In the last stop on my whistle stop tour of the tax gap, I address how much of the tax gap is made up of tax avoidance.

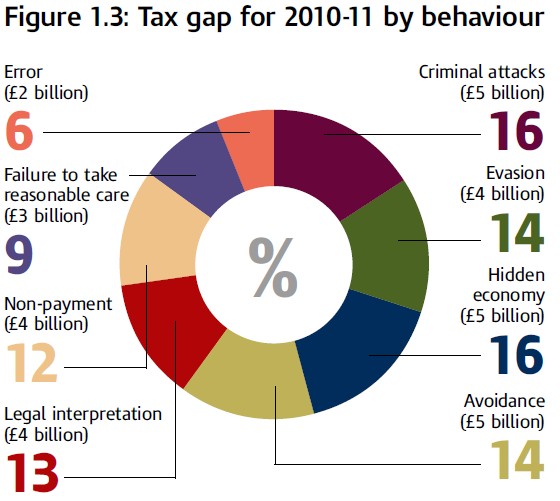

HMRC publish data in relation to how, their statistics indicate the gap arises. That data is summarised in the following table:

HMRC describes ‘avoidance’ (for the above purposes) as that which is ‘operating within the letter but not the spirit of the law’. As such, HMRC say, it does not extend to “legitimate tax planning” which “involves using tax reliefs for the purpose for which they were intended. For example, claiming tax relief on capital investment, saving in a tax-exempt ISA or saving for retirement by making contributions to a pension scheme”.

Two cautionary notes must be sounded in considering these figures. First, some commentators appear to eschew the notion of “legitimate tax planning”. Richard Murphy, for example, the controversial tax campaigner, appears to regard even pro-purposive tax planning as the mere exploitation of “loopholes”. Second, as I have previously noted, the tax gap only refers to tax which is within the letter or spirit of the existing legislation. It does not refer to tax which should be within the letter or spirit of existing legislation.

If pro-purposive tax planning is included, or the gap is defined as including that which should be taxed, then the size of the tax gap will increase and the proportion of that gap attributable to avoidance will increase substantially.

However, as things stand, the proportion of the tax gap attributable to avoidance, whilst large in absolute terms, is relatively small expressed as a percentage of the tax gap. Despite this, it almost entirely dominates the political debate.

I will turn next week to look at the Progress Tackle Tax Avoidance Charter. But, and this has been the point of my quick survey of the tax gap, an efficacious tax policy is one that goes everywhere the tax is uncollected, and does not merely follow the noise.

You must be logged in to post a comment.