Remember shares for rights?

I’ll let Osborne jog your memory for you. Here’s an extract from his 2012 Conference Speech:

This idea is particularly suited to new businesses starting up; and small and medium sized firms.

It’s a voluntary three way deal.

You the company: give your employees shares in the business.

You the employee: replace your old rights of unfair dismissal and redundancy with new rights of ownership.

And what will the Government do?

We’ll charge no capital gains tax at all on the profit you make on your shares.

Zero percent capital gains tax for these new employee-owners.

Get shares and become owners of the company you work for.

Owners, workers, and the taxman, all in it together.

Workers of the world unite.

And the deal would be sweetened by tax breaks. The first £2,000 of shares would be free of income tax. And the first £50,000 of shares free of capital gains tax.

It felt, even at the time, rather ugly. Should we be allowing employers to strip fundamental protections from their employees? Here’s the view of Lord (Gus) O’Donnell, speaking in the House of Lords:

You might think it even worse than that. We weren’t just permitting it. We were, through the tax system, incentivising it. To extend Gus O’Donnell’s metaphor, the rest of us, who fund these reliefs through their tax bills, were encouraging and subsidising the slave trade.

And the amount, and likely beneficiaries, of that subsidy was alarming too. As Paul Johnson of the IFS warned at the time:

it has all the hallmarks of another avoidance opportunity.

And although the cost was said to be fiscal washers:

The OBR highlighted that this was only because Treasury was looking at it only over a five year time scale (an oft-resorted to piece of trickery as I noted here). Beyond that timescale, the cost would quickly rise towards £1 billion per annum (real money, even in Treasury terms: by way of illustration about what was expected to be raised by the Mansion Tax):

But nevertheless we shouldn’t worry because:

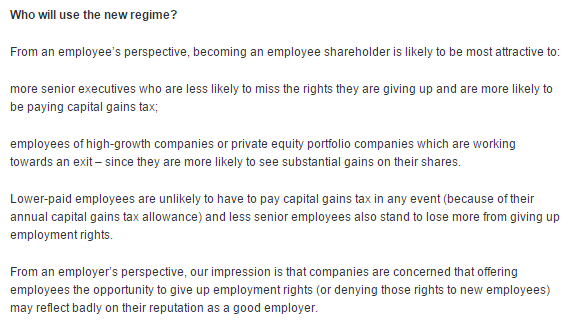

Now, I raise this because of a chance remark from a friend at a very grand firm indeed who said that he was spending all of his time constructing shares for rights schemes for private equity and MBO clients. But none, he said, for ‘normal’ people.

Let me explain the swizz, and why it’s so valuable.

Forget about the income tax break. £2,000 might be meaningfully valuable to regular folks. But they’re not (as we shall see) the people for whom Shares for Rights was designed for. And it’s not what the OBR was worried about.

There are two other features that enable – you might almost think encourage – the real swizz.

First, the capital gains tax limit isn’t a cap on the amount of relief. It doesn’t give you the first £50,000 of gains tax free (saving you a mere £14,000 in tax). It’s a cap on the value of the shares when you get them.

Second, the shares don’t need to be ‘normal’ shares. They can be so-called ‘sweet equity’: very special shares for the very special people – the ‘value adders’ at the top.

Now. Assume you’re in private equity and you buy a company for £1m. What value might HMRC attribute to special shares which gave you a right to all of the sale proceeds above £1.25m in five years time? Not very much in a world where the Government can borrow over a five year term at an interest rate of only marginally above 1%. Less than £50,000?

Of course, the invariable logic of private equity deals is that you think you’ll be able to obtain high capital growth. Without that belief you don’t transact. If you’re wrong, then of course the capital gains tax break is worth nothing. But if you’re right?

Assume that in five years time you sell the company on for £1.8m. You’ve now got a capital gains tax break on £550,000 worth £154,000.

I’ve simplified my example – but not relevantly so. Here are some other ones from the law firm Bird & Bird. They conclude, tellingly, by asking: “Is this too good to be true?” (I’ll spare you the suspense. The answer is ‘No’. Or what passes for it if you’re a lawyer).

But don’t just take my word (and Bird & Bird’s) that it’s best used by senior management in private equity deals. Look here. Or here. Or here. Or here. Or… well, you get the picture.

Indeed, of course, as Magic Circle firm Linklaters observed, it was never even designed to be used by lower paid employees.

So much for workers of the world uniting. (Although there is a sort of uniting: together the rest of us have to make up the lost tax.)

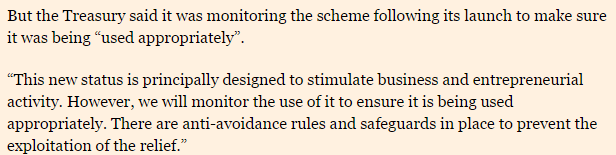

Oh, and how’s that monitoring going by the way?

Not so good. I couldn’t find a figure – although one is given for other types of employee share schemes. And I did find an HMRC document entitled: “Tax allowances and reliefs in force 2013-14 or 2014-15: cost not know” which contains a reference to, yep:

Gains on disposals of exempt employee shareholder shares

So whilst it could be the £1bn predicted by the OBR. It could be more. Much more. It could be the whole amount being saved in 2016-17 by cutting tax credits.

Despite what Treasury promised, we Just. Don’t. Know.

I agree, it’s very difficult to see how HMRC will monitor it successfully. It’s also very difficult to see what the policy objective behind this legislation is.

HMRC do have details of the number of companies that use these shares as their value is invariably agreed with HMRC at grant.

HMRC also have details of the number of employees who receive these shares (and their initial value) because they are separately disclosed on the ‘other’ share plan return. HMRC will also have some details as to the type of shares on the ‘other’ return (are they the largest class of share in the company?) which can help risk assess them.

But it is difficult to see how HMRC will be able to get a sensible estimate of the value of the gains that are eventually realised as that is not something that is disclosed. This is not disclosed on the self-assessment tax return or the ‘other’ share plan return.

It’s likely that there have been relatively few exits at the moment because the shares only started to be used in September 2013 and so at the moment the amount of tax saved is likely to be relatively small. But soon their will be more secondary buy-outs, listings, etc.

If I was HMRC I would be changing things to make it clear what the actual gains that were exempt were. If I was in HMT, I would be wondering whether this was introduced to create work for lawyers.

if HMRC took a policy decision to challenge the implementation on a strict basis, I think that some people using them could struggle to show that all the conditions in s205A have been satisfied.

One thing that I think would be interesting is to see how some of the current ways of using these shares interacts with the GAAR.

Similarly, I would be wondering whether some of the artificial conditions that allow the £2,000 AMV to be achieved should be effective. But fortunately, I do not have to worry my pretty little head about such things.

Just to be clear, it is not only private equity situations that use these shares. There are many others but what they all have in common is that they expect high share price growth. Some of these are relatively new, growing companies. Also, it is used by people who work at the target company, not those those who manage the funds.

If I were the Chancellor, I’d be scrapping this for new shares and allowing, as a nice transitional rules, the exempt gains to be included as part of the entrepreneurs’ relief limit for the individual (and capped at that amount).

This is why I really don’t like tax exemptions. I’m not really fond of reliefs, either, to be honest, or setting up lots of privileged situations. Tax should be on the economic position, and if you want to encourage something then actively encourage it, don’t do it through the tax system.

I never liked this one, in particular. Bin it. Maybe allow ER on existing schemes as a transitional rule (although I think ER is over-generous, too), but don’t let any more start up.

I know a partner at a law firm who has been “churning them out” for private equity clients and expressed surprise that I’d not done any (too complex, smells wrong).

As regards monitoring, it’s very easy to check how many are in place, since one part of the scheme is that you can write to HMRC in advance to check that the value is between £2k and £50k. You should pretty much always do that, because if you get the value wrong then you lose the tax relief (ie if the value is £1900 then you pay tax on the lot). As for the potential loss of tax, well that depends what the shares are worth now, so it’s impossible to know.

One of those times when you wish you hadn’t been right… A selection of contemporary quotes I heard from accountants in practice when the proposals first surfaced:

“I read this with growing horror – I’ve spent years telling clients they can’t just choose the employment status of people who work for them.”

“…government is continuing its practice of rushing through major changes, often without properly considering the consequences.”

“If there is no guarantee of voting rights or dividends what is the difference going to be in terms of corporate performance over the current ESOP system?”

“As a reputable employer, I don’t think we would want to recruit staff this way.”

“… this is not well thought through and there are some considerable operational issues with this type of scheme. They can be made to work but it will need careful drafting of the legislation and the rules.”

The speech was surely written by a spad or another little wonk working for George…. but where did the idea come from, surely not HMRC or the Treasury?

Is there a pool of “advisors” who are hired to come up with off the wall ideas like this… and selling off the remaining council houses on the cheap and appealing to only the most dedicated party faithful?

Pingback: Balancing the Books – with One Eye Shut | Waiting for Godot