As of yesterday, the OBR’s expected deficit (or Public Sector Net Borrowing) for the year ending April 2015 was £90bn: see OBR table 1.3.

Here’s a chronology of some earlier forecasts.

22 June 2010: George Osborne delivers his Budget forecasting a deficit for 2014-15 of £17bn (table C.6). He fell short by £73bn.

12 October 2010: George Osborne confirms his aim of eliminating the deficit by 2015. He fell short by £90bn.

23 March 2011: George Osborne delivers his Budget forecasting a deficit for 2014-15 of £46bn (table C.8). He fell short by £44bn.

29 November 2011: George Osborne delivers his Autumn Statement forecasting a deficit for 2014-15 of £57bn (table C.7). He fell short by£33bn.

21 March 2012: George Osborne delivers his Budget forecasting a deficit for 2014-15 of £52bn (table D.6). He fell short by £38bn.

29 November 2012: George Osborne delivers his Autumn Statement forecasting a deficit for 2014-15 of £62bn (table B.6). He fell short by £28bn.

20 March 2013: George Osborne delivers his Budget forecasting a deficit for 2014-15 of £71bn (table B.6). He fell short by £19bn.

5 December 2013: George Osborne delivers his Autumn Statement forecasting a deficit for 2014-15 of £84bn (table B.6). He fell short by £6bn.

20 March 2014: George Osborne delivers his Budget forecasting a deficit for 2014-15 of £95bn (table D.5). He overshot by £5bn.

3 December 2014: George Osborne delivers his Autumn Statement forecasting a deficit for 2014-15 of £91bn (table B.5). He overshot by £1bn.

18 March 2015: George Osborne delivers his Budget forecasting a deficit for 2014-15 of £90bn (table C.5). He gets it right.

8 July 2015: George Osborne delivers his Budget forecasting a deficit for 2014-15 of £89bn (table 1.2). He falls short by £1bn.

The purpose of this exercise is not to be rude about George Osborne’s – or the Office for Budget Responsibility’s – forecasting skills.

Forecasting is a tricky business. However well run, and independent, the OBR is.

So why does any of this matter?

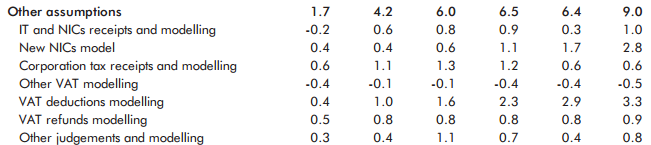

Well, as is now well understood, yesterday the Chancellor got a £33.8bn windfall, mostly from modelling changes but also some modestly improved forecasts of receipts (see Table 4.8).

And that’s a £33.8bn change in OBR forecasts since July.

And he’s already spent two-thirds of it, according to the Resolution Foundation.

Spending it is bold, given the OBR’s forecasting record. You have to really want to believe – really want to – that all of those earlier forecasting errors were anomalous. And that now, at last, the OBR’s going to get it right.

I’m not saying Osborne was wrong to slow the pace of spending cuts (as those on the left put it) or spend more (as those on the right do). I’d be ejected from the Labour Party if I said that.

It’s more that all of this bouncing around from Osborne feels a touch… unstrategic. An opportunistic, rather than a long term, economic plan?

Well, at least the forecasts gradually get closer to the (final?) figure, subject to some inevitable uncertaintly.

Is the most recent OBR figure still an estimate? Do we still not know the final deficit for 2014-15, nearly 8 months after the year end? Surely they know what was collected and spent last year? Do they need to wait for tax revenues for the 2014-15 tax year to roll in before they can say for certain? When do figures for prior years stop moving?

It always amuses me when the Chancellor confidently reels off various series of numbers for each of the following 5 years, as if he is laying down established fact rather than (at best) an educated guesstimate. Events, dear boy. Bombing Syria will be expensive.

You say he has already spent two thirds of the accounting adjustments. To what extent has be really “spent” any amounts expected in 2020-21 already? Earmarked, perhaps?

Accepting the uncertainty of forecasts should itself be part of the economic forecasting strategy. These budget variances largely hinge around the extent to which actual GDP growth varies from what has predicted.

There is a culture that forecasting low growth is defeatism that will attract the derision of the opposition, for its paucity of ambition.

Why not instead take growth out of the equation, plan for the consequential higher tax levels that would be needed to balancr the books in the early years, and then, after ‘banking’ each quarter’s achieved growth rate, re-cast the forecasts to reflect the money that really IS spare?

Barring growth actually going negative, this would then permanently remove the element of nasty surprise and consequential sharp braking on spend.

The boring predictability of it all must be worth a lot, in terms of being able to plan over a long term.

Reblogged this on perfectlyfadeddelusions.

Actually the £38bn has nothing to do with changes in forecast GDP growth.

But your fundamental point is one I think a prudent Chancellor absolutely would take into account…