If you click here you can see a link to the Electoral Commission list of donations to referendum participants arranged by size.

I have listed below the ten donors of the largest donations, in descending order, to the ‘Out’ campaign and some material in the public domain that might cast light on the attitudes of those donors to tax and tax planning.

There is, of course, much other material in the public domain about those individuals – both positive and negative. It is my intention only to set out what is in the public domain that could reasonably be thought to cast light on their attitudes to tax and tax avoidance. Where I have given other information it is only by way of introduction to individuals about whom little else is known.

1. Peter Hargreaves gave £3.2m to Leave.EU Group Limited.

Here’s what the Daily Mail records him as saying about corporation tax.

I never understood why companies should pay tax. They don’t have a vote. If they didn’t have to pay tax, they would come here in droves and employ millions of people who would pay loads of tax.

This is consistent with other public statements that suggest he believes that lower taxes generate more tax receipts. He took steps to pay an increased dividend before the 50% tax rate came in.

2. Better for the Country Limited – otherwise known as Leave.EU – made a non-cash donation of £1.95m to Grassroots Out Limited. The Guardian has identified that Leave.EU was incorporated by STM Fidecs Nominees Limited, a company based in Gibraltar that “specialises in financial planning…. for high-net-worth individuals… re-locating to, other, frequently lower, tax jurisdictions.”

Its shares were then transferred to Arron Banks who remains, so far as the public record discloses, both a director and 100% shareholder. Arron Banks’ name has appeared in the so-called Panama Papers. The Guardian reports that he has set up “37 different companies using slight variants on his name.” That, you may think, is a tendency associated with a desire to reduce transparency.

The Guardian report also contains this paragraph.

3. Diana Van Nievelt Price gave £1m in cash to Vote Leave Limited. Little is know of her.

4. International Motors Limited gave £600,000 in cash to Vote Leave Limited. “Lord Robert Norman Edmiston” is a director of International Motors Limited. The shares in that company are held by I.M. Group 1991 Limited, the shares in that company are held by I.M. Group Limited, and the shares in that company are held by “Robert Norman Edmiston”. Lord Edmiston is said by the Mirror to have had his first application for a peerage blocked by HMRC over a tax dispute. He is also reported to have received an “accelerated payment notice”. Accelerated payments notices are given by HMRC to those claimed by it to have used a “tax avoidance scheme”.

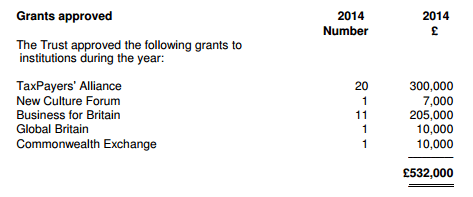

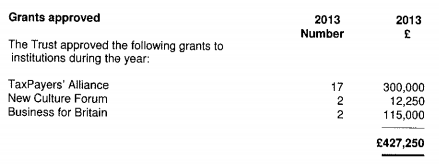

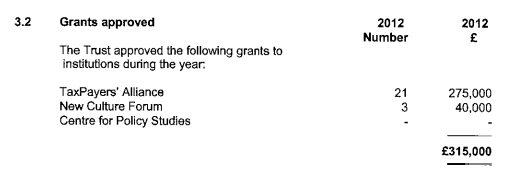

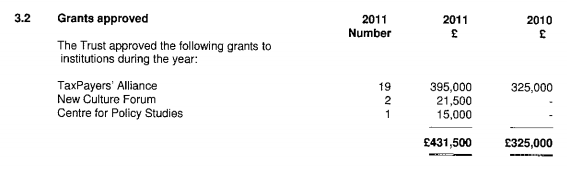

5. Patrick Barbour gave £500,000 in cash to Vote Leave Limited. Patrick Barbour was until 10 April 2013 a trustee of the Politics and Economics Research Trust. I have written here about how over the last five years 79% of its grants have been made to the so-called Taxpayers’ Alliance. And I have described PERT as “channelling money to the Taxpayers’ Alliance.” The Politics and Economics Research Trust is currently in discussions with the Charity Commission “about decision making and monitoring of grant funding.” I hope to write more on this after the Referendum. Patrick Barbour has also written papers for the Taxpayers’ Alliance.

6. Gladys Bramall gave £500,000 in cash to Vote Leave Limited. She is a former member of the BNP but little else is known about her.

7. Jeremy Hosking made two donations to Vote Leave Limited (£500,000) and Brexit Express (£480,000). He operates a hedge fund.

8. Peter Cruddas gave £350,000 in cash to Vote Leave Limited. Peter Cruddas is a one-time resident of the tax haven Monaco and former Co-Treasurer of the Conservative Party who resigned over the ‘cash for access’ scandal.

9. Terence Adams gave £300,000 in cash. He appears to have construction interests in the US.

10.= John Stuart Wheeler gave £250,000 to Vote Leave Limited. The Guardian has written of his £5m donation to the Conservative Party in 2000 which was followed shortly thereafter by Conservative MPs seeking to change the Finance Bill in a manner which would benefit the tax treatment of financial spread-betting, the industry in which Mr Wheeler then operated. Jonathan Wood also gave £250,000 to Vote Leave Limited. There is a Jonathan Wood, hedge fund manager, who has made substantial donations to the Conservative Party. The Evening Standard reports he has lived in Switzerland and Monaco – both might reasonably be described as tax havens.

For reference – and I imply no connection to the matters stated above – I have written here about some highly misleading tax related statements made by leading Vote.Leave figures such as Michael Gove, Boris Johnson and Iain Duncan Smith. I have written here about how leaving the EU will reduce the UK’s ability to combat tax avoidance.

For the sake of transparency, I should say that I will be voting Remain tomorrow.

Follow @jolyonmaugham

And 31 December 2012?

And 31 December 2012? And 31 December 2011 and 2010?

And 31 December 2011 and 2010? So over those five years PERT made 95 grants (including

So over those five years PERT made 95 grants (including

{kind=link}

You must be logged in to post a comment.