This morning saw the release of new Tax Gap figures for 2013/14. Here are some highlights.

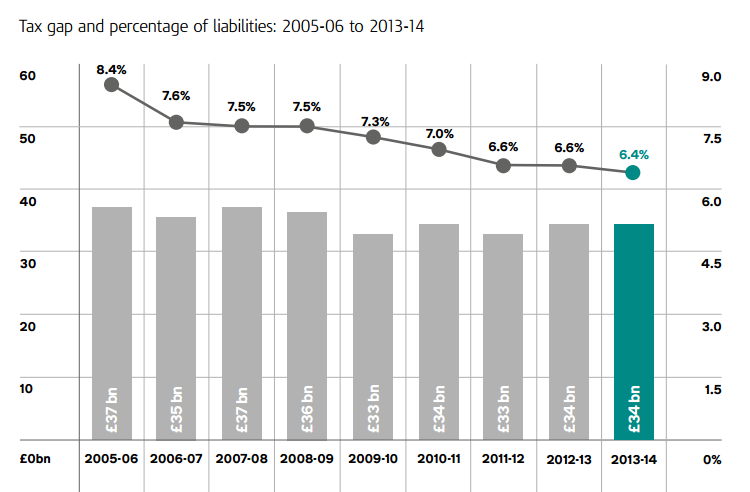

In cash terms the Tax Gap remained static at £34bn but in (the more meaningful) percentage terms it fell from 6.6% to 6.4%.

What can we ascertain from these figures about HMRC’s performance if we dig a little deeper? (This question reflecting, as I observed here, that the Tax Gap is better understood as a performance metric than an anti-austerian’s El Dorado?)

This chart probably sums it up best.

For me, the stand-out trends are these.

First, we are beginning – for the really radical measures will take effect only in the tax year 2014-15 – to see the fruits of the Coalition’s success in tackling personal tax avoidance. One can also see this trend (more starkly still) in the slump in the disclosure to HMRC of tax avoidance schemes (for those interested, I have discussed that slump here).

Second, we also see (in relation to excise duties) the effects of the very substantial cuts to HMRC’s FTE staff (more on this below) in the excise gap figures. The Summer Budget appears to have recognised the deleterious effects of these cuts:

(although the cynic in me notes that no figure was there given as to what that additional resource would look like).

But perhaps the most interesting question is what the future will look like. For we are, it seems to me at least, at an inflection point.

As I noted here, HMRC has sustained very substantial cuts in budget and staffing numbers since 2005-6:

My perception is that the progress – despite these cuts – in closing the tax gap reflects a number of different trends.

First, (see here and here) the Conservative Party is presently culturally better equipped to tackle avoidance and evasion than is Labour. The problems of avoidance and evasion are complex and will not be solved by a purity of moral purpose alone. Likely it is that my colleagues on the left will react to this assertion with outrage. But it is common ground across the left spectrum: see this, for example, which I co-wrote with Richard Murphy. And under Cobyn the problem has become worse not better as I noted here:

My intention is that Labour should react, not with outrage, but by recognising the issue and moving to address it.

Second, a consequence of their expertise is that the Conservatives have been able to alleviate the effects of cutting resource through some radical legislative steps: the General Anti Avoidance Rule, Follower Notices, Accelerated Payment Notices, Direct Recovery of Tax Debts to name but a few. There is much more to do – as the Conservatives rightly recognise – in particular around offshore evasion by wealthy individuals which, in consequence of campaigning work done largely on the Left (to which I have been a modest contributor), has risen up the political agenda.

But legislative steps are an imperfect solution. They are imperfect because they cannot address the resource heavy areas of smuggling, the shadow economy and so on. Technological advances – see this piece from the Telegraph on HMRC CONNECT – can assist but we also need investigators.

Perhaps more profoundly, they are imperfect because they create imbalances in the system. Over time they will erode – indeed, they are already eroding – the reputation HMRC has previously enjoyed for fair dealing. I hear this frequently from business leaders – and it is borne out by my personal experience too. If this situation goes unalleviated – and my conversations with senior HMRC staff suggest it will accelerate rather than diminish – it will cause serious harm to HMRC’s ability to collect tax and to the investment climate. This is a very real concern.

However, third, in the short and medium term, I expect these figures to improve. The tax avoidance figures next year will show the effects of the adoption in the Finance Act 2014 of a slew of radical legislative measures – and there is more to come from further legislation in subsequent Acts. And at some stage soon – although the current data records no such trend – we will see some modest benefits from a growing focus on evasion. Modest, because unless someone is brave enough really to tackle the shadow economy, our scope for improvement is limited.

Thanks Jolyon, I am not clear what you mean by regulation creating ‘imbalances in the system’. Can you be specific at all?

It’s a whole other piece – and it’s a rather piece for me to write – but you might get some sense of what I have in mind if you read this.

Sorry to be late to the party. At times there are too many blogs to reply too (like the new one on reliefs/expenditures) plus finding the opportunity to study the Tax Gap publications. And something substantial like this needs a substantial reply!

Jolyon has picked up on some interesting figures and trends, although I think the excise gap worries are not actually excise, as this has fallen significantly, but refers to the alcohol and tobacco trends. That would explain why the Budget is putting money there. It’s more than likely this is organised smuggling by criminal gangs, where intelligence led activity is more cost-effective in detection than stopping every white van that goes through a Channel port. But it certainly illustrates an area where some more “boots on the ground” might improve intelligence and serve as a (small) additional disruption.

As for tax expertise within the Labour Party it must surely be possible to assemble such people, especially given the calibre of the new economic advisers. And I’m sure there are those in the tax profession willing to act as “sanity checkers” on new ideas (like addressing tax relief and “tax expenditures”?).

The Tax Gap analysis has some other interesting material, sometimes buried in the footnotes and methodological annexe. The following tables suggest that error is falling, for reasons that are not immediately apparent. Perhaps taxpayers are more aware of the possibility of error, or perhaps HMRC has got the forms better?

Table 6.3: Proportion of Self Assessment returns with under-declared tax liability1

2005-06 2008-09 2009-10 2010-11 2011-12

Proportion of SA returns 29% 26% 25% 20% 19%

of which, size of under-declaration

£1 to £500 15% 13% 12% 9% 9%

£501 to £1,000 5% 5% 5% 3% 3%

over £1,000 9% 8% 9% 8% 7%

Table 6.4: Business taxpayers: Proportion of Self Assessment returns with under-declared tax liability

2005-06 2008-09 2009-10 2010-11 2011-12

Proportion of SA returns 49% 39% 38% 31% 25%

of which, size of under-declaration

£1 to £500 21% 16% 15% 13% 10%

£501 to £1,000 10% 9% 8% 5% 5%

over £1,000 18% 14% 15% 13% 10%

Table 7.5: Proportion of SMEs with incorrect Corporation Tax returns where additional liability established

2005-06 2008-09 2009-10 2010-11 2011-12 2012-13

Proportion of SMEs 41% 25% 24% 23% 19% 16%

of which, size of additional liability

£1 to £1,000 22% 11% 10% 12% 12% 11%

over £1,000 19% 14% 13% 10% 7% 5%

This is not all good news. If businesses are getting better (less prone to “error”) the same does not seem to be true of non-business taxpayers, where rates are not falling in the same way, but are essentially static. So maybe we need to consider how we get non-business taxpayers to improve, in line with the more publicly maligned ‘businesses’

Table 6.5: Non-business taxpayers: Proportion of Self Assessment returns with under-declared tax liability

2005-06 2008-09 2009-10 2010-11 2011-12

Proportion of SA returns 14% 15% 13% 11% 14%

of which, size of under-declaration

£1 to £500 10% 9% 8% 6% 9%

£501 to £1,000 2% 2% 2% 1% 2%

over £1,000 2% 4% 3% 4% 3%

But equally interesting (to geeks) are some careful qualifications on the size of the estimates. One concerns the losses attributable to large businesses. There is a small uplift totalling £1bn over a four year period. This is because “HMRC has always acknowledged that it may not identify every risk and this has previously led to an under-estimation of the tax gap. This year for the first time we have evidence from the Large Business Risk Task Force created following the Chancellor’s Autumn Statement in 2012. The additional risks identified by the Large Business Risk Task Force has allowed us to derive an uplift for unidentified risks.” (p66)

In other words, the more staff you have to look for risks the (marginally?) higher the results. Given the reductions in HMRC staffing that Jolyon mentions (from which Large Business were not exempt) you wonder if there are still a few more millions awaiting discovery?

And the same is true, but more so, for the losses from ghosts (£1.2bn) and moonlighters (£1.9bn). The methodological annexe (G57 and G58) describes the use of techniques like questionnaires, or Jobseeker’s Allowance claimants. I suspect this is as strong as can be done but I wonder if there any additional surveys or approaches that might be tried. It is no surprise that the Tax Gap warns (p57) “Due to the extent of the assumptions used to produce this estimate and the inherent uncertainties in the methodologies, this estimate has a large margin of error and should be treated with due caution.”

I can see Jolyon’s concern that some recent measures to tackle high-end avoidance have created a lot of friction, especially in a few firms. But in terms of HMRC’s interactions with taxpayers as a whole, those measure apply to a very small fraction of the total taxpayer base. It seems unlikely to me that this declining goodwill hinders efforts to tackle evasion, the hidden economy, or reduce error by non-business taxpayers.

Finally, I agree on the hidden economy (£6.2bn) and evasion (£4.4bn). The end of the Tax Return may contain that brave step,or half-step, over which Sir Humphrey cautioned Ministers. It says “Their accounting software will be able to feed data straight into their digital tax account, so most businesses will simply log-in to check their details with no need to send an annual return”. Whilst this may not deal with purely cash based transactions (the household services like window cleaners or gardeners) I suspect this will give HMRC a much greater understanding on businesses, such as times and values of transactions. It will be that much harder to the conceal business activity, especially if coupled with things like the Merchant Acquire data.