In his paper ‘Risk-Mining the Public Exchequer’, David Quentin says

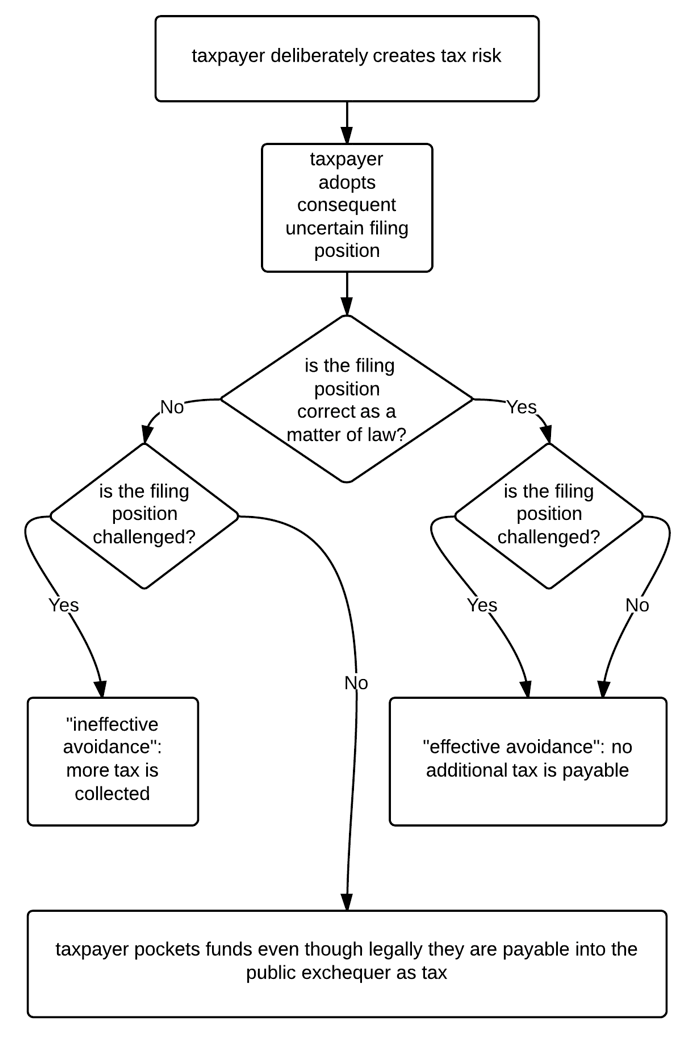

This risk game that tax avoiders play with what is potentially public money is set out in the flow-chart on the next page. The innovative feature of this apparently simple flow-chart is that I put the questions in the correct order. The mistake invariably made in this context is to treat the process of tax authority challenge as itself determinative of whether or not a liability to pay additional tax arises. This treatment reflects a fundamental error of analysis. Except in the very rare case of retrospective anti-avoidance legislation, the liability is anterior to the processes of enforcement.

David illustrates this in a flow-chart

While liability is indeed anterior to the processes of enforcement, I’m not sure that David’s flow-chart gets it quite right though in implying that liability is determined by HMRC’s view of the law. Liability to pay tax is determined by the law. So taxpayer risk is in principle a function only of the likelihood of the taxpayer being wrong in law. Taxpayer risk is in practice also a function of the likelihood of challenge by HMRC and of the challenge succeeding.

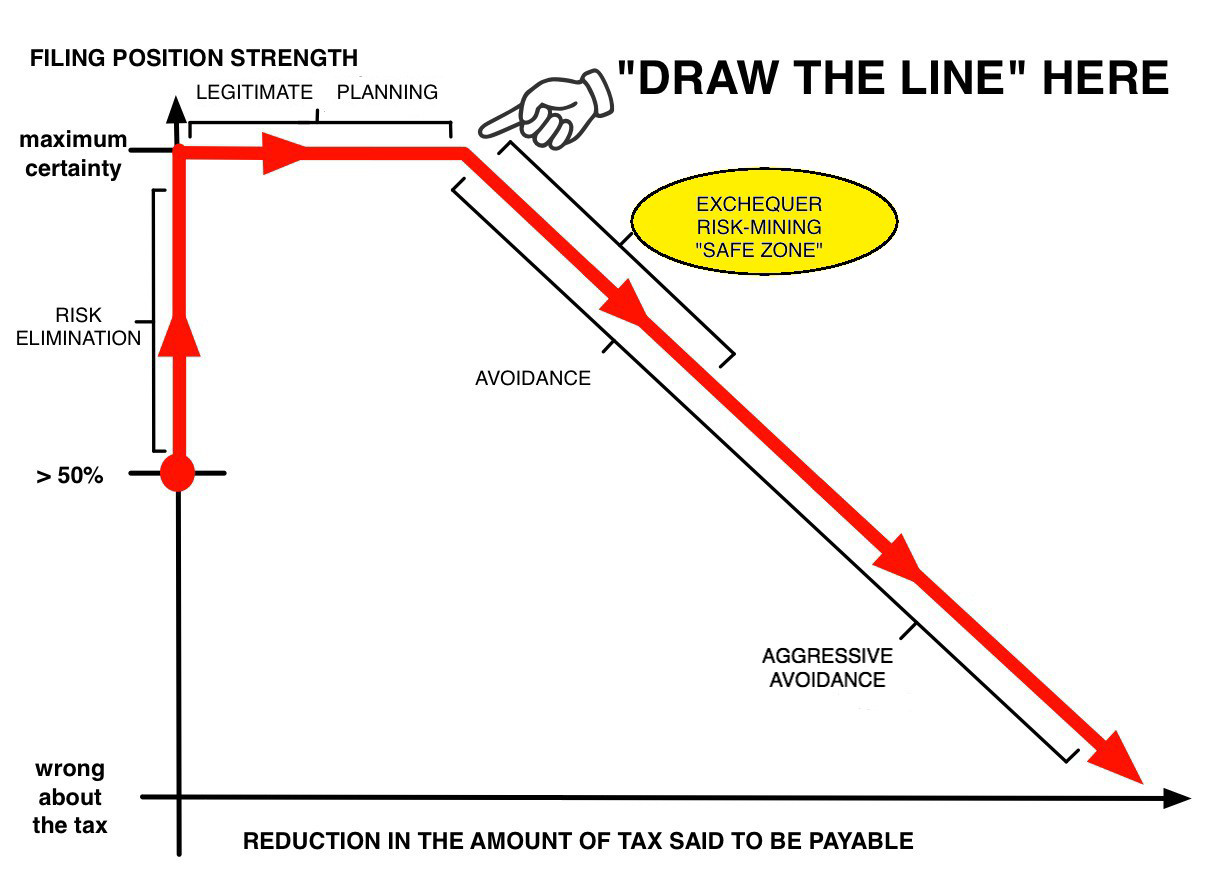

For David, maximum certainty means reducing each of these functions to nil, but the risk of HMRC challenge can only be reduced to nil by adopting HMRC’s view of the law entirely. In David’s picture below, that’s what travelling along the horizontal path with him is – looking at reliefs, allowances etc. and seeing if your actual circumstances meet criteria set out in HMRC guidance.

David is perhaps disingenuous in going on to say

It should be emphasised that we are talking here about tax risk that has been deliberately created qua tax risk, and not tax risk which has arisen as a result of deliberate but non-tax-motivated behaviour. If you do something in pursuit of your commercial objectives and it gives rise to tax risk, you are not in the “avoidance” zone. You are over on the left of the curve in the zone where you want tax advice to eliminate tax risk, not create it. If you have an uncertain filing position over in that zone and it is not challenged you cannot be reproached for any loss to the public exchequer. The difference is in the risk gradient at the end point that the tax advice is taking you to. There is no “blurred boundary” or difficulty in “drawing the line” between on the one hand eliminating and on the other hand introducing tax risk factors, and advice which fails to identify itself as doing one or the other would be very incompetent indeed. To distinguish deliberately-created tax risk, which is better thought of as risk for the public exchequer rather than for the taxpayer (for whom it is really an opportunity) I propose to label it “exchequer risk”.

Does David actually mean ‘abuse of law’ – like driving a lorry across a border and back for no purpose other than to get a tax refund? If so, it is a false distinction (or at least not a very meaningful one) to say that on the one hand there are these cases and on the other hand every other case where taking advice is only for the purpose of eliminating tax risk. But that seems to be implied by his saying that there are no blurred lines.

That there are blurred lines is shown by Rebecca’s examples which as she says illustrate that the law can produce wide variations in tax burden on essentially the same income of the same person depending on which part of ‘the law’ is thought appropriate to apply. Clearly Rebecca feels that risk of challenge arises not so much from any uncertainty about the law, but uncertainty about HMRC’s position – informed by her knowledge that if for no other reason where there is less tax burden there is likely to be more risk of challenge.

While Rebecca calls this bread and butter planning, she recognises that in some cases the public might see it as the gaining of an unfair advantage. Precisely because they are ‘planning’ of some sort her examples perhaps slightly obscure the principle. And notably, they cannot be on David’s horizontal line because they are not characterised by maximum certainty.

For example in relation to the appropriate use of a relief, even with the best will in the world and intent neither to minimise tax nor plan anything, it is not always entirely clear whether every taxpayer detail matches up precisely with every HMRC requirement. Indeed in many cases, HMRC having provided guidance, it is left to the taxpayer to decide upon an apportionment, or make some other decision about his or her own liability. The guidance (and indeed the law) is often couched in terms of what is fair and reasonable and this requires the taxpayer to make a subjective judgement in any case. And HMRC are clear that their guidance (with a very few exceptions) represents their view of the law and that only the courts can decide what the law actually provides. Taken together with Rebecca’s points this means that maximum certainty in terms of certainty about risk of challenge can only be assured by always taking an extreme position on any spectrum of choice.

I’m not one to harrumph on about ‘Westmoreland’ et al and it being the mark of honour of an upright citizen not to feel obliged to offer anything up to the Revenue, but it does not seem reasonable to characterise choosing anything less than maximum certainty as the deliberate choosing of risk such as to amount to attempted avoidance, when maximum certainty derives not from the law but from adopting HMRC’s view of it. Rather, the taxpayer risk accepted or declined by the taxpayer is 1. that the position they adopt might not be correct in law even though they believe it to be so and 2. that HMRC might challenge it successfully. Taking a position that is not believed to be correct in law in the hope that it will not be challenged is not avoidance, it is evasion.

If it is accepted that positions of less than maximum certainty can be adopted legitimately (in every sense) then the question is what those positions are. Even if HMRC were to provide certainty to Rebecca as to the position that they would adopt themselves in relation to each of her examples, HMRC are not always right about the law. While they might point to a high rate of success in litigation, that tells us nothing about the proportion of cases where they do not litigate because they feel their case is not actually likely to succeed. Though of course something about this can be inferred from the volume of legislation.

For this reason, it does not seem correct to characterise taking any position other than one of maximum certainty as the taxpayer creating risk. Rather, each point on the spectrum of choice has a particular risk of successful challenge. The taxpayer does not create the risk but in his or her choice of filing position either accepts the risks associated with that position or declines them. Jolyon’s badges of avoidance can be helpful in assessing this risk, although I feel that they are more weighted towards assessing the risk of challenge rather than the risk of successful challenge.

So from the taxpayer point of view I think the position appears to be more like this:

I think this is the correct way of presenting things because when David talks about Exchequer risk he can only mean the risk that an incorrect treatment in law will not be detected by HMRC. A correct treatment in law cannot pose an Exchequer risk properly defined – a risk that an amount of tax actually due is not paid – whether or not HMRC’s initial view is that the amount is due. This is implicitly accepted by HMRC in adjusting the tax gap estimates in light of decisions of the courts. That is, some of the tax gap is always at risk in that it is comprised of an incorrect estimation by HMRC of the tax due. To put it another way, there exists a tax risk for the Exchequer in that tax said to be payable by HMRC in law is not payable and if correct filings are made will not in fact be paid even if they are challenged by HMRC. It is not meaningful to describe a taxpayer making a filing that is correct in law as creating tax risk, let alone deliberately so. The only tax risk in these circumstances is the Exchequer risk created by HMRC’s incorrect view of the law. David labels as ‘effective avoidance’ in his flowchart those cases where a filing that does not adopt HMRC’s view is found to be correct in law by the courts. As a filing that is correct in law results in the payment of the correct amount of tax it rather begs the question of quite what has been avoided. I do think that bundling up such cases with ones that are not correct in law and labelling them all as attempted avoidance is not particularly helpful to the debate.

In conclusion, David’s assertion that “the deliberate creation of exchequer risk … is the essential defining characteristic of what has hitherto been labelled “tax avoidance”, distinguishing it from “legitimate tax planning” does not seem right. The concept of exchequer risk seems to rely too much on maximum certainty (or rather its absence) when this is in fact not a relevant criterion for establishing liability to tax. Neither enforcement nor certainty can be anterior to liability.

Follow Michael O’Connor on twitter @StrongerInNos

You must be logged in to post a comment.