It’s a tough business trying to structure a sin tax.

Because your purpose is somewhat confused. Although we readily think of alcohol and tobacco we might also include amongst sins discouraged by taxation flying, quarrying, landfill and no doubt others too. Usually we tax exclusively to raise revenue but not so with sin taxes. Speaking of air passenger duty John Healy, in 2003 Economic Secretary to the Treasury, said in a written answer:

Air passenger duty was introduced in 1994 as a measure whose principal purpose was to raise revenue from the aviation industry but with the anticipation that there would be environmental benefits through its effect on air traffic volumes.

Are you trying to maximise revenue? Or dissuade commission of the sin? And if dissuade, how much? A little bit, presumably, because if you really wanted to dissuade, you’d ban it.

It’s tempting to say these considerations plague the design of sin taxes. But that would suggest, falsely, an elevated status for design. You either fudge it – no, you usually fudge it – or you take intellectual dignity from looking to raise a particular sum of money to spend on countervailing measures. Take this example from the 2001 Budget:

And they can be regressive, sin taxes. Can, because assertions that they invariably are (see, for example, from the Adam Smith Institute):

should be treated with some caution. It all depends on how they’re structured.

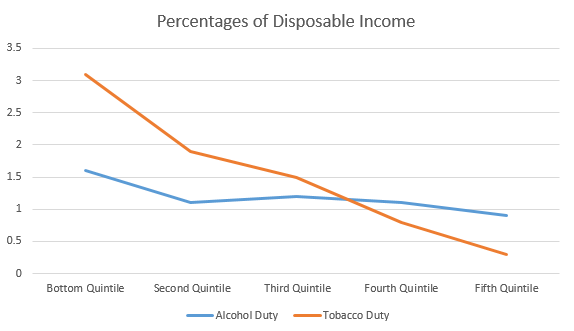

The proportion of your disposable income consumed by tobacco duty, for example, falls sharply as your income rises. But with alcohol, not so much (source: ONS).

Indeed, the percentage of our expenditure – as opposed to our disposable income – we expend on alcohol duty is absolutely static as we rise up the income scale (see Table 3(c)).

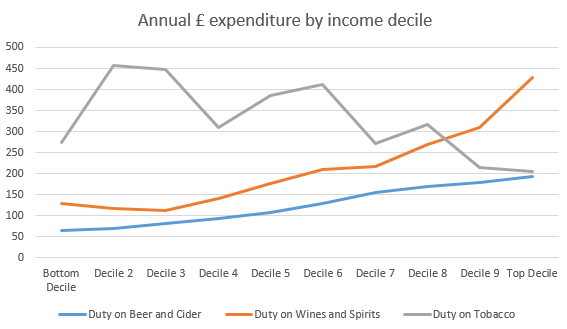

These points emerge even more powerfully if you look in cash terms (see Table 14).

So the rich smoke less, but drink more, than the poor. I know I do – and I’m pleased I’m not alone.

You’d want to be careful drawing conclusions from this data. But you might tentatively draw a few.

(1) It’s not taxes that discourage the better off from smoking. Although the disincentivising effect of tobacco duty declines as you rise through the income deciles still the rich smoke less. This lower propensity to smoke must derive from something else.

(2) People drink more as they can afford to (Oscar Wilde was wrong: work isn’t the curse of the drinking classes at all). And this suggests that alcohol duty does suppress consumption at its present level – and would suppress consumption more if raised.

(3) If you were inclined to conclude that the rich smoke less because they’re better educated as to the dangers of smoking you’d then have to answer the question why they drink more. This might drive you to conclude that social fashions play a part too.

Are there any implications for a sugar tax? Some tentative ones.

(1) You might start by noting that alcohol and tobacco have no (legal at any rate) substitute goods. The decision you face is to consume or not to consume. But increasing the price of sugary foods and drinks might more readily cause consumers – especially price sensitive ones – to switch to alternatives.

(2) The data on correlations between obesity and income is more complicated than you might think. Whilst for women obesity seems clearly to be correlated with low income the picture is less clear for men. But where there is a relationship, a sugar tax will be regressive – if it’s set at a level where the poor will pay it. The higher the level at which you set it, the more likely the price sensitive consumer will switch to products not covered by the tax. A sugar tax could easily be like alcohol duty – barely regressive at all.

(3) The mixed picture around alcohol and tobacco duties suggest that factors other than affordability are important too. Changing social mores may well rank high amongst them. Perhaps you would earmark revenues – as with the aggregates levy – to fund measures to achieve that change. And to offset the effect on the poor of price rises on sugary foods – by encouraging thrifty and health eating.

I think the key to making it non-regressive is to use any tax revenues to subsidies fresh or healthy food. After all the idea isn’t to raise tax revenue but to improve people’s diets, which will have massive benefits for the nhs.

One potential problem with the observation from these charts that the rich drink more but smoke less than the poor is that the data better support the observation that the rich spend more money on alcohol but less on cigarettes than the poor.

This does not necessarily lead to drinking more (though I have seen newspaper headlines about middle class drinking epidemics which I presume have their own evidential bases) since, of course, different alcoholic drinks cost different amounts – 5% cider available at £1 per litre or 12.5% vintage champagne at £2000 per 75cl. Rather than drinking increasing as income increases, it may simply be that people move from e.g ‘Vineyards Spanish Cabernet Sauvignon’ at 3.50 per bottle to ‘1998 Clos du Marquis, St Julien’ at 58 per bottle (here avoiding the issue of different alcohol duty rates as both are still wine at 12.5%).

If this is what the data actually show us, then it may not be that people drink more as they can afford to and that alcohol duty does not necessarily suppress consumption at its present level – and would not necessarily suppress consumption more if raised.

Cigarettes on the other hand however (though it doesn’t explain the actual drop in expenditure on tobacco) seem to fall generally within a range of 33-52p per cigarette which can obviously add up to rather a large difference on a consumption of say 20 cigarettes a day but is not anything like that available with alcohol (however cigars and ‘rollies’ may change the picture in ways which I haven’t taken into account).

The rich man and the poor man (not to mention the tailor, spy and thief) with the same 20 a day smoking habit are likely to have differing expenditures on this of at most £120 a month, whereas their half bottle of wine a day habit could cost c£800 more a month for the ‘clos du marquis’ rather than the ‘vineyards’.

Hi Ronan,

Respectfully, I think you’re missing that the charts for alcohol reflect duty – which is levied on the amount of alcohol – rather than price.

Jolyon

Yes I completely and utterly missed that – sorry for inflicting such a long reply with no basis!

Ronan

If you care, I’ll delete your comment and my reply… but it’s probably helpful to others to leave it there (and you are anonymous)?

No need to worry about that – unless a short note on it would help others under the same misapprehension see that it doesn’t apply without having to trawl through my screed…

Isn’t the question of a sugar tax made more difficult by the fact that the target audience for deterrence is children? If it is to prevent obesity, if a person can get through childhood without becoming overweight, they are surely less likely to become overweight in adulthood. However as children they are invariably not taxpayers and it is largely not their money which is being spent.

Isn’t the answer that Parents’ purchasing decisions will be affected by a sugar tax?

I was just about to make the same mistaken point – until I spotted this exchange. So it is useful!

I’m not too surprised that the rich drink more wine, but I’m impressed that they pack away more beer too! The exchange with RPM above was helpful for me, as I had also interpreted the second graph as showing total expenditure on booze and fags, not the duty paid by each decile. Is it really right that the top decile are drinking abount three times as much beer and abount three times as much wine/spirits as the lowest decile?

Surely there are many substitutes for alcoholic beverages – non-alcoholic drinks, of course. Perhaps we need a caffeine duty too…

Broadly speaking, smoking is a full-time job whereas drinking is done during leisure time. Does the change in the typical working environment as income rises have an impact on smoking such that it becomes less convenient to do so?

I’d guess not. But it’s just a guess. I think it’s about social acceptability.

I’d have been interested to see analysis of consumption of fossil fuels by income decile. Is this available? I suspect it would show carbon pricing as very progressive ‘sin’ tax.

I believe it is, yes. If you click through to the ONS spreadsheet, you’ll be able to work it out… Do let me know.

Interesting as this discussion is, I think the question of whether the tax would be regressive (alongside the question of whether there are other things that need to be done as well as a sugar tax) is a dead cat being lobbed about by the sugar industry for obvious reasons. If the future health implications of obesity are as bad as we are led to believe then the only question that needs to be answered is whether such a tax would work as part of an effective package of actions to reduce sugar consumption. The bulk of informed opinion seems to be it will help. So we should do it. If it turns out to have unforeseen negative impacts (which i doubt) it is reversible no? There are some areas of taxation where picking over the full detailed complexity is important for effective policy making. I am not convinced this is one.

You may be right. But (as is so often the case in our discussions) I feel obliged to say that being right is not enough. You also have to persuade the doubters – and some of them are worried and some of them say they are worried about regressivity. You can’t just ignore that issue and expect right to triumph because it’s right.

Respectfully yours,

J

The cynic in me says that the retail trade would simply take the opportunity raise the price of the untaxed can of diet coke to match the price of the less healthy taxed alternative.

That is true a lot of the time, especially regarding tax. But I think the sugar tax discussion might be different. But I’ll take the nod to my ‘rightness’ and leave it at that (even though I know you didn’t necessarily mean it as a compliment 🙂 )

OK – ‘Duty on hydrocarbon oils & Vehicle Excise Duty’ behaves by income quintile much like alcohol duties, but about twice as much.

It makes me wonder what are the significant luxury goods in the micro-economics sense of those on which expenditure rises faster than income. From the stats in that ONS spreadsheet, the only ones we tax are air travel, and property transations. Is there a comparable ONS spreadsheet analysing income by quintiles? That would give a cross sectional answer to the question. A longitudinal study referred to in a non academic article I read a while back shows, for the US, that property is overwhelmingly the dominant luxury good

How America Spends Money: 100 Years in the Life of the Family Budget

The implication is that of indirect taxes, only those on property taxes can be significant and progressive.

Perhaps worth noting that there is a form of sugar tax already, in that – unlike most food – confectionary bears 20% VAT. Not including cakes, of course, or biscuits other than those covered in chocolate. Similarly, most beverages are standard rated.

Pace pasty tax, one simple alternative to an explicit new sugar tax would be to move the lines dating back to the 1960s and before on what items are zero-rated (15% purchase tax was extended to confectionary and chocolate covered biscuits, but not cakes, in 1962 – see these debates: http://hansard.millbanksystems.com/commons/1962/may/16/clause-6-purchase-tax – great quote that “the Tory Party, in all their majesty, fully armoured and equipped, are descending on the children and relying on confectionery, soft drinks and sweets, etc., to secure the national economy for another year” – and http://hansard.millbanksystems.com/commons/1962/jul/03/clause-6-purchase-tax – complaints by the MP for Reading, where Huntley and Palmer was based).

We can’t extend the zero rate, but we can reduce its scope. So for example there could be a trigger extending VAT on, say, foods items with more than x per cent sugar.

Why are cakes and most biscuits zero rated anyway?