing to with Real Facebook’s real US corporation tax liability. And if you match it to Real Facebook’s actual provision for US corporation tax in 2014 it drives Facebook’s effective tax rate down from (an improbably high) 40.1% to (a less surprising, for us cynics at least) 6%.

And the argument that you can tell that there’s no funny business in UK Facebook’s accounts because of the high rate of corporation tax paid by Real Facebook simply evaporates.

***

I said there were two arguments advanced by the taxperts in UK Facebook’s defence. The other is the total tax contribution argument. It is that you shouldn’t focus on the corporation tax paid (or more accurately not paid) by UK Facebook because of all of the other taxes that UK Facebook causes to be paid. In my original piece on UK Facebook’s accounts I said of it this:

The commentariat didn’t think there was any of that going on. Here, by way of example, was one response from a commentator:

I can’t imagine anyone would seek to excuse legal non-compliance in one area by saying ‘but they comply with some other law’…

It’s worth pausing to note that I was making a general observation about how tax avoidance is justified. And that justification certainly is advanced. Speaking yesterday of UK Facebook here Chas Roy-Chowdhury, head of taxation at the Association of Chartered Certified Accountants, said this:

This is, it seems to me, a diversion. The allegation that someone has avoided corporation tax does not seem to me to be answered by pointing to the fact that they comply with other of their legal obligations.

Follow @jolyonmaugham

great post. There does seem to be an argument, which differs from the “but look they also pay NIC” line, which says that by arranging affairs in this fashion, so that they never make a profit because they are always deducting share options that were vested (or whatever right phrasing is) in previous years, actually results in more money for UK than we’d be getting from a corporation tax on a simple revenues equals salary costs plus margin business. I got that from here (and some comments further up)

http://www.timworstall.com/2015/10/14/just-for-posterity/#comment-597643

p.s. I think it’s a good thing that some people “rally round” corporations, or at least question accusations of tax avoidance etc. we need people interrogating claims made by all sides, let’s not beg the question of who is right, those on the ‘tax campaigner’ side do at times exaggerate, get things wrong, easy to see why some people are going to take on themselves role of questioning their claims.

“The allegation that someone has avoided corporation tax does not seem to me to be answered by pointing to the fact that they comply with other of their legal obligations.”

Has anyone made such an allegation? Twice now you have suggested they have, but without making clear what the substance of it is. All the above seems to do is say that the current UK & US rules were followed. So, what is this allegation of which you speak?

There is a more fundamental point though. What do we want companies to do?

Surely, we want them to set-up offices, warehouses and factories in the UK, to produce value-add goods & services we want to use, and which may be exported.

We want them to employ some of the 1.7m without a job, the vast majority of whom would love such an opportunity. The country saves benefit costs, and receives income tax, NI and VAT and all the other taxes they will pay.

We know that taxing something reduces the amount of it we get. Should we not incentivise, rather than penalise, those companies who employ people on high wages as Facebook seems to do in the UK, and encourage more of it. Maybe not by reducing Corporation Tax to zero, but making it so low that it doesn’t put anyone off from setting-up in this country.

This is not simply a tax question. At some point, some companies are going to decide that if they get attacked by campaigners even when they follow all the laws they are required to do, they will suffer less PR damage by simply not establishing in the UK at all.

This does not seem to be an outcome in anyone’s interest, especially not the currently unemployed and low-paid.

Hi,

Are you the same person (posting as Soarer) who has been making false allegations about me over on Tim Worstall’s site? If you are, I think you need to withdraw them before I reply to your post.

Jolyon

I must have misremembered and I unreservedly apologise. I will make the same point on Tim’s site, though I cannot delete the offending post.

Thanks – and for fronting up. Am working on something else but will try and reply this evening.

I think Paddy Carter makes some good points. And I echo Jolyon’s opening words “It does surprise me that this is the invariable and knee-jerk reaction to stories asking whether Big Business is misbehaving. Although not quite as much as it surprises me that many taxperts don’t understand that the consequence of their myopia is poor understand of tax issues: journalists don’t feel able to call on experts that they can’t trust to tell the unvarnished truth. This is a real bugbear of mine.”

I’m not sure if I then agree on a need to be “transparent about the premise from which we proceed. When we act in a professional capacity it’s right that we talk our own book. Everyone understands that we sometimes speak as lobbyists.” If this means being as open as we can about who we are, or work for, that is one thing. But, at the risk of parody, we seem to be in a world where people apply certain tests and filters before engaging with any evidence based arguments. Based on comments on CiF and on Twitter, and exaggerating of course, we can see three layers of filter.

The first is to discount anyone working for a Regulatory body (like HMRC). This can be either because they are too soft on business and big taxpayers, or because they have too many powers, which they use to harass innocent taxpayers and tie them up in red tape.

The second filter is to reject anybody who works for an organisation funded by Trade Union A, NGO B, or accountancy firm C, on the grounds they are hopelessly biased and their funding dictates their arguments.

Then we move to the third, what might be called establishing the witness’ credibility, or the political response. What have they posted before? Do they belong to a pressure group? Have they expressed any support for a politician, or political party, even one outside the UK?

If these tests are passed then people seem willing to get down to examining their arguments. Surely that is, to use a technical tax term, bonkers? Can we not actually look at the facts and apply to them our understanding on how tax and accountancy rules apply, even if it was the Dark Lord himself who was advancing the arguments.

The discussions on FB seem to have started on the lines that minimal CT shows they’re doing something fishy. (It’s the journalists’ mantra of why are these lying b*** lying to me.) But I’m still not clear on exactly what causes the smell.

Is it wrong to make no taxable profits in the UK? Well. We have legislation designed to deal with things like hobby farming, where there is a real loss but it disguises private costs and people try to set them against taxable income.

If a “real” business makes a loss why is this suspicious? If there are offshore payments for IP to connected parties in low tax jurisdictions then clearly there are significant grounds to challenge. But if the business donates all its profits to a charity, are we worried? Probably not if it went to Oxfam but maybe not if it is a small private charity.

Is it a sense that FB has form and so there must some fire beneath the apparent smoke of share options. Is there fire? I never knew there were so many instant UK experts in the taxation of share options, how GAAP and tax rules interact, not to mention American accounting standards, and so on. But having read their analyses I still can’t see the mischief that has “outraged” Guardian readers.

I stand to be corrected but I cannot see how the UK Exchequer has suffered because the options were awarded. Clearly the amount of tax per employee is bound up with their individual circumstances – when they were awarded, whether and when exercised and so on. But share options, unlike say Employee Benefit Trusts, don’t have a reputation for being a vehicle for corporate tax avoidance. So it doesn’t seem that relevant to consider the tax rate payable outside the UK unless you believe that somehow UK taxable profits have been shifted elsewhere. (The normal accusation against large MNCs is that the money goes to low tax countries – not the USA!) But how much and where seem to be unanswered questions.

So, is this smoke without fire?

Correct me if I am wrong, but I think you are arguing that Facebook UK must have got its transfer pricing wrong, as (assuming your analysis is right) it will never make a taxable profit in the UK. The answer to that suggestion must turn on an analysis of what its 300-odd UK employees are doing and how much that is worth for the group.

I doubt any of the esteemed commentators or twitter taxperts are really in any kind of position to know how much profit Facebook UK “should” be recognising. So it comes down to an allegation that HMRC are not being sufficiently diligent in challenging the transfer pricing. Do you really think HMRC can’t be bothered to check what could easily amount to tens of millions in corporation tax?

The premise that it doesn’t matter if you avoid corporation tax provided you create (tax paying) jobs plus pay VAT and NI only works if it creates net new employment/activity. If Facebook is hoovering up advertising spend that would be spent on alternative (tax paying) advertising outlets then what precisely have we gained?

As good example is Starbucks who are able to use tax avoidance as a competitive advantage over onshore rivals. If they left the market you can’t seriously believe that that economic activity wouldn’t be absorbed by their UK based rivals.

I take your point, but if we reduced and simplified Corporation Tax, it should become easier to pay it than avoid it. This will make a more level playing field for local companies as well.

Also, this tax in not a major contributor to government income, being about £40bn out of the total £600bn or so tax take, so around 7%. It does not need to negatively impact much economic activity to quickly become tax-raising negative (as, for example, according to the EU, a Tobin Tax would be)

One of the problems with complex regulation, as is illustrated above around Corporation Tax, is that it pretty easy for major corporates to deal with. They have armies of accountants and administrators. Its a relatively small cost for them.

For an SME, it can be a major burden. The recent changes to VAT rules on digital services (the area where I assist a small number of companies, though in a technical capacity, not tax or accounting), which have been called for by some avoidance campaigners, have made many UK companies think twice about selling into other EU countries. They now have to worry about VAT regimes in every country in which they sell, as opposed to just the UK where they are based. Potentially, where once you had to follow just the UK VAT reporting & regulations, you now have to follow those of all 28 member states. If, as some want, this gets extended, and country by country reporting introduced, the administrative burden on SMEs will be hugely increased, for no real benefit.

This is rolling back the Single Market, and not in a good way. For corporates, its not a worry. For SMEs it is a major headache. How do you work out the VAT rate for each country in which you sell, when the regimes are all different, the rates vary and its all in a language you don’t speak?

As a humble member of the quotable but apparently nameless commentariat I have to agree with both you and Soarergtl (and probably the vast majority of people) that of course it is “no defence for X, facing an allegation that it doesn’t pay the appropriate amount of corporation tax, to say: ‘well, I’ve done some other things that the law requires of me.’”

As you have pointed out clearly X is not Facebook, since no one has alledged that Facebook is not meeting legal obligations here, and no one is arguing that breaking the law in one area is ok if you are compliant in another (certainly I don’t think this is what Chas Roy-Chowdhury was arguing in his remarks?). So I am not sure what relevance the imaginary case of X brings to the altogether different case of Facebook. It is a diversion.

However the points about the broader tax footprint of FB’s operations may be relevant to other questions which go beyond questions of legality.

One of the frustrating things with the tax debates is that they tend to slip, sometimes mid-sentence between questions of whether the problem being discussed is one of legality or morality or the economic case for taxing companies differently. All of them are fair enough questions, but they are not the same.

As no one seems to be arguing that FB is avoiding taxes which it legally should be paying I think we can put that one to bed without seeking further ‘defense’.

The general argument seems to be that FB has misbehaved by breaking a moral code. But so far we have far failed to crystalise these moral concerns into a practical set of principles and testable expectations. So, as Iain notes it is hard here to get beyond the broad perception that big-companies-with-small-tax-bills must always be up to no good

Thirdly there is the economic question of who would be better or worse off if FB were taxed differently, either through changes to the law or through moral suasion to change its behaviour. Here the questions of the overall tax impacts of Facebook’s operations do seem relevant.

Personally I think there there is a case for trying to establish clearer principles for good corporate behaviour in tax that go beyond legal requirements – but to do that, as Iain and Paddy say we need to get beyond the attack-and-defense dynamics towards discussion of facts and principles.

Sorry for delayed response. It’s been pretty hectic.

I think, with respect, you’re may be misreading what I said. I said avoided – i.e. legally – not evaded (i.e. illegally). People are cross about legal avoidance – and the rules that permit it. I think they’re right to be cross. And to say, ‘why focus on corporation tax – businesses pay other taxes too’ does not and should not deflect that crossness (apologies: ugly word). Relevantly to Facebook, it does business with UK advertisers and generates revenue here. As I understand the way in which its business model operates those revenues will never be subject to UK corporation tax. I don’t think that’s right.

As to your ‘more fundamental point’, Facebook does all of those things not out of the goodness of its heart but because doing them will enable it to generate more profits. So I don’t think those things, either, excuse Facebook’s business model – or a tax regime which enables it – which is perceived (we assume) to generate profits in the UK without those profits being liable to corporation tax.

I wasn’t really arguing that. My main point was (as @stephen_wigmore identified) about the nature of Facebook’s business which may not be what everyone expects. But, yes, I suppose a corollary of that argument is that UK Facebook has its transfer pricing wrong. I’m not especially interested in speculating about what steps HMRC may or may not be taking in relation to UK Facebook. I don’t think it’s a particularly productive avenue of enquiry in circumstances where neither of us has any visibility.

If I named the people I was being rude about I’d be criticised for doing that. I took the view it was politer to allow people to self-identify if they wanted to. You have.

As to the defence point, I think you need to read the answer I gave to Soarergtl. I certainly don’t accept it’s a diversion – but I used X because I wasn’t then seeking to make a point about Facebook. If you read my original post (“the appropriate amount”) and your original comment (“has anyone suggested legal misbehaviour”) I hope you’ll be able to agree that you rather assumed I was making a legal point. And that your assumption might not have been justified.

That having been said, I do agree the ‘moral’ debate – which is what I was focusing on – is not sharp enough. As I see it, there is avoidance which clearly has a moral element, avoidance which clearly doesn’t, and a large ‘difficult’ category. The fact that we have a ‘difficult’ category doesn’t mean we don’t have a category of case in which there is a moral element. Beyond that, I’m not quite sure whether you’re saying anything you want me to respond to.

Thanks for the considered response. I think we simply disagree on the fundamental.

I accept that Facebook at al set-up in the UK to further their business aims, generally to make profits. As I work for businesses which also want (and need) to make a profit, someday, I see nothing wrong in this. I expect you do not either.

Where we might part company is that I believe the UK needs these companies to want to set-up here, to provide goods, services and, crucially, employment.

The UK is, in effect, competing with other countries (especially the rest of the EU) to attract these companies and the jobs they bring. We even (though I am not necessarily in support of it) subsidise them to set-up in areas of high unemployment (Amazon, for example).

Causing reputational damage to companies which have, apparently, broken no laws and observed all regulations by vague allegations of wrongdoing (though I don’t believe you have done this, but others have attempted to do it) seems an odd way to attract them to the UK, rather than, for example, Ireland, Spain or Switzerland.

It is to them a marginal, but real, cost which we do not need to apply unless actual wrongs (rather than some people’s ideas of ‘moral’ failings which may not be widely shared) are discovered.

Worst of all are those who want to apply unnecessary regulations because ‘big corp=bad’ which generally fall much more heavily on local SMEs than on the supposed target. The recent VAT changes would be one example of this.

This is what I mean by being ‘anti-business’.

Reputation management is always a cost of doing business (personally I think the issues go wider than reputation management but for present purposes…). Everyone’s entitled to object to behaviour they find wanting. Businesses can choose to suffer the reputational consequences or change their behaviour.

I don’t see any existential question raised for UK plc by any of these propositions.

Not existential certainly, but marginal. A marginal increase in the number of jobs in the economy is all that is needed.

I agree – we disagree.

I think one key aspect is the extent that tax is zero sum: who else must pay?

For a given level of spend (or a given level of deficit) then there is an expected level of tax income. And if by creative techniques people avoid paying that, then either spend must be cut – or other taxes must go up to balance.

So if Facebook or Amazon or Starbucks pay less, we must pay more. And it is legitimate to discuss that.

Now clearly, this happens: over the years the balance of tax from different streams has changed. Corporation tax has gone done, VAT has gone up and so on.

And that is partly @soarergti’s point.

We may (as a country) decide corporation tax is a ‘bad’ tax or it is inefficient and, as a policy, to reduce that rate.

But until we do that, it is not unreasonable to expect everyone to pay by the same rules.

That has a moral dimension – but it also has a significant policy implication.

Are we happy that Starbucks has a significant cost advantage over another coffee chain, not because it is more efficient or better, but because of how clever its tax lawyers are?

Amazon for a long time avoided VAT. It now avoids much corporation tax. That gives it huge advantages over retailers who do not do those things.

Is that fair?

Perhaps we are happy with that, and accept the consequences.

Perhaps we could say that no-one, including local bookshops, need pay these taxes.

Or perhaps we feel that companies should, indeed pay their “fair share” and should not gain business advantage in this way.

Those are political choices.

But it is naive to think that multi-billion pound tax bills do not have economic implications if they are paid or not, and it is naive to ignore the political consequences.

Elegantly put. Better than I would have, even if I had realised I needed to get out of the trenches.

I can definitely support dividing avoidance into smaller categories. It chimes with my example of gifting profits to a charity – Oxfam probably good, private and small possibly less so. I also think there’s possibly a category of too difficult to think about (say a national charity that operates High Street stores that sell new goods and undercuts local firms because, amongst other things, the law exempts them from paying rates, and staff volunteer, and then donate their trading profits to the charity).

But I think for MNCs it’s not always about competitve tax advantage. It’s said that Starbucks makes an operating loss because it took on too many expensive properties. So, if there are no profits then tax is not relevant? If FB paid more tax (and so maybe charged advertisers more) do we really think there are viable lower cost competitors who would be able to take advantage? Google?

If we see tax purely in terms of cost then that is the kind of argument we can fall into. Do we tell Tescos or Sainsburys that they must not use their purchasing power to offer lower prices than a local convenience store? I think the moral fair share argument only succeeds if we talk in terms of an old favourite, social responsibility. It might be that the tax laws almost conspire to generate avoidance (PE exemptions for Amazon) so we change the laws. But surely we also create frameworks that bind such firms into other areas, such as training, supporting micro-businesses and start-ups.

Do others find that might a more productive type of discussion than how to calculate the ETR of a UK/US company?