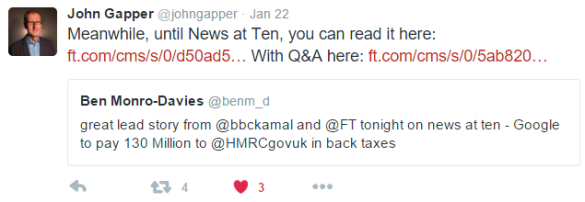

First out of the blocks on Friday the 22nd was John Gapper of the Financial Times:

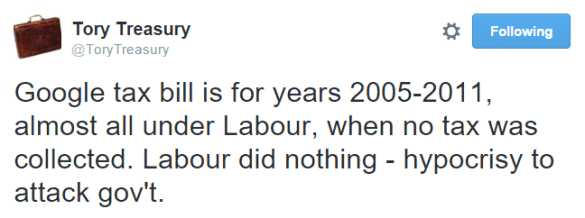

At 10am on Saturday 23rd, this is what the “Official CCHQ voice for all things Treasury” said:

And here’s what the Financial Secretary to the Treasury, David Gauke, said later that day at 1.47pm:

Labour quite properly wanted to understand whether these allegations were true.

And there were also wider public concerns around whether the deal struck with Google represented a good one for the UK taxpayer. John McDonnell, Shadow Chancellor, was given permission to ask an urgent question in the Commons:

But David Gauke said he could not give further details because of the duty of taxpayer confidentiality.

But what is the £130m actually from? And to what does it relate?

It has been widely quoted that it is from tax, interest and penalties. The source of that belief appears to lie in an interview HMRC’s head of business tax, Jim Harra, gave to the BBC’s the World at One.

Following a tax investigation, a taxpayer will pay any additional tax that has been found to be due, plus the interest consequential on paying that tax late.

The penalties are particularly important.

There can be modest fixed sum administrative penalties for technical slips. But penalties can also signal that a taxpayer has behaved ‘badly’ – negligently or fraudulently. They can send a message that a taxpayer has been held to account.

So does Google have a liability to penalties? Not according to its accounts. Only tax and interest:

I think it likely that Jim Harra was responding to a specific question with a general answer – that would be my expectation given the deep (perhaps too deep) privileging of taxpayer confidentiality in HMRC – and the press failed to grasp the context of his answer.

So, Google was not penalised.

But what is the composition of that £130m figure?

First, £69m for periods prior to 30 June 2015.

Second, an existing provision of £33m:

That provision first appeared in Google UK Limited’s accounts to 31.12.12 as £24m:

and grew over the year to 31.12.13 to £33m.

Third, interest of £14m:

And fourth £14m of extra tax liability for the current year:

Making £130m.

And to what periods does it relate?

Here’s what Google UK Limited’s accounts for the period ended 30 June 2015 report:

You’ll note those words “for prior accounting periods and the current accounting period”. On 30 June 2015, Labour had been out of office for fully five years.

So the highly political allegations tweeted above appear to be untrue.

The £130m liability does not cover the period 2005-20111. Instead it covers a period dating back to 2005 and ending on 30 June 2015. It’s 2005-2015. Including over five years of Conservative Government.

Jolyon, I think there are several different issues here.

Google has settled a long(ish)-running tax enquiry and the quantum of that settlement, including penalties, is £130m. As you have shown, that covers the periods from 2005 to 30 June 2015. Of course, the £69m for prior years is not analysed so we don’t know whether it is spread across those years or whether, for example, it just relates to one or two years.

For many, there is then the question as to whether £130m is the “right” number.

The issue that I believe your post really highlights, however, is that Politicians really should try to avoid scoring political points on matters about which they do not have sufficient knowledge. Labour said that the Government had been soft on Google in the past (I’m paraphrasing) and the Tories claimed that the “problem period” was mainly Labour’s responsibility. Well, frankly both arguments are stupid in their own way.

Maybe Labour could (should?) have done more to toughen the regime for multinational companies. Maybe the Tories should have done more since 2010.

The point that seems to be getting missed in all of this, however, is that it is HMRC that is tasked with enforcing the tax legislation – including establishing whether or not Google has a PE in the UK – not politicians. As we know (and is increasingly being questioned) HMRC is a non-ministerial department. It is not up to politicians, therefore, to enforce the collection of taxes. Their role – which both parties have failed at – is to ensure the legislation is robust.

Actually, the politicians have another important role as well. To ensure that HMRC is properly funded and resourced in order that it can do its job effectively.

In theory your point could be right, unlikely though that would be. In practice we know it’s not right because of the £13.8m adjustment for this period.

If by “your point” you mean my comment on the £69m, I was making the point that its precise allocation is unknown. My suggestion that it could, in theory, relate to only one or two years was meant as an example, however unlikely.

The fact that there is an amount of £13.8m relating to the current period would not appear to have anything to do with the “prior periods” per se.

The adjustment for PE 6/15 is in consequence of the “tax audit settlement”. Are you suggesting it has nothing to do with the £69m additional provision?

Jolyon, I fear we are talking at cross purposes here. My original comment, which was in respect of the “settlement in respect of prior periods” – i.e. the £69m. I said that

“Of course, the £69m for prior years is not analysed so we don’t know whether it is spread across those years or whether, for example, it just relates to one or two years.”

What I was saying was that the £69m covered (apparently) the periods from 2005 to 2013. Almost as an aside I commented that what we didn’t know was how that £69m was allocated between those years. My example of it applying to just one or two years was an extreme example to highlight my point.

In your response, you referred to “your point”, I took this to be a reference to this point above. Was I wrong?

The fact that an element of this overall settlement relates to the current period – and I am not in any way disputing that it arises as a result of the enquiry and the settlement – does not (I believe) change my point about the allocation between the earlier years of the £69m.

Pingback: Google’s £130m: what is it and when is it from? | VeryVexed

Without investigating much, I suspect that the £130m relates more to later periods than earlier periods, and there are at least two reasons that could be right. I believe the revenues and profits of Google have grown dramatically in the period from 2005 to 2015, and I suspect the number of Google employees in the UK has also increased substantially (as well as its other costs, such as premises). If there is a profit-related element to the settlement (a commission, say) then there will be more in later than earlier periods. Similarly, if there is a cost-related related (an uplift to cost-plus pricing, say) then there will be more in later than earlier periods. (However, as interest increases with time, it is likely to be weighted more to earlier periods.)

I am sure Jim Harra is correct on the tax *rate*. I doubt HMRC has agreed a 3% tax rate, or anything explicitly below the headline rate of corporation tax in each period. The question is not the tax *rate*, it is the tax *base*.

It seems, at least so far, that HMRC do not think there is anything worthwhile pursuing through litigation. Are you able to express an opinion on whether that is because of poorly drafted legislation or pusillanimous tax collecting?

Not really. Sorry.

Gauke’s statement, although political as you say, appears consistent with this fact pattern. The Treasury tweet, not so much.

Sorry, backing up, the tax disclosure, note 8 in the 2012 accounts, is that there is a £24m provision for tax in relation to “share-based payments” (presumably deductions for cost relating to the shares and restricted stock units granted to UK employees, detailed elsewhere in the accounts, see note 17). That provision is not changed in note 8 of the 2013 accounts.

(The December 2012 and December 2013 accounts are freely available from Companies House beta, but then the period of account was extended from December 2014 to June 2015, and I can’t see the June 2015 accounts there. Are they available online somewhere else?)

So, is the recent settlement of £130m anything to do with transfer pricing and PE status at all, or just the deductibility of costs relating to employee shares?

Nice point. Am looking. The accounts to 30 June 2015 aren’t publicly available (although I have a copy).

Pretty clear that there were two separate incidences of underpayment of corporation tax. You can see this from the separate provisions at Note 8 of accounts for pe 31.12.13 – and how those provisions track through to the accounts for the pe 30.6.15.

Pingback: Once might be unfortunate. But twice? | Waiting for Godot

Good point – so there is a second provision for £1.1m on page 18 of the December 2013 accounts. Not clear to me why it is not listed on page 17 too. Also not at all clear what it relates to – possibly more than one issue.

Since I posted above earlier, the 2015 acocunts have appeared in the Companies House system – “02 Feb 2016 – Full accounts made up to 30 June 2015 – This document is being processed and will be available in 5 days. ”

I’m also not sure where your £33m figure comes from (“…grew over the year to 31.12.13 to £33m”). Is it in the 2015 accounts? Not interest, presuambly, as you disucss that separately.

Sorry, just trying to understand (a) what issues are dealt with in the accounts and (b) what the £130m settlement relates to.

The £33m figure comes from the 2015 accounts (see the “Second” above). I don’t quite get to that number if I do the maths – I come out to £26m or so…