Writing here, I explained how Employee Benefits Trust work and why they were used for tax planning.

But I also promised to try and explain why the decision of the Court of Session in the Rangers case seems to me to be wrong. And to look at what happens next.

But first, let me repeat my warning from Part 1:

If you’re a tax specialist you’ll also need to make allowances for the fact that this piece isn’t written for you. I make no apologies for not capturing in these posts the full technical detail around Employee Benefits Trusts.

***

As I said in Part 1, to have a liability to pay income tax you need to have something that is “income” – but you also need to “get” that thing. If you work hard for three years and your employer pays you a bonus in year three because of all of that work do you have a liability to pay income tax in year one? There is income from that year, after all?

I give you this example because what I think the Court of Session has got wrong, in summary, is to focus too much on the income and too little on the getting.

But let me take it a bit more slowly.

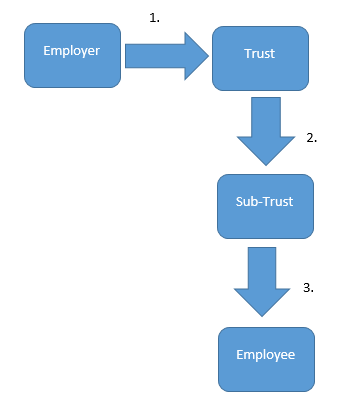

You might think about the Rangers transaction as looking a little like this. (And sorry for my home-made diagram. You need to make allowances for us lawyers.)

What happens at 1 is that the employer gives money to the trust – think of it as a big pot – for all employees. At 2 the trust gives money to the sub-trust – a smaller pot – for a particular employee and his family. And at 3 the sub-trust lends the money to the employee.

So when does the employee “get” the income? When does he have a liability to pay income tax?

Of course he gets his hands on the cash at 3. But all the courts so far have held that what he has is a loan of the money – which he may need to repay.

And at 2 the money is passed to the sub-trust for the benefit of the employee and his family. But all the courts so far have held that the employee hasn’t got it – because the trust might decide to give it to someone else – for example his daughter – instead.

Now everyone involved kind of knew the money would just flow straight through from employer to trust to sub-trust to employee. And the loans don’t look the same as a loan you might take from a bank – no-one’s been demanding that the loans should be repaid. So you might feel that what the courts have held doesn’t have much reality to it. But as I said on Good Morning Scotland, the law isn’t always about common-sense.

And what’s more important now is that they’re not conclusions a judge can overturn on an appeal.

So what about at 1? Might there be a payment there? Because the new argument HMRC advanced before the Court of Session was that the employees got the income at 1.

But how, you might ask, could they have got it at 1 if they didn’t get it at 2? Isn’t it odd that at 1 it could have been given to any employee but at 2 it could only have been given to the employee or his family? How could it be the employee’s income at 1 if it wasn’t at 2?

Well, the answer the Court of Session gave was this.

You can satisfy the “getting” bit of the test for a liability for income tax in two ways. You can satisfy it if you get the money yourself. Or you can satisfy it if you agree that it should be paid to someone else.

There’s definitely something to this argument as a matter of principle.

Think about it this way. Most of you won’t receive your wages through some complex EBT structure. Most of you will receive them directly from your employer. And you couldn’t avoid income tax on them by agreeing that they should be paid into your daughter’s bank account rather than your own.

And what the Court of Session said had happened here was, in effect, that the employees had agreed that they should be paid into the EBT (at 1) rather than to them. And by agreeing, they had satisfied the requirement that they “get” the income.

But, although that might be right in principle I have some problems with the practice.

The first is that the Court of Session seems to me to see the “getting” requirement as a problem to be solved rather than a key part of the question. And I think this may have led it to the second and third problems.

The second is that the Court of Session is not terribly clear – or not terribly clear to me, at any rate – about where you can find the agreement that someone else should be paid the income.

But I should also make this point. There were two different types of arrangement before the Court of Session: one for footballers and one for managers. And this criticism I have advanced of the Decision may be stronger for managers than for footballers. Because footballers did enter into an agreement (called a side-letter) when they signed with Rangers in which they seem to have agreed that payments should be made to an EBT rather than to them. But Managers didn’t sign an agreement – although they too were found by the Court of Session to have agreed.

The third is that we are taxed on our actual pay – and not on what we might have been paid had we negotiated a different package with our employer. We are free (at least if we do it right) to agree with our employer a package that involves us getting less stuff that does give rise to a tax liability (for example, pay) and more stuff that doesn’t give rise to a tax liability (for example, child-care vouchers or pension contributions). And if we make that choice then we pay (the lower) tax on our actual pay package rather than (the higher) tax on what we might have negotiated. I’m not sure that the Court of Session fully appreciates this.

***

It’s not easy for an outsider – like me – to look at a case and say what the answer should be. The answer is often quite sensitive to the facts. The advocates arguing the case – and the judge or judges hearing it – know those facts better than the outsider does. And that’s a particular problem in this case. I’m not sure why – perhaps it’s because the Court of Session decided the case on an entirely new argument – but the facts relevant to this new argument are not terribly clear from the Decision.

So, although I stand by the problems I have set out above with the Decision, it is perfectly possible that my analysis is wrong. You know this, of course. But it’s important that I say it.

***

But actually my views are not nearly as important as what happens next.

If there is an appeal to the Supreme Court either I will be proved wrong or I will be proved right. And whatever my view is now will be irrelevant.

And if there isn’t an appeal to the Supreme Court then the fact I think the Decision is wrong will also be irrelevant – because it will remain the Decision. And no-one will care if someone somewhere (me, for example) thinks it’s wrong.

So will there be an appeal?

I don’t want to speculate about the financial position of whoever’s running the litigation. There are other people around who are better informed than me on that subject.

But if there is money to fund it I’m pretty sure there will be an appeal. It would be an odd decision to stop at your first loss, having won twice. That’s especially true where you’ve lost on a ‘new’ point. And it’s especially, especially true where that new point is controversial. I can put my hand on my heart and say that all of the tax professionals I have spoken to about the Decision find it difficult to see how it can be right. They might all be wrong – but that sort of sentiment towards the Decision is absolutely going to encourage rather than discourage an appeal.

***

Thanks for sticking with me this far. Even I know that tax is less fun than football.

I know it now, anyway. So I appreciate you sticking around. And I’ve enjoyed engaging with many of you on twitter.

Please come back for Part 3 where I’m going to talk about what I find particularly interesting about this case. Which is what I think it tells us about who the real winners and the real losers are from this kind of tax avoidance.

Follow @jolyonmaugham

Well done, something even a Scottish investigative (alleged) journalist must surely be able to grasp, although having had the misfortune to hear Cowan/Spiers/Cosgrove spouting bile and propaganda on BBC Scotland I could be wrong on that. They still insist EBTs are illegal…lol

Income or non income, that is the question? Or understanding of such income? Great blog, looking forward to part three.

http://www.bbc.co.uk/news/uk-scotland-glasgow-west-34118126

2 managers and 2 assistant managers all with side letters.So are you admitting that the side letters are a problem?.

I think that the discussion shows that some people think that form is more important than what commercially happens. Sarcastically, I could say that these are the people who tend to think that capital gains tax is a tax on arithmetical differences and not a tax on gains. I think the Court of Sessions has shown that it thinks that employment income tax is a tax on the earnings that have come from the employment (with ‘earnings’ being the equivalent of the ‘gain’ rather than the ‘arithmetical difference’). So I think the decision is right from a big picture perspective (i.e. the wide s62) as well as common sense. And I think that while the law isn’t just about common sense, that should be a part of any judgement.

As you say, things are very fact specific and there were plenty of these found by the FTT. If my employer tells me (or Mr Yellow) that they are ‘thinking of’ paying me a bonus of £100 or paying £100 to a trust for the benefit of my family, what would I prefer, and I say the trust then doesn’t that fact pattern make the decision sound right? If it was done the other way around (we’ve decided, where do you want it paid?) it would clearly be earnings. But why, when there has clearly been a provisional decision on the payment of the bonus by the employer, should the order matter? If so then we’re back to the arithmetical view of what is taxable.

Oh, when I read your first post on this, I read it as if Joan was your bare trustee until she gave you the savings book, which obviously gives a completely different meaning to ‘getting’ to the one you had. I wonder which one Joan had in mind?

I am not “admitting” anything. I am not making an argument, I am trying to explain. Ask me your question taking that fact into account and I’ll answer it.

I agree with you completely. I have never met a member of the Revenue Bar that is comfortable with an honest, common sense judicial approach to tax avoidance. I thought it was disappointing that Jo failed to declare his interest in the contiuance of the formalistic approach seeing as the common sense approach adopted by the Court of Sessions would easily defeat schemes he had defended in the past and will no doubt defend in the future, Eclipse 35 being one example.

You couldn’t think I was guided by self-interest if you had read this https://waitingfortax.com/2015/05/01/tax-avoidance-and-me/. And what do I have to gain from – as you come close to implying – attempting to mislead Rangers fans about what’s going on here? I have no interest at all in the outcome – and in my pieces I am not arguing for an outcome. I am just explaining the Decision a I see it.

In the original decision of the FTTT the QC representing the HMRC did not dispute that the loan documents were legitimate loan documents

How does this sit with this latest decision,as this was said to be a major reason why HMRC lost

Page 44 paragraph 191

“Further, the legal effect of the trust structure and loans (all of which, it was conceded, were not in law a sham)”

Click to access TC02372.pdf

It narrows HMRC’s ability to argue that the “getting” was at 2 or 3. It narrows it but does not entirely exclude it because what the decisions talk about as “Ramsay” is an alternative to sham.

The sham doctrine is concerned with individual ‘transactions’ that constitute a scheme considered in isolation; in reality they are meant to work together to ‘produce’ the tax advantage. So, there’s no harm in conceding that the individual transactions are not sham and arguing that the scheme as a whole is “a nullity”, which was what Lord Wilberforce held in Ramsay.

That is true – narrows but does not exclude. Exactly as I said.

You positioned yourself as an uninterested party and I don’t doubt your integrity in any way. But you’re presenting a point of view that fits your professional interest and you should have made that clear; or at least avoided the impression that the approach taken by the Court of Session is unprecednented. That is the message many Rangers fans seem to be getting and they are clearly feeling victimised. How many of the Rangers fans hailing you as completely independent would understand your entirely legitimate role in a case like Eclipse 35? I seem to remember that the Telegraph attacked you (very unfairly in my view) on this in the run up to the general election before you were forced to defend your position. If you had been upfront about it from the start they would not have had that ammunition. So, in the interest of public understanding of the oddities of the tax world, I thought you should have explained the relationship between the common sense approach adopted by the Court of Sessions and your approach in cases you’ve been involved in (and as I said would be involved in in the future). You don’t want hand a hostile ‘investigate journalist’ another ammunition. That’s all I meant to say. And I am HUGE fan of yours.

Would this mean that as it stands this ruling makes the loan documents invalid? would any appeal be based on challenging the fact that a new argument should not be allowed at this stage as I understood that any appeal would be on a point of law that had already been disputed or an error

No, the loan documents are still ‘valid’. But the fact that the Court of Session has held that there is a “getting” at 1 means that the validity of those documents is irrelevant.

Rangers may argue it is too late to take the new point now. But they would want to be pretty clear they were right – because it’s quite an ugly thing to do: to try to stop someone running an argument which they have won on.

How does it fit my professional interest? Where do you think it has affected the quality of my analysis – given that I have explained very clearly that the Court of Session’s approach does have common sense appeal? And what should I have stated over and above that I do work in the field of EBTs?

It is very easy to play the man. Anyone can do it. But it demands real justification.

“Common sense appeal” but not legal appeal? What was Ramsay all about? You’re of course entitled to comment on a judgment but it’s disingenuous to dress your (self-serving) commentary as an (independent) explanation. The Court of Sessions explained their decision and their explanation is clear enough for most people to understand.

Are both parties allowed input to these appeals or is it only the party that is appealing the judgement

I’m giving that comment a yellow card. Temper your tone about me to that which is within the bounds of reasonable or I will no longer accept your comments.

Both parties can argue in the appeal.

Does the letter of indemnity make the use of the EBT scheme invalid?

No. I think it may well be irrelevant to the legal analysis of the EBT structure. Although it may – not likely but it may – have an impact on who actually picks up the tab if Rangers ultimately loses.

I’m sorry if that’s how you feel about it. My last comment – an advice if you like – is that you should perhaps be more mindful of the inherent unfairness in this sort of interventions – criticising judges that can’t defend themselves in BBC studios, online blogs and on Twitter – and of the wider implications of lending credence to the attacks the judges will inevitably receive from Rangers fans on a matter like this.

Do you think it likely that BDO will appeal?

The fact that this decision gives HMRC the precedent they were looking for (although having read that all EBT’s are different, can the decision be used as a precedent?) do they have an obligation to appeal?

If the decision has an impact on other cases, and given that all the companies under the Murray umbrella that the decision affects are either liquidated or in the process of being liquidated, can another “interested party” appeal the decision?

You say that as though this blog were the only format in which professionals express views about whether judges have got it right; and as though I had done some hatchet job. Neither of those implicit assertions bears any remote connection to reality. When I want your advice, John, on how to communicate with the public I will come find you and ask you for it.

Perhaps you think that comment on judicial decisions should best be expressed in Latin maxims in the pages of august professional organs? Perhaps you think I shouldn’t be trying to explain it to those whose lives are affected by it? Perhaps you think they won’t really understand the issues?

I’m only saying that you should disclose the fact that your life would also he affected by it. If the courts should revert to or indeed strengthen the original fiscal nullity version of the Ramsay principle (which is what the common sense, real-world approach of the Court of Sessions indicate) there’ll be significantly fewer tax avoidance cases and much fewer work for every member of the Revenue Bar. That, I suggest, is where the self interest of all of us that work in tax, resides. So, to claim that we’re completely independent on these issues is simply not true.

I disagree,are trusts not supposed to be independent of the employer and have discretionary power?.If a player has a letter which shows he must be paid then the trust must pay or rfc2012 plc (formerly known as rangers football club in liquidation) would be in breach of that players contract.

Who would be liable in those circumstances,the trust who refused to give the player his (cough) loan or the club who agreed to pay the player what he has stated in his contract and side letter.

No indepedence or discreation means the EBT scheme is not workng the way you describe it should.Perhaps that is why DM changed trustees as equity seemed to be getting a bit nervous of the way he was doing things.

Good analysis (even for us alleged tax specialists) and I think I would count myself in the ranks of those who consider the decision to be incorrect. In the context of applying this decision to the thousands of contractors who continue to be plagued by a 10 years and counting HMRC “investigation” I think it has limited value?

As you say the decision was based on its facts and the “new” argument was very specific to those facts, unclear as they are. HMRC had to show that liability arose at step 1 because the tax at point was PAYE via a regulation 80 determination. I don’t know if the managers/players have had individual assessments but these are not mentioned so perhaps HMRC was limited.

For other contractors, HMRC has raised assessments on the unsatisfactory “other income” rules to tax loans drawn. If it is the case that the ONLY decision supported is one to pin a liability on an employer for PAYE, then it’s hard to see how an individual recipient of loans can be taxed?

It’s also interesting to note that HMRC has yet to make much of the decision and usually such victories are shouted from the rooftops. Perhaps the nudge unit is busy elsewhere and next week will see this?

Looking forward to part 3.

Whilst this has indeed been an interesting discourse on courts applying a purposive or ‘common sense’ construction of evidently artificial arrangements, I don’t think you have fulfilled your stated brief here. You main stated audience was the fan-base of Rangers FC, helping understand a little better what has happened to their club. Do you not think you are misdirecting them slightly by concenrating so much on your ‘getting’ argument? This focuses your attention on to the recipient – the INTENDED recipient! – and away from the tax effects for the employer. Frankly Rangers fans.are uninterested in what happens to.an ex – player from nearly two decades ago they are interested in any liability to pay HMRC a large amount of money, be it CT or Income Tax or NIC withheld amounts.

We’re going round in circles. Those who are interested in my response can read my previous answers.

If there’s no “getting” there’s no income tax liability for Rangers at stage 1. It’s often missed but it’s the employer not the employee who (almost invariably) bears responsibility for failing to apply PAYE correctly. So I disagree – I think it is entirely appropriate to focus on the “getting” argument.

Leaving aside whether or not your analysis of this specific case is correct, what your article serves to highlight is the anomalous position of trusts regarding taxation. Why isn’t the payment at 1 subject to assessment?

Further, although you mention reducing tax liability by choosing to receive other forms of remuneration, this is to ignore the benefit-in-kind view of things. If the ultimate destination of the payment is clear, then it ought to be viewed for tax in that light.

Perhaps the publicity here will help to get things changed for the better.

You miss the “self evident” point. It it’s theirs at 1.(as you say) then its theirs at 2, 3 a,b, z,x or y no matter what tortuous route it takes. It could not have went to any employee at 1. as that was what the side contracts were for. On signing for rangers a letter went immediately to the trust recommending a sub trust set up for the amount in the side contract. You haven’t read Heidi Poon have you?

Pingback: Tax Research UK » Rangers’ EBT: why the Court of Session got it right

The reason payment at 1 isn’t taxed is that is can’t be allocated to anyone (usually). No one is suggesting that a contractual bonus can simply be redirected to a third-party to avoid tax. Hence the position for the managers being stronger. As an aside those who purport the common sense approach. Common sense should tell you this decision is flawed. It it was common sense and obvious why wasn’t it run in the first two rounds of litigation, or in sempra or dexta ( which are distinguished on a dubious basis). It was a desperate argument and it it a poor reflection on the court of session that it was successful. the facts of this case are either so specific this simply doesn’t have wide application, or we just allow HMRc to ignore statute and case law, and let them do what they think is best – which is what this decision implies.

The side letters destroy your argument completely.

I’m afraid if you take these so called side letters and factor in the Ramsay Principle that at least in those cases where side letters were issued this situation is clearly tax avoidance and not tax management.

The trusts are based on the payments being discretionary, both at the point of the money going in and on the loans being granted. The side letters negated the discretion at both parts, making those EBTs fail.

The CoS took the simple view that as soon as the payment went into the trust the player had received total control over the money, making the whole trust structure purely a mechanism to avoid tax as it served no other purpose. That is where they “got” their payment.

It’s classic avoidance, taking a scheme designed for one thing and using it for another. In essence to minimise tax due. The CoS, like Dr Poon saw through the sham and ruled as such.

Who in your opinion Jolyon, would be the best QC in the land to appeal this ruling to the Supreme Court?

I’m going to take the Fifth on that one. But there are several candidates – if money is no object.

Haha is that a filth of the commission? seriously though throw a few names in the hat.

I would guess most tax experts’ idea of the leading, proven, tax litigation QCs at the moment would be Kevin Prosser and Jonathan Peacock

Subsidiary question, if you don’t mind. How likely do you think it would be for the Supreme Court to reach a “split decision”. For example finding that where there was a side letter tax was due at the point of payment into the trust.

However where there was no side letter the EBT succeeds and tax does not fall due unless the beneficiary decides to take the money out of their sub-trust as a payment rather than as a loan, which I believe is open to them.

Personally I think that if the decision is made that side letters cause the EBT to fail then that would be extended to the smaller number where no such letter was led as evidence. I’m assuming they are working on a balance of probabilities proof here.

Crowdfunding to pay their bill ?

Great articles thank you for the extra information.

So in your view could they enforce the players (employee) to pay back the paye tax or would it sit with Rangers (employer)?

A question on the proceedings Jolyo : you (sort of) distinguish between Rangers and the other Murray companies on the basis of the Rangers side letters. As dsr as you know, did the other companies ever try to.draw any distinction on that basis?

Thank you for your interesting article Jolyon, looking forward to part three. I have three questions if you don’t mind:

1) Do you think the much weakened state of Murray’s companies (ie. Murray Group/MIH being wound up since the start of this year) had any bearing on HMRC’s decision?

2) As HMRC decided to use ‘common sense’ to reach their decision, could a subsequent appeal not then also use the ‘common sense’ approach in that, Rangers use of EBTs were fully declared at the time and cleared by financial and legal advisors, the football authorities, auditors and HMRC?

3) It has been said that only Murray or BDO can appeal, is this correct or could a third party (eg. shareholders of the old company or fan collective) lodge an appeal?

Thanks.

As to your 1), nothing’s impossible but I’d only harbour that as a serious possibility if Murray were in weakened state when this saga began. As to 2), I don’t think so. But if common-sense is relevant, I don’t think it helps Rangers in the way you describe. I’m not sure it’s common-sense that by HMRC behaving as you describe they conceded that the arrangements ‘worked’. As to 3) I don’t know the answer, I am afraid. But it is a very reasonable question.

Great question. I would also be interested in your reply to this Jolyon

First of all, wonderful blog posts and look forward to part three.

Couple of questions if that’s ok?

1. When can we expect part 3?

2. What do you think will happen to David Murray personally? Apparently he was the biggest beneficiary so will HMRC go after him personally as an ex Director, even though his business and ultimately his employer is in liquidation? Has this win helped HMRC or hindered them technically, to go after Directors personally and is it different if the business is in liquidation?

As to 1. Pt 3 later this week. Have thought about what I want to say but have not yet started writing. When I know, I’ll say on twitter.

As to 2. I may say something about those responsible in Pt 3 but anything I do will be a moral rather than a legal observation.

I suppose where we differ is that I simply don’t understand how an appeal court can be right in principle but wrong on the technicalities.

To step back a moment, the law, in theory, is made by the public acting though their elected representatives in parliament.

In a democratic society the role of a judge should be to uphold the will of parliament though their decisions.

That will occasionally mean that the court will say – look you may have dreamed up this awfully clever scheme that you think complies with the letter of the law, but that scheme clearly goes against the intent of the public when they made this law and we will strike it down.

That is clearly the extent of judicial discretion in advancing common law and in exercising that discretion they will often rely on common sense, because in effect it is the common sense of a law which it is their job to find.

I am fairly sure that it was not the intent of parliament to allow companies and individuals to get out of paying income tax by putting money into an offshore trust which was loaned to the employee on the basis of a prearranged agreement. If that had been the intent of parliament there would have been an expressed exemption for that kind of scheme in legislation.

Would you not agree?

Also – how does any of what you have said take away from the obligation of the employer to withhold tax when making a payment into the trust? The Court of Session made the argument that the agreement from the player that payment should be made into the trust meant that the actual payment into the trust constituted payment of employment earnings by the employer. They therefore had to pay PAYE when paying into the trust. I am not clear on where you take issue with the court’s conclusions on the obligations on the employer.