In October, I wrote this post. It made five points.

(1) I explained why I believed Uber was supplying transportation services.

(2) I set out what that meant in tax terms – Uber was liable to pay, but was failing to pay, hundreds of millions of pounds in VAT every year.

(3) I explained that HMRC’s ability to collect that unpaid VAT was time-limited – as time passed, HMRC lost the ability to collect those hundreds of millions of pounds for the rest of us.

(4) I argued that HMRC should raise assessments to protect its position in case the various cases before the courts confirmed Uber was supplying transportation services.

(5) And I said that HMRC’s failure to do so was remarkable – it indicated serious wrongdoing at HMRC.

Points (1) and (4) were, shortly thereafter, put to HMRC by the Public Accounts Committee (see, from Question 88, here). But what did HMRC say by way of response? And does that response hold water?

(1) Is Uber supplying transportation services?

The basis for arguing Uber is liable to VAT is that the economic reality is that it is supplying transportation services as principal not as agent for the drivers.

Explaining why HMRC is not pursuing Uber for VAT, here is what Jon Thompson, Chief Executive and Permanent Secretary of HMRC, said to the Public Accounts Committee:

But as the Employment Appeal Tribunal in the Uber case pointed out:

Which side of the divide an individual falls will inevitably be case- and fact-sensitive. That, indeed, is the message I take from the various “mini-cab” cases I was referred to in the VAT context. Most are first instance decisions and not binding on this Tribunal, but, in any event, what they show is an attempt to determine in each case whether the drivers were providing their services as such to or as part of another entity (the taxi firm) or directly to the passengers as their clients or customers.

(And earlier, at para 81, the Employment Appeal Tribunal had observed that in agent/principal VAT cases involving taxi services “the decisions went both ways.”)

What is remarkable and unique about Uber’s arrangements is the degree of control it exercises over the drivers and the arrangements with customers. These are the factors that led the Employment Tribunal to conclude (and the Employment Appeal Tribunal to agree) that drivers were workers supplying services to Uber, the principal. These are the factors I consider would cause a Tax Tribunal, too, to conclude that Uber was a principal for VAT purposes. In other words, it is clear that there is a line in agent/principal VAT cases involving taxi services and if any case falls on the principal side of the line – and we know that some do – you Uber’s should.

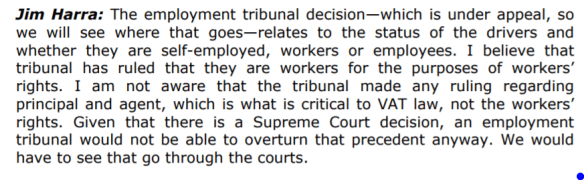

Jim Harra, Second Permanent Secretary to HMRC, went on to make a further point about the Uber Employment Tribunal decision, as it then was. He said:

But this, I am afraid, is simply wrong.

It is true that the Employment Tribunal decision is about worker status. And it is also true that the VAT question is not identical to the worker status question (it may very well be as a matter of law that the threshold for VAT is lower than the threshold whether the drivers are “workers”). But it is quite wrong to say the Uber case is not about principals and agents: if workers are supplying their services to Uber it follows that Uber is not an agent vis-a-vis the customers.

You can see this very clearly from the Employment Appeal Tribunal decision:

(4) Should HMRC make a protective assessment?

The Public Accounts Committee also put to Jim Harra, Second Permanent Secretary to HMRC, that he should raise a protective assessment to protect the position of taxpayers generally whilst the matter was resolved. To this he said:

The power to make protective assessments arises under section 73 of the Value Added Tax Act 1994 “where it appears to the Commissioners that [here, Uber’s VAT returns] are incomplete or incorrect, they may assess the amount of VAT due from him to the best of their judgment…”

But does HMRC really have no power to make a protective assessment where they wish to protect their position whilst they wait and see what the law is? Is Jim Harra right that HMRC can only make an assessment if it believes the sum in that assessment is due and that if this leads to hundreds of millions of pounds of tax being lost then so be it?

This is a striking contention, and one which flies in the face of common sense. Why should the law require that HMRC sit on their hands doing nothing whilst other cases roll through the courts and hundreds of millions of pounds of tax owed to the general body of taxpayers are lost?

It flies in the face of common sense. And it is also, as it seems to me at least, wrong.

When confronted with facts which give rise to two possible tax treaments – X and Y – it is HMRC’s routine practice to make assessments in the alternative: one for X and one for Y. HMRC then argues those assessments in the alternative: it says ‘we think that X is right but if we are wrong then we say the liability is as described in Y’.

This practice has been blessed by the courts on numerous occasions: see, to take an example from the Court of Appeal, Courts plc, approving the decision of the Court of Session in Glasgow which concerned alternative assessments made under section 73. But if Jim Harra is right then the Court of Appeal and Court of Session are wrong: HMRC has no power to make assessment Y because it believes that it is sum X which is due.

Indeed, the Courts plc case itself concerned a protective assessment raised precisely because HMRC was concerned that the slow progress of other litigation jeopardised their ability to raise assessments within a statutory time limit

There is also a profound tension between what Jim Harra told the Public Accounts Committee and HMRC’s own published Litigation and Settlement Strategy which states:

In other words, there are circumstances where HMRC will take a case to litigation even where it believes it is unlikely to succeed.

Summing up, neither of the answers given by HMRC to the questions put by the Public Accounts Committee seem to me to bear examination. They look to be answers driven by a desire to explain away their failure to act. I expect to release, shortly, direct and good quality evidence that is in my possession that HMRC is motivated by improper reasons in failing to act against at least one large multinational tech company.

In the circumstances, I remain of the view that, as I put the matter in my blog post of October:

I can see no good reason why HMRC should adopt this stance. None at all. It is inexplicable to me – unless HMRC’s conduct is motivated by factors otherwise than collecting the tax demanded by the law. I do not know what those factors might be. But this smells very bad.

HMRC said one last thing to the Public Accounts Committee:

Since that oral evidence was given, Uber has lost its appeal against the Employment Tribunal decision. And yesterday it lost the case in the Court of Justice of the European Union that Jim Harra referred to. Both the Employment Appeal Tribunal and the CJEU held that Uber was supplying transportation services.

We must hope that HMRC now takes the steps it has indicated it will to ensure Uber is subject to the same tax law as the rest of us. In the meantime I will continue to pursue my action against Uber and my actions against HMRC (see here and here) to establish Uber’s liability to pay Value Added Tax.

Pingback: Uber: HMRC and the Public Accounts Committee | Waiting for Godot – leftwingnobody

Pingback: HMRC should be hanging their heads in shame over Uber

Well done for doing this – couldn’t agree more with what you say. Look forward to your revelation as well.

All I can say Jolyon is ‘Go for it’. HMRC is a disgrace.

You’ve misrepresented what Harra said. There’s a big difference between saying “We think that X is right but if we are wrong then we say the liability is as described in Y’ and ” X could be right though we’ve lost when we’ve argued similar points before, but if we are wrong then the liability is zero and we’ll be liable for a lot of costs which will have to come out of public money”. And what about all the other small cab firms who operate on a similar basis? Are you suggesting that somehow if you’re right, it’s only Uber who’ll be liable to start charging VAT? Not sure I’d be too happy if my minicab starts costing me an extra 20% on top…

Blogged on the ECJ decision here https://medium.com/@StrongerInNos/uber-developments-a80e63d116ab

tl;dr version of blog – Question was whether Uber were making any supply ‘in the field of transport’ as they needed city authorisation if so. Advocate General said the Uber app and the actual taxi ride were part of a single supply of transport made by Uber – so yes. Court found that the app was itself a service ‘in the field of transport’ – so yes too, but for this different reason. Court’s Conclusion didn’t say anything about whether Uber was providing the actual transportation too, but that isn’t any reason for HMRC to disregard the AG’s more extensive analysis.

AG Opinions are an academic analysis, however well reasoned. They aren’t a statement of the law unless endorsed by the CJEU. Consequently they are of limited value and in running a legal argument you can only rely on what the Court itself has held.

Pingback: Uber: HMRC and the Public Accounts Committee | Barking at cars