Sandwiched between the rise in Insurance Premium Tax (which raises between 2015-16 and 2020-21 the sum of £8.16bn) and the increases in the rate of tax payable on dividends (which, over the same period, raises £6,785bn) is this measure:

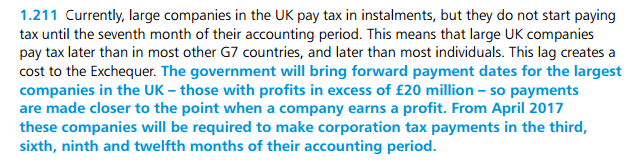

![]() which over that period apparently delivers £7.83bn of new tax receipts.

which over that period apparently delivers £7.83bn of new tax receipts.

What, you might well ask, is this? Further detail is provided here:

So this £7.83bn isn’t new money at all. It’s tomorrow’s corporation tax receipts, that we’re getting today instead. But because receipt of it is being accelerated into 2017-18 and 2018-19 we can all pretend that financial security has been delivered unto us:

This isn’t the first time the Tories have pulled this trick either. It was delivered to the tune of £10bn in the last Parliament too (as I explain here).

The bank loss restriction was a temporary timing difference which should naturally reverse when the losses that were blocked in earlier periods are claimed in later periods.

But surely this one is a permanent difference – after the change, the cash always arrives sooner. So we get some of next year’s cash this year, and some of year 3’s cash in year 2, and so on. No? (Perhaps I am missing something – when does this change reverse?)

It’s a con that politicians of every colour have pulled many times before and will continue to. I’m sure you have acknowledged this before, why the party political bias now on a day that the Tories have delivered more Labour policies than Blair or Brown?

You may be right. I have removed the point. Thanks.

Not sure I have – but then I have only relatively recently become interested in tax policy.

Sorry, my point was not just that this change won’t naturally reverse itself, but also that there it is an actual one-off cashflow advantage to the Exchequer in getting the tax in earlier, somewhat similar to a windfall tax.

Still, lucky that this advantage arrives in the next five years, eh?

Another way to think of it is as a factoring of future receipts. Which we treat as being on P+L rather than B.S.

Why is the OBR quite content to sign off on rubbish like this?

Because they’ve got a narrow brief, as does Treasury. And the Tories are bright enough to know what questions to ask.

I’m with Andrew. If you merely factor trade receivables, that might not affect the timing of P&L recognition of the underlying income, on the basis that it does not change the period in which that income is appropriately viewed as earned. (The P&L entry that does result is the finance charge / factoring cost inherent in the difference between the price received for the receivable and its face value.) But in changing the rules here, the government really is accelerating the time at which it earns (perhaps not quite the right word!) its tax revenues.

Yep. It’s like a farmer getting a one off extra crop of apples. Which is fine if he does not use the one off sales proceeds to support an ongoing revenue expenditure line.