Late February. How’s your New Year’s Resolution going? Not so well? Congratulations, you possess a necessary (but happily for George, not sufficient) qualification to be the next Chancellor of the Exchequer.

In its first Budget, 22 June 2010, this is what the Coalition said:

But am I making some party political point? I am not. This is what Labour said in its Pre-Budget report 2002:

And these are but the last two in a long line of failed resolutions: changes were considered in 1994, 1988 and…

There have been some reforms: Labour introduced a levy for non-doms: a £30,000 annual membership fee to belong to the best tax mitigation club there is. And the Tories have changed the fee structure to reflect the (perfectly sensible) notion that the less deserving you are of club membership, the more you should have to pay to continue to belong. Come April, if you’ve been resident in the UK for 17 of the last 20 years, it will cost you £90,000.

But proper reform? It’s the fiscal equivalent of getting a little more exercise. You know it’s a good thing but it’s just… so… well… Gosh, is that the time? There’s an election coming!

***

What most proper (by which I mean non-tax haven) countries say is: if you live here we’ll charge you to tax on all your income and gains around the world. In the UK, we’ve carved out an exception to that rule: if you are not ‘domiciled’ here we’ll charge you tax only on the income or gains you bring in (or ‘remit’ – hence the remittance basis) to the UK. Your assets and income outside the UK won’t be charged to tax here – and, if you arrange your affairs carefully, might not be charged to tax anywhere. And your country of “domicile”? That’s your ‘home’ country.

I could write tens of thousands of words delineating the operation of these two key concepts: ‘domicile’ and ‘remittance’ basis. But to focus on how they work rather than what they accomplish is to miss the point. And the point is that the remittance basis is a fiscal sweetener – a bribe, if you like – payable to the wealthy with foreign connections to cause them to move to or remain in the United Kingdom.

It’s only having called it by name that we can turn to look at whether we should be paying it and, if we should, what it should look like.

Proponents of the non-dom rule say that it encourages wealthy foreigners to move to (they don’t say but do mean) London and spend their money in (also) London – and that brings benefits including additional tax receipts to the economy. They’re right.

Detractors say, looked at globally, the rule signals our enthusiastic participation in a race to the fiscal bottom which makes winners of the fantastically wealthy and losers of everyone else. They’re also right. Some detractors – a good recent example being the BBC’s recent The Super Rich and Us – also point to the fact that the arrival of wealthy foreigners hasn’t spelled the end for inequality in the UK. Someone, somewhere, possibly in Norfolk, will be flexing his blackboard ruler, but that seems to me a little like arguing that, because I’ve turned on my two-bar electric heater and I’m still cold, it follows that heaters don’t make you warmer.

But just stand back and accept the logic of the (good) points for a second. There are all sorts of ways in which we might entice wealthy foreigners to come and live here. Stable government, a civil service free of corruption, our cultural richness, excellent public infrastructure (someone stop me, please, before I get completely carried away). Do we need a fiscal inducement too? And if we do need a fiscal inducement is this the one?

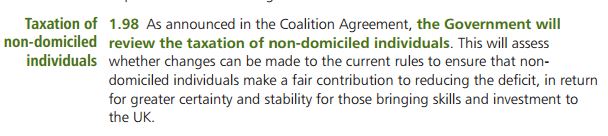

To answer that question we’d need to model how many would leave, how many would fail to come, and what the loss would be to the economy. Many will tell you they can, or have, performed this exercise. For myself, I like to recall what the Institute of Fiscal Studies, which so often (and often accurately) tilts at fiscal forecasting had to say, back in 2007, about the effects of rival political proposals for a non-dom levy:

![]()

This is the link for that pleasing flash of intellectual clarity.

But let’s press on, whilst recognising that to do so we’ll need to assume that sensible modelling is possible. Let’s also assume (controversially, but for the sake of argument) that we’d like to continue paying a sweetener.

The question then is, what should that sweetener look like? To answer that, you need to go back to my two key concepts: remittance and domicile.

The concept of domicile has many problems. The question whether X is domiciled in the UK often fails to admit of a clear answer: it is to borrow an attractive phrase (from Ian Jack) “a peculiar mixture of fact and intent”. Perhaps in consequence, legal challenges to domicile status are relatively rare (such that questions might sensibly be asked about whether all of those claiming the status actually have it). But most importantly of all, the line in the sand that the legal test draws is a pretty crappy way of separating out those we might want to give a sweetener to and those we might not. You might think that, after someone has put down roots, they might no longer need (or deserve) an incentive to come or remain here? But the domicile rule all but ignores that critical fact.

As to the remittance basis of taxation, it’s enormously complex to apply. That’s a thing modestly undesirable (to all but tax advisers). But its real failing is that it disincentivises the very thing we want to incentivise. The reason we give a sweetener to get wealthy foreigners to come here is not because we like their company (although often we do). The reason is that we want them to bring their money here and spend it here. Taxing them on the income and gains that they bring into the country discourages them from doing the very thing that the sweetener is designed to encourage them to do.

I don’t want to suggest policy on the hoof (he said, with the inevitable air of a man about to do so anyway). But it doesn’t take much imagination to think of mechanisms that might consistently promote the policy objective of offering a sweetener. If we are to have a tax mitigation club, what about a different one, with equally high annual subs, but that gave you a reduced rate of income tax or capital gains tax for the first, say, five or ten years of residence here? Not desperately politically palatable perhaps, but no less so than the present system properly understood, and likely to deliver far better economic results.

More modest reform might look like a domicile equivalent of the statutory residence test in the Finance Act 2013 – to create bright line tests between resident and non-resident status – coupled with a deemed domicile provision (akin to that in the Inheritance Tax Act 1984) by which you would be deemed to be a UK domiciliary after a number of years residing here.

But I’d love to hear your suggestions – and responses to the above – too.

Personally I struggle to believe that the super wealthy “non-doms” choose to live in London instead of Monaco because of the tax perks. It’s not the weather that keeps them here so it must be all the other great things London and the UK have to offer.

Therefore they don’t need a bribe to live here, so my policy on the hoof suggestion is scrap non-dom tax status altogether and tax all residents the same, like most civilised countries do.

If you want to phase it in to see if it is going to result in mass exodus then start off by saying that non-dom tax status is limited to 3 – 5 years.

It’s not rocket science…

Doesn’t even take much political balls, I would think it’s a sure fire vote winner!

In recent years I can think of a couple of non dom clients who appear to have acquired UK as domicile, show no signs of returning to their land of birth where taxes are higher and in reality would stay here anyway. Perhaps the Domicile relief is really passé.

I think an evidence base is needed for policy

Which other countries have a domicile rule that have an economy equivalent to the UK’s?

And if they don’t have such a rule, why not?

And what’s the alternative? Why not 4 years on remittance when first arriving and then full residency parri passu with all others living in the country?

Why not?

Because, the question not asked, is what benefit do the wealthy as opposed to those bringing their ability to work here on a temporary basis provide to the UK?

That’s the pragmatic view from Norfolk

I have always thought that there are a number of non-doms who have really acquired a domicile of choice in the UK. If an individual has a home/family/etc. in the UK would they not be regarded as settled in the UK for the time being and, therefore, having acquired a domicile of choice in the UK? RDR1 appears to imply at paras 5.16 & 5.17 that HMRC consider this to be the case but they seem reluctant to challenge. Should an adviser not consider the acquisition of a domicile of choice a little more carefully as well?

Why on earth would one want to offer any kind of sweetener? Where do the sweeteners stop? Your point here

“You might think that, after someone has put down roots, they might no longer need (or deserve) an incentive to come or remain here? But the domicile rule all but ignores that critical fact.”

And there is some evidence on the size of this problem.

http://www.taxjustice.net/2014/09/09/britains-super-wealthy-non-doms-bring-huge-tax-revenues/

All this is classic ‘competitiveness’ claptrap (by this, I mean you are right). Has anyone really weighed the costs versus benefits? And where does this nonsense stop? Martin Wolf put it well:

“Non-doms, we are told, make a gigantic contribution to the economy. If they are taxed too heavily, they will depart and the economy will suffer. Again, why not pursue this argument a little further? Should the UK not subsidise the inflow of human capital, just as many countries subsidise inflow of foreign direct investment? What about a negative tax (a subsidy) on all UK income earned by non-doms above, say, £100,000 a year?

Yet this, too, ought to be extended to highly paid citizens who, presumably, also provide big benefits to the economy. Why should the country wish to subsidise people to employ foreigners instead of citizens. So why not give everybody who earns about £100,000 a year a negative tax rate or at least a nice juicy lump sum? Moreover, if having non-dom billionaires resident in London is good, why not subsidise them too?”

The whole non-dom thing should be scrapped. Bad for Britain, and bad for the world.

“Which other countries have a domicile rule that have an economy equivalent to the UK’s?”

Well, there’s a project for a tax researcher…..

But isn’t that the wrong question in this context? Shouldn’t the question be which other countries that do NOT have a domicile rule have as many wealthy foreigners living there? And if they don’t have as many as us, why don’t they?

The thing about the super wealthy is they really are not going to stay here if we seek to tax them on world-wide income if there is somewhere else for them to go which won’t. So they go live in Monaco or Switzerland and if they really miss London they can fly in and out on their private jet for the weekend.

There IS evidence that the £30k/£50k levy is having the effect of reducing the number of non-doms in the UK (it’s mixed, but you can google for it).

If £30k makes some run, I can’t see many staying if we try to extract £100m+ a year (or whatever it might be) from them.

And bearing in mind that if you have International Conglomorate Inc in Switzerland earning billions for you, you don’t HAVE to pay yourself dividends to put in your Swiss account, you can let in roll up in the company while you stay here and only remit what you need (which is what you are doing at the moment) or get the company to lend yourself some to get by in the meantime. So you change the rules , announce that £XXXm will be collected, pre-spend that money (as Governments tend to do) and then find you only bring in £Xm.

Now this isn’t to say that I agree with the current system but it seems to me that a constant theme running through the tax reform debate is (i) the rich are ‘getting away with it’ (ii) they are exploiting ‘loopholes’ and (iii) all you have to do is close those loopholes with the quick stroke of a pen and extra tax will come flooding into the UK exchequer so fast we won’t be able to spend it all, justice will prevail and we’ll all live happily after. I happen not to agree with any of those three points, especially not the last one.

So, do I have an answer? If we’re talking about the super wealthy, I would favour an extension of the ‘investor visa’ scheme. If you’re hugely wealthy and want to come here, invest in UK business (properly, not just buying a £1m worth of FTSE 100 shares) or buy government bonds.

I often hear those who argue for higher taxes and clampdowns on this that and the other that it WON’T chase people out of the UK. That’s maybe true but it certainly won’t make the UK a destination of choice.

Perhaps it might be worth considering why we have the tax regime for non-domiciled individuals in the first place? It wasn’t invented as a “sweetener” to encourage rich people to come and live here.

There seems no reason at all for domicile to be the connecting factor for tax. Outcome often counter-intuitive one suspects; hence it’s a historic freebie and a fairly random one. Time to go surely?

The remittance basis makes no sense at all, with a tax incentive to somehow structure your offshore bank accounts properly to avoid spending money in the UK. It combines complexity with a dumb fiscal outcome ie just about the opposite of what the tax system should be. I would scrap the remittNce basis but alongside it introduce some sort of mega punishment tax if formerly remittance basis income is sunk into residential property as I suspect that would be the damaging destination of much of it.

From my tiny City experience, I know several Freanch people who have become multi-millionaires using the non-dom rule, carefully taking weekends abroad so as to deduct days (what good to the London economy?), then, having amassed this money, back off to France to put their feet up.

It makes no sense.

There is very little I would take issue with in your summary of the domicile rules which as you say, in effect turn the UK into one of the most favourable tax havens in the world, only for those who had the good fortune not to be born here ! I am no expert but I know of very few jurisdictions that actively discriminate unfavourably from a tax perspective against its permanent population. Yes non doms bring other tax revenues with their generous spending but in bringing in vast swathes of wealth, we create other distortions, most obviously in high end property markets which has knock on effects which we really have not got to grips with in the UK. I digress but I would wager that not all of the effects of non doms are beneficial if we take into account the broader needs of our “permanent” population. To address this, in classic British style we have introduced further complexity and distortion via stamp duty reform rather than addressing root causes, “tinkering at the margin” dare I say it. The problem as I see it arises from creating a complex many tiered structure which is at odds with an equitable system of taxation. I would hope we could agree that a tax structure that allows for upward social mobility and economic growth is a good thing and something that we should aspire to as a nation.

The solution lies as you and others have pointed out is with more of an American approach – live here and pay our taxes, the concept of the fully paid up citizen. The issue with the non dom rule is that we are as much a part of the problem of global tax avoidance. As I have said elsewhere and others have intimated, tax havens are pretty dreary places to permanently reside This will probably provoke howls of derision from the two or three people who disagree but so be it, the proof lies in the vast number of ultra rich who choose to avail of the many benefits of residing in the UK. But not pay as little as they possibly can. As intimated above, many of these people come from jurisdictions where the rule of law is very flaky and this is of huge value to the ultra rich.

We have chosen (globally) to be competitive on the corporate taxation front and i think we need to do the same on with income taxes but on an equitable structure for all residents. Simplification again is of huge value here too when we consider our tiered tax rates which are utterly meaningless to the ultra rich as in effect, their income tax rate would be 45% and I think we could all agree they would not pay it. I could digress and highlight that widespread avoidance by the resident wealthy is prima facie evidence of the fact that our top rate of tax is too high but that no doubt would enflame other passions…. Therefore in my view we need to migrate towards a flatter, fairer level of tax paid by all, regardless of country of birth. This will take courage and the ability to move on from the political tinkering mindset of the various flavours of government we have had over the years which has only served to create greater inequity and complexity.

Of course this is not something that will be achieved in a pen stroke but it is vital in an era of global competition, where wealth increasingly attaches itself to mobile intellectual property (leaving anachronistic tax structures behind – another subject in itself) that the direction of travel is the right one.

There is very little which is “bright line” about the SRT – a disgraceful and inelegant attempt at what passes for legislation these days. On an unrelated note, will you be updating your earlier blog entry on film partnerships soon? Much has been said on avoidance etc on this blog since then and i am wondering if you have anything further to add in light of recent developments?

Not sure I’d agree on srt – certainty it’s a big improvement in the status quo ante. But what do you think it would be interesting to hear about on film relief?

As an aside, I think it’s fair to say our non-dom tax rules are a happy ( or not, depending on your viewpoint) accidental historical legacy. Be that as it may, they do indeed now represent a simple bribe. A bribe obviously has no connection with fairness, so we should only consider whether or not it actually works.

So well done Jolyon for pointing out the counter purposive effect of the remittance rules. (We can of course ‘alienate’ our income and gains first by placing it in an account with HSBC in Geneva in the name of a Guernsey trust, but that was last week’s fun).

So the question would seem to be “How should we bribe people to come here?”

At which point my sense of whimsy can be let out to play. For we have an excellent methodology very apparent to us in Switzerland. Yes indeed, a borderline-notional rent-based tax that allows you to bring all non Swiss earnings into the country without tax. And its success can be measured on the number of outraged posts the HSBC Geneva story has generated. And it’s open to all non-Swiss with enough dough; no need to mess around with a concept like domicile. The UK, having already introduced a charge, a ‘finders fee’ if you like, can happily move to a more honest Swiss system of open bribery.

Again, do not bother me with notions of fairness.

Perhaps I should add that, with most of us taking our father’s domicile and a large influx of immigrants into the UK in recent years, a much higher proportion of British born UK citizens will theoretically now be able to claim non-dom status. This is an issue that may have no choice but to address soon.

Apologies for the tardy response. I guess what I am asking is this: My summary, based on this blog, would be that you have relatively strong views on avoidance. As you say yourself:

“Advising a client as to his prospects of succeeding in litigation, I would be heavily influenced by my assessment of whether his use of a particular relief was pro- or anti-purposive. That technical assessment of prospects would map closely to my view of the morality of a transaction that accesses a relief provided for by Parliament.”

I am also thinking about your blog re Weak Transmission and some follow up comments you made in the Hardman lecture. With all of these in mind (films, comments re morality, the stance in WT and the H lecture) may I ask therefore to what extent does your personal opinion (assuming I have accurately summarised it – apologies if not) influence your decision to represent certain taxpayers in litigation (and of course I am not asking you to be specific re certain cases)? For instance if your view of the morality of the transaction were negative what would happen?

Hi Shay,

Not sure it’s sufficiently interesting to blog about (although that doesn’t always stop me). But very happy to answer your question. There are a couple of facets to the answer:

(1) The Bar has a cab rank rule – so formally speaking I am obliged to accept any instructions that come in. The rule isn’t much observed in practice but it has a powerful foundation: the right of everyone to have an advocate for their cause.

(2) Before I litigate I am usually (although not invariably) asked for a view on prospects. As you’ve observed, my view on prospects is (usually) influenced by how I think a judge will feel about the prospects. That might make me more pessimistic than others – which can cause clients to go elsewhere – but against that I am very experienced in litigating these cases and so people generally trust my judgement and tend to want my services.

Not sure if that answers your question – if not, do put some follow ups…

Jolyon

Pingback: Waiting for Godot | Why are HMRC not challenging non-dom status?

Have looked at that question here https://waitingfortax.com/2015/02/23/why-are-hmrc-not-challenging-non-dom-status/ …

Pingback: Waiting for Godot | Is the sky falling in?

Hi. The conversation has moved on but just for my own edification I’ve had a look at the BSB handbook and in particular rc21. Surely enough scope within rc21.2 to decline to act in the sort of scenario were discussing unless I’ve misunderstood it? What I’m confused about is that you’re actively making a best case in Court re certain planning (you got a nice mention in the recent judgment) on one hand yet writing on here opposing such things on the other. I am not saying it is wrong. I just am surprised by these seemingly contradictory actions.

Hi Shay,

I don’t think rc21.2 quite covers the point. That deals with conflicts of interest – to take an example, where I am being asked to sue a company that I own – rather than the situation you have in mind (where I might have personal views about what my client has done).

But leave aside formalities for a second (and I do think that’s the right way to think about it – see the “formally speaking” in my original answer).

Obviously I wear two hats: one as someone with personal views on tax policy and practice and one as a member of the Bar. Personally I’m very happy wearing those two hats. I appreciate that I will likely rule myself out of doing particular pieces of work as a barrister by expressing the views that I do as a commentator. But that’s a risk I take and a result I’m happy to live with.

As a commentator on policy and practice I obviously have and express views on avoidance transactions: I don’t think I am as far along the spectrum as your original question implied. I’m probably slightly more anti-avoidance than many of my professional colleagues but I’m far more pro- sensible tax planning than most of those who are campaigners. Fundamentally, like many of my colleagues, I’m driven by what I see as the importance for society of a fair and properly functioning tax system.

As a member of the Bar, I guess I’d make three points. The first is that that a large proportion of the transactions badged ‘aggressive tax avoidance’ are not clearly so. There’s usually an intellectually respectable way of conceptualising a transaction as ‘good’ avoidance and (recognising that there’s a spectrum) sometimes it can be difficult to work out what the ‘right’ analysis actually is. Certainly it’s not always something you have a view on immediately you pick up a set of papers.

The second is there’s a very important principle that everyone is entitled to proper representation. If members of the Bar allow moral judgements to guide who they’re prepared to represent that principle collapses. Perhaps there’s a distinction to be drawn here between pre-transaction planning – which I’ve never sought out – and post transaction litigation (which I have).

The third is about the role that I play as a barrister. Let me pose, rhetorically, the difficult question: if I was professionally free to say ‘no’ and I was asked to act in a piece of litigation involving an especially ‘bad’ transaction, would I act? I would. As a barrister, I recognise that it’s for judges and not for me for to say what the law means.

So I think I can consistently (a) argue (as a barrister) that the present state of the law is that my client should succeed and (b) argue (as a commentator) argue that the law should be changes so that that client shouldn’t.

Hope that’s helpful,

Jolyon

Quite a few jurisdictions do it – they just call it something other than a ‘non-dom’ rule. For example Belgium has special income tax rates for ex-pats if they can show they are ‘controlling’ activities outside of Belgium. Belgium also has incredibly low/non-existent taxes on dividend income, so most wealthy people wouldn’t be paying much anyway.